An Easier Fed Era

Hello All,

As the week has kicked off, it’s been a relatively quieter one as recent holiday volumes have persisted but initially to kick off the week, we did see the indices gap-down lower which was mostly attributed to the selloff within global bonds due to hawkish comments / jawboning out of Japan where December rate-hike odds now sit near 80%, but as the week has progressed, the dip sure enough got bought given the accommodative tailwinds from the Fed with a December rate-cut essentially solidified along with the continued loosening of financial conditions acting as an added tailwind too.

Thus far on the week, the Q’s have been the best performing of the indices, currently higher by 68bps, whereas Spooz has been the ‘worst’ performing of the indices although is just essentially flat on the week, higher by 2bps.

We recently published our ‘2026 Outlook’ which has a plethora of coverage on a wide range of topics / themes as we get ready to head into 2026 after coming off a strong ‘25 & for those who would like to read & prep for ‘26, I included the report just below:

Earlier on in ‘24, a series we had started was ‘Educational Pieces’ with each including a wide variety of topics, some even suggested by you all & we’ve finally decided to release Part Trois.

Nevertheless, for those whom may have missed the first educational piece along with the subset of topics included:

General background / knowledge on all option strategies

In-depth talk on risk / reversals & how to go about expressing / utilizing them

Options Structuring

When to used naked calls / puts vs. spreads

Choosing expiration dates

Identifying key pivots / supports / resistance zones

General briefing on stock gaps

What to look for in regards to fundamentals

Implementing fundamental / macro / technicals into a trade

Hedging

Creating risk/reward setups

Taking profits / managing losses

Overall Process

Book recommendations

I include a link here to the original.

And given the amount of positive feedback we had received on the first educational piece & how helpful it was for many, we decided to release Part Deux earlier on in ‘25 & for those who may have missed, a link to Educational Piece Part: Deux can be found here.

And then FINALLY, a link to the last part of the series, Part Trois (For now, Part Quatre coming soon), can be found here.

Psychology is the silent driver of performance & your edge often comes not from knowing more but from managing yourself better.

To jump straight into it, again, it’s been a relatively quieter week with not much action necessarily to recap as economic data in general has remained on the quieter-end & recent holiday volumes have carried over from this past week & into year-end, we’re essentially down to two ‘significant’ events before 2025 is essentially wrapped up & it boils down to FOMC next week in which a December cut is already essentially solidified & it more so will come down to if Powell’s tone is dovish & or hawkish leaning & finally, we also will receive the November jobs report the following week which is arguably one of the more important reports as we’ll see the effects from the recent Govt. Shutdown & the general expectations are a negative weight / effect on the economy.

