Fiscal Stimulus Derby

Hello All,

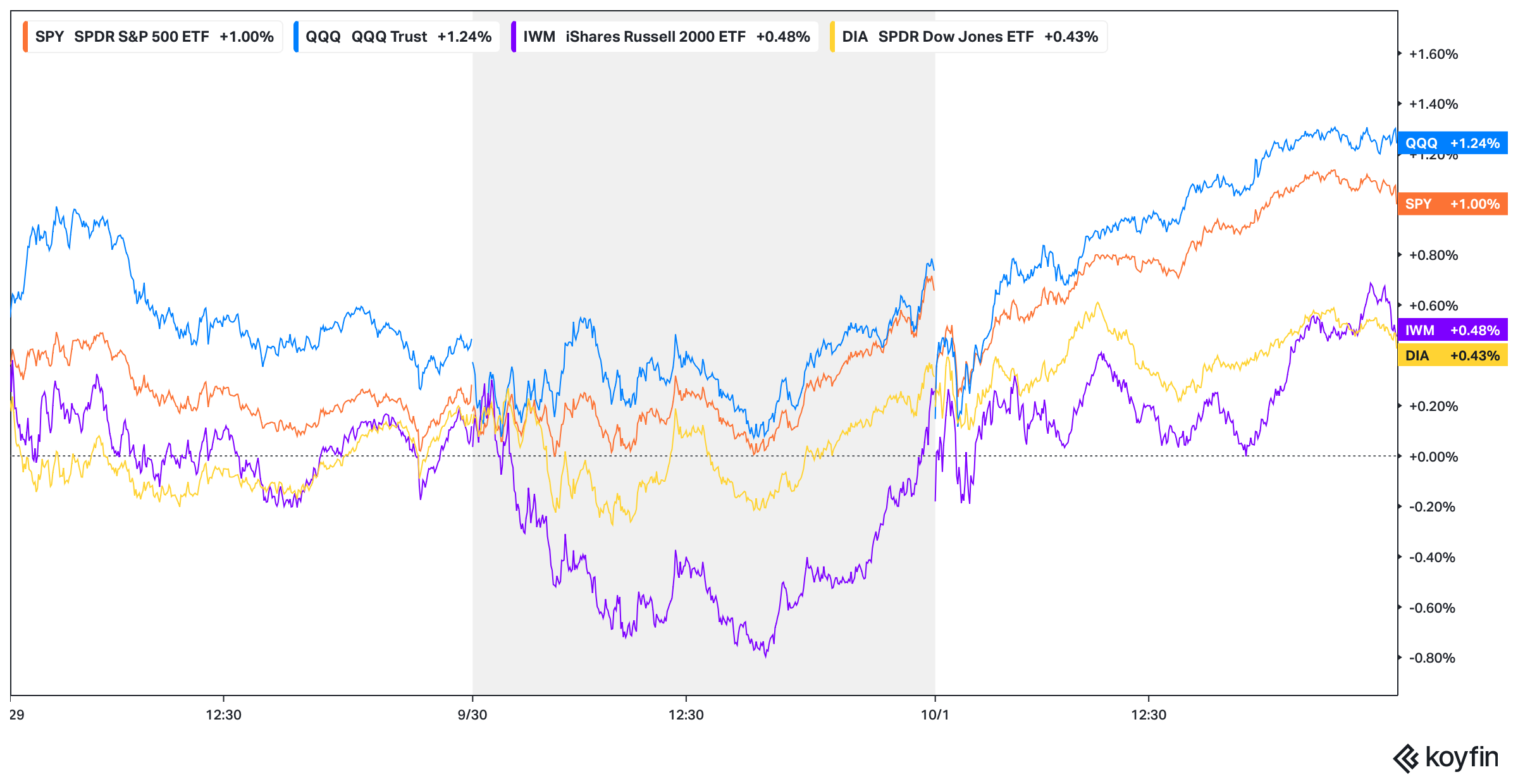

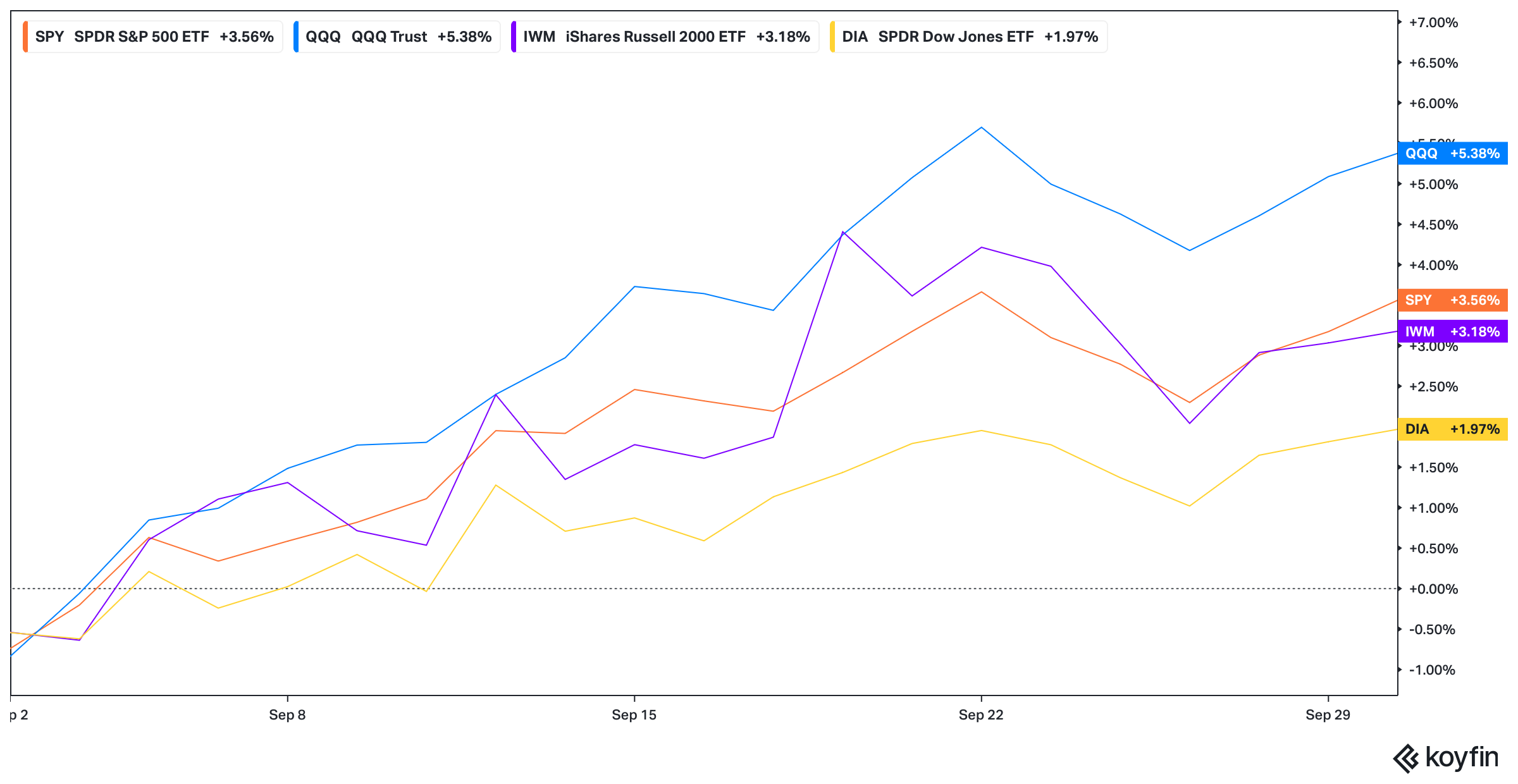

We’ve had a slight pickup in events / economic data as the week has initially kicked off followed by the Govt. having been shutdown for the time being (Likely no NFP report on Friday) along with recent economic / labor data having been somewhat mixed / softer than expected, but nevertheless, that still hasn’t stopped the pattern of shallow dips continuing to be bought as Spooz in itself went on to make yet another new ATH today, up 100bps on the week, whereas the Q’s thus far have been the best performing of the indices, +124bps on the week, & Small-caps & the Dow have more so traded inline & are both up around 45bps on the week.

Earlier on in ‘24, a series we had started was ‘Educational Pieces’ with each including a wide variety of topics, some even suggested by you all & we’ve finally decided to release Part Trois.

Nevertheless, for those whom may have missed the first educational piece along with the subset of topics included:

General background / knowledge on all option strategies

In-depth talk on risk / reversals & how to go about expressing / utilizing them

Options Structuring

When to used naked calls / puts vs. spreads

Choosing expiration dates

Identifying key pivots / supports / resistance zones

General briefing on stock gaps

What to look for in regards to fundamentals

Implementing fundamental / macro / technicals into a trade

Hedging

Creating risk/reward setups

Taking profits / managing losses

Overall Process

Book recommendations

I include a link here to the original.

And given the amount of positive feedback we had received on the first educational piece & how helpful it was for many, we decided to release Part Deux earlier on in ‘25 & for those who may have missed, a link to Educational Piece Part: Deux can be found here.

And then FINALLY, a link to the last part of the series, Part Trois (for now), can be found here.

Psychology is the silent driver of performance & your edge often comes not from knowing more but from managing yourself better.

To jump right into it, this week has been somewhat more active in regard to event risks / economic data, but in general, the same theme has continued in terms of dips within the broader indices being relatively shallow & bought as the slow churn / grind higher continues…