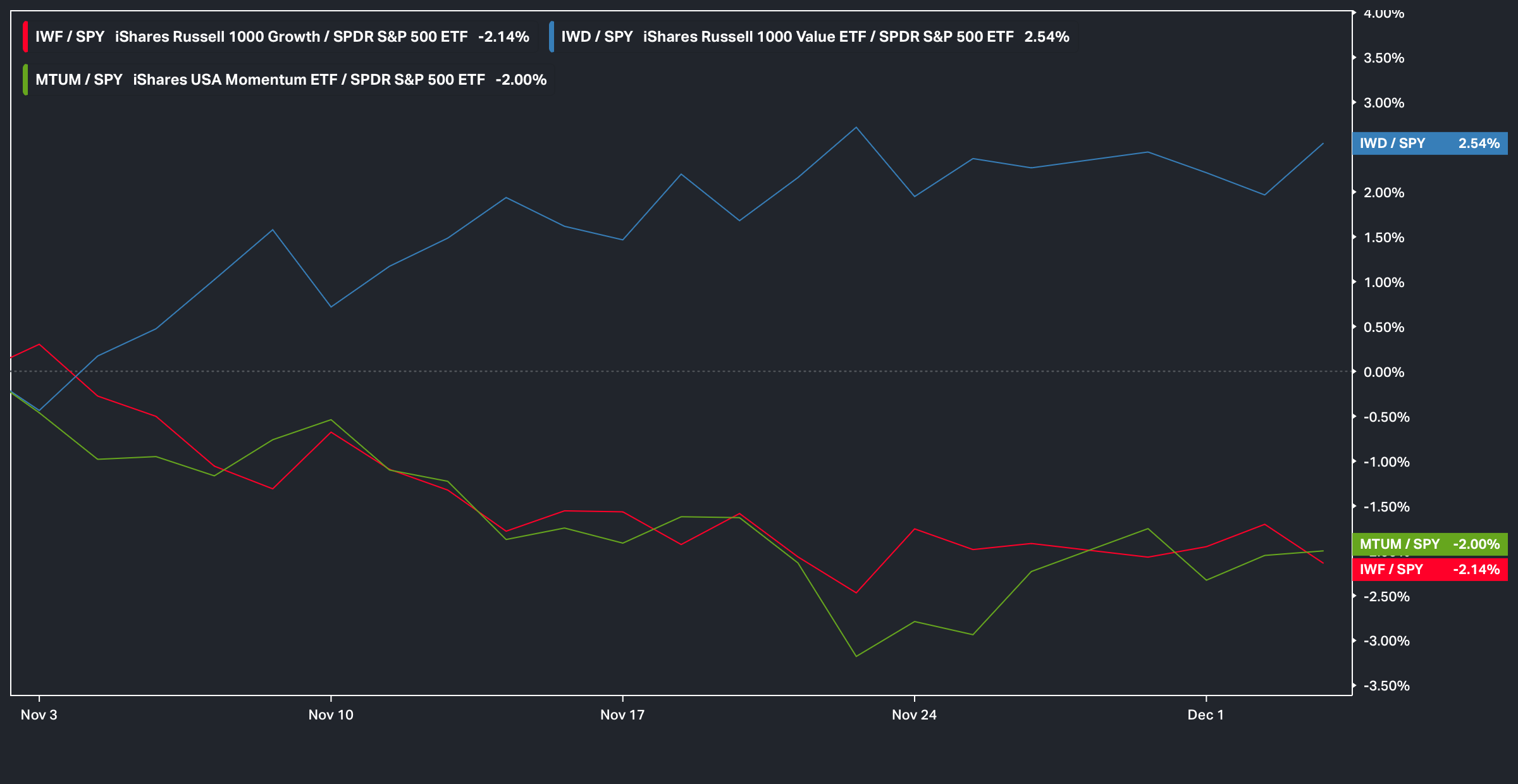

Having said that, the general theme which has continued to persist through December from November is the continued rotation out of Beta / Momentum-driven names to instead Value (Cyclicals / Lower-beta names) & that can be clearly seen just below as there is a near 500bps spread between the groups:

Nevertheless, recent action within the indices following the Fed’s pivot from a couple of weeks back essentially solidifying a December cut has been quite impressive as despite Spooz still sitting just 100bps below ATHs, the Advance-Decline Line actually went on to go ahead and make a new high which is a strong signal for healthy upside participation / underlying breadth metrics.

And following the rebound within the indices after the tantrum decline a couple of weeks back, we’ve seen shorter-term oversold signals (% of Stocks Above 20D) work all the way back toward slightly overbought territory; The % of Stocks Above the 20D is sitting near 70% after being sub-30% just a couple of weeks back.

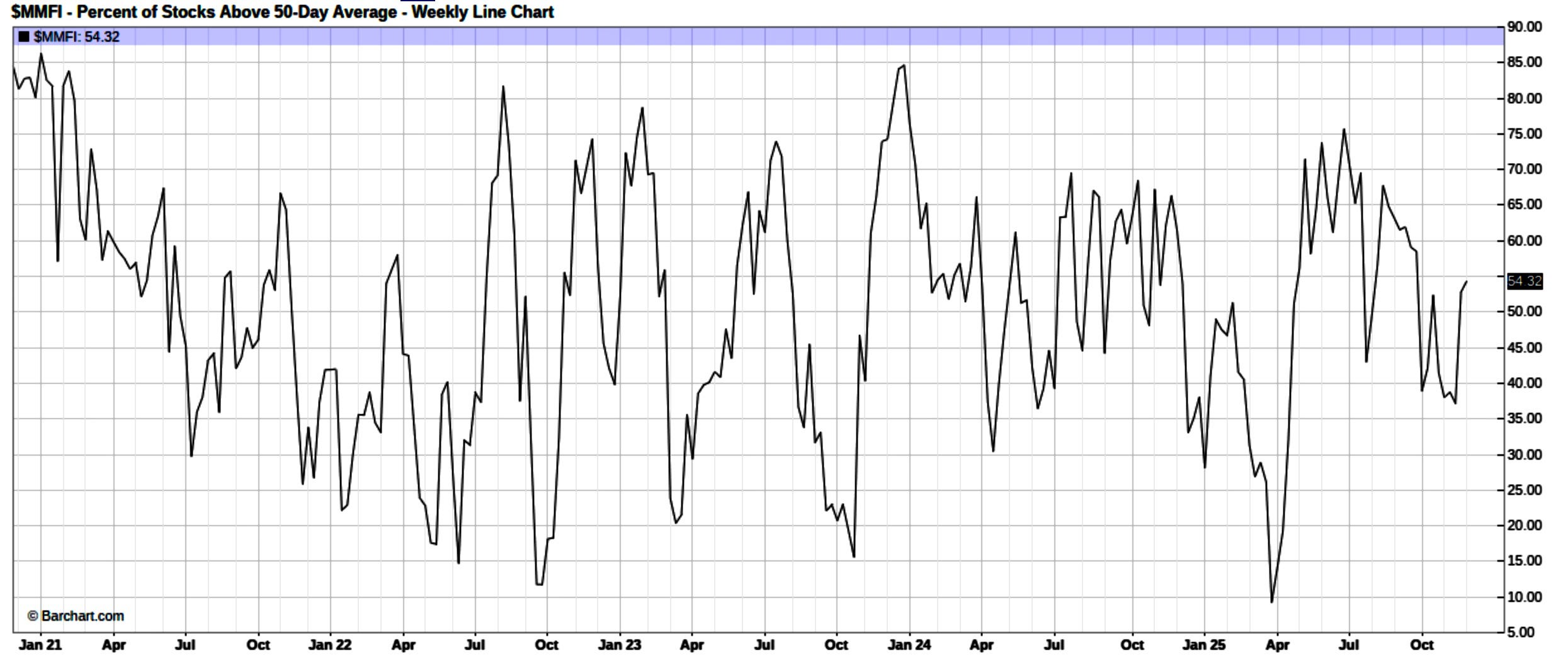

And on a more broader timeframe, the % of stocks above the 50D hasn’t quite made it’s way into overbought territory & is still arguably more neutral which emphasizes in the shorter-term, although conditions may be slightly overbought, the broader picture is the indices are still recovering from the 2+ week tantrum decline with conditions still remaining within neutral territory.

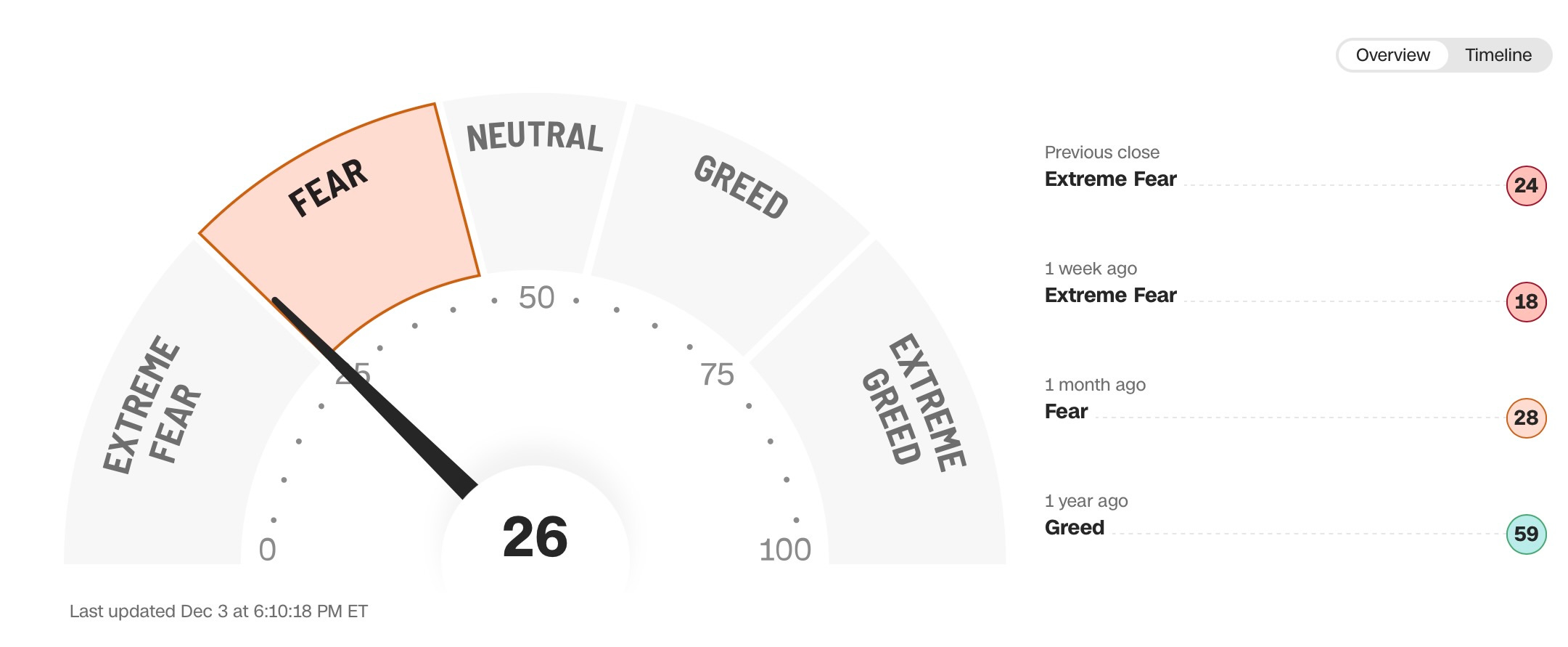

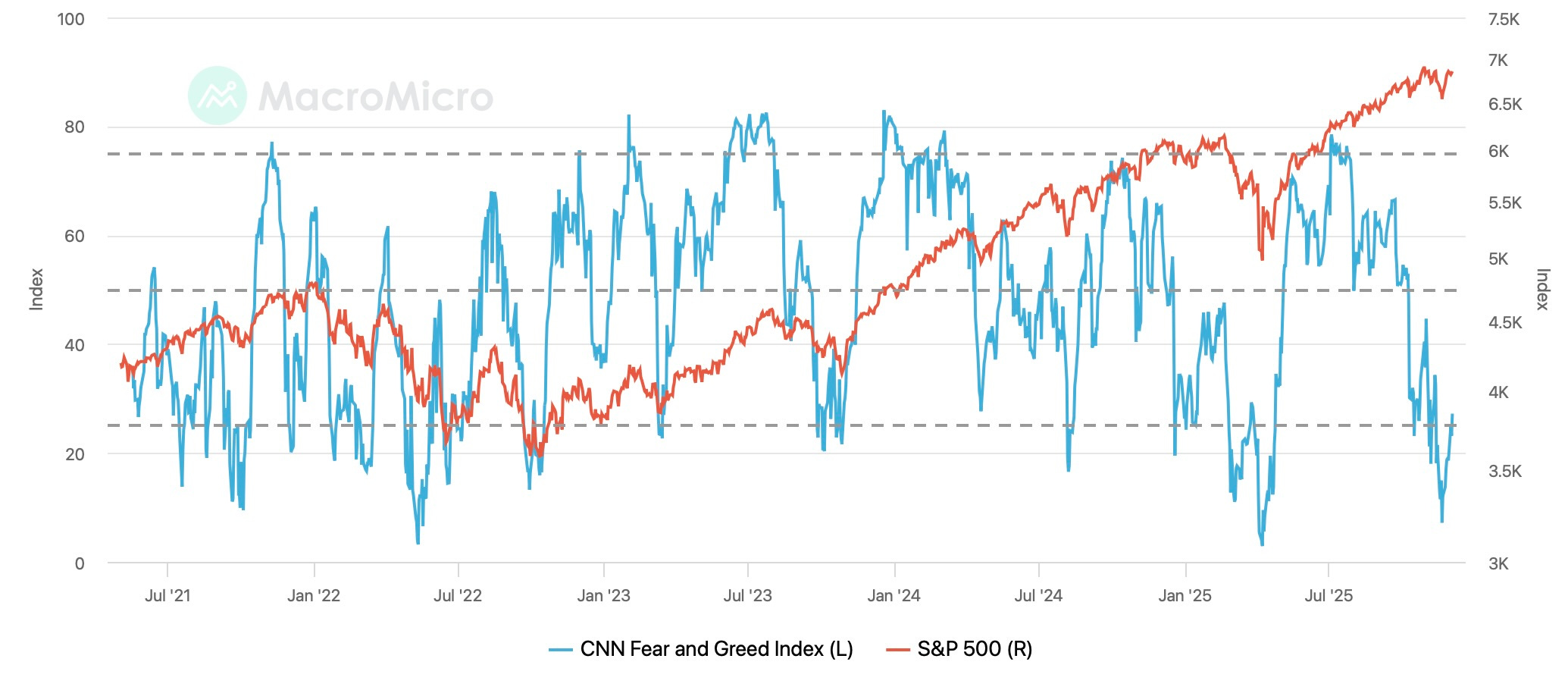

And of course, the other interesting phenomenon worth sharing is despite Spooz being just 100bps off ATHs, the fear-greed index has hardly budged & still remains within ‘fear’ territory.

And to those whom dis-credit the metric & or feel that it’s faulty / not accurate, as pictured below but the indicator has actually proven to be quite reliable and periods within ‘extreme fear’ territory have tended to mark every major interim low & or ‘hard’ bottom these past few years:

Moving away from the indices, again, we haven’t necessarily had much economic data reported this week although there have been a couple of standout data-points worth mentioning:

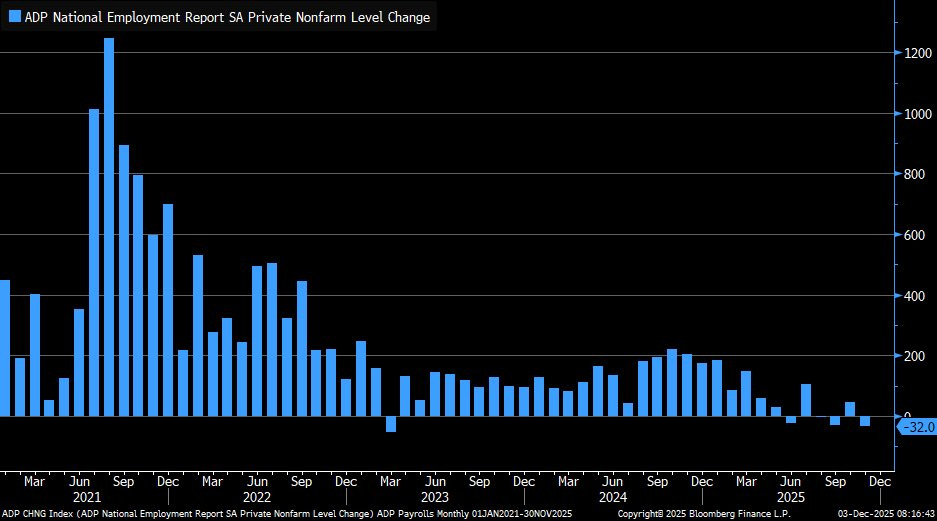

Today’s ADP report showed private-sector payrolls fell by 32k in November, the third decline in four months and the largest drop since 2023, underscoring a cooling labor market. Weakness was concentrated in small firms, which cut 120,000 jobs, whilst large firms added 39,000 and medium-sized firms added 51,000, continuing a three-month pattern in which small businesses have shed roughly 178,000 workers whilst large companies added about 143,000. The losses were led by professional and business services, information, manufacturing, construction, and financial activities, whereas hiring remained positive in education and health services and leisure and hospitality.

Although the report shows clear softening beneath the surface, large firms are still hiring and core service sectors like education, health care, and leisure/hospitality remain resilient, which suggests demand hasn’t collapsed. Wage growth is also cooling in an orderly way rather than collapsing, pointing to a labor market that is normalizing rather than crashing, with the slowdown concentrated in smaller, rate-sensitive businesses rather than broad-based weakness.

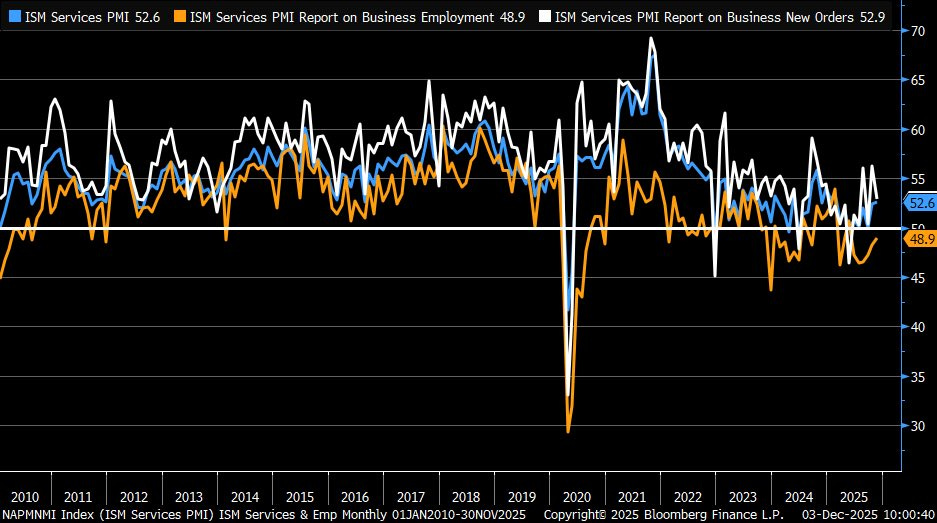

And moving along into the November ISM #’s, Services came in at 52.6, up slightly from 52.4 and above expectations, signaling that the U.S. services sector remains in expansionary territory. But having said that, new orders fell to 52.9 from 56.2, suggesting softer demand and inflation pressures moderated as prices paid dropped to 65.4 from 70 (7-month low), indicating some easing in cost pressures. Finally, we did see a slight improvement within the employment index, up from 48.2 to 48.9, but it still does remain within contractionary territory. With that being said, it’s also worth noting that the survey period overlapped with the government shutdown which may have influenced business sentiment and contributed to some of the softness in demand and hiring intentions so data in general is likely to be a bit noisy rather than a ‘big’ signal. The weakness in the interim is essentially to be expected & is well-anticipated.

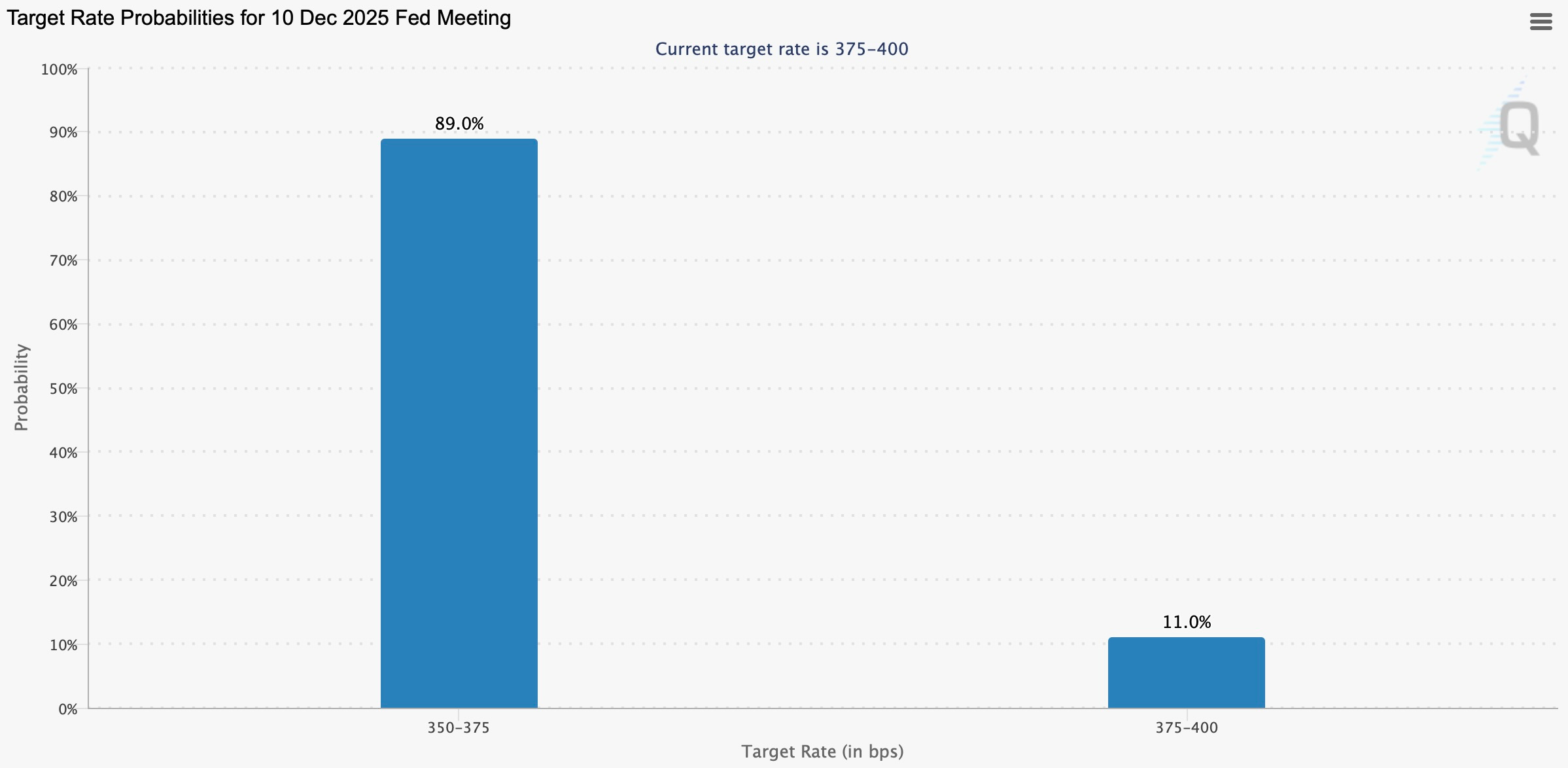

And following the recent softness in data along with continued dovish commentary out of the Fed ever since the new cycle highs within the unemployment rate a couple of weeks back, the odds for a December cut now sit firmly just below 90%, essentially solidified into the December FOMC meeting next week.

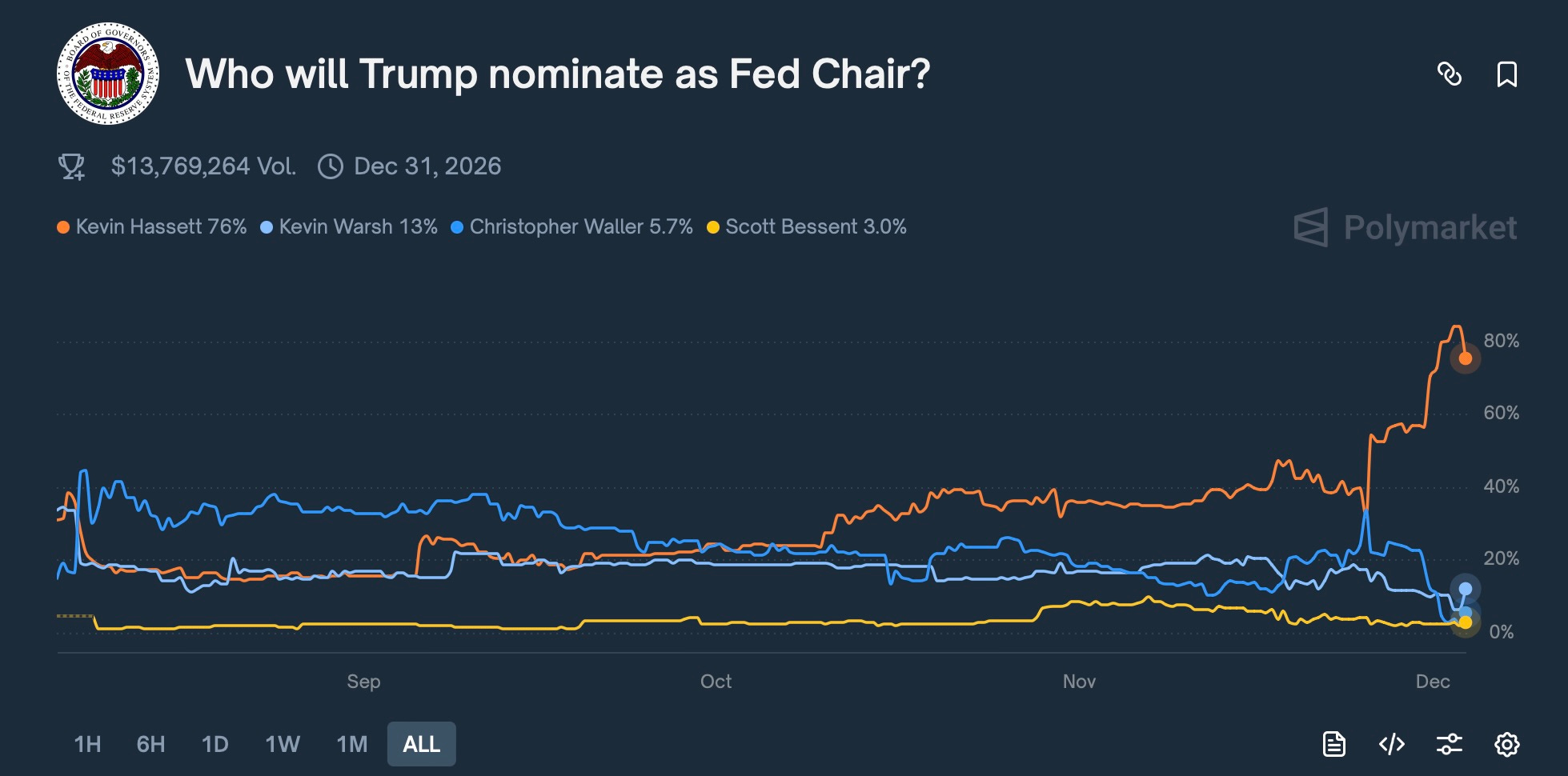

But despite FOMC next week, Powell will likely be viewed as a ‘lame duck’ anyways given he will be on is way out early next year as his term comes to an end & markets instead will be paying attention toward whom Trump selects as Powell’s replacement & as of now, Hassett remains as the current favorite with Warsh as the 2nd favorite & Waller as the 3rd favorite.

And it shouldn’t be of any surprise that Hassett is the current market favorite given he has clear motives to aggressively cut-interest rates along with the relative close ties to Trump as well: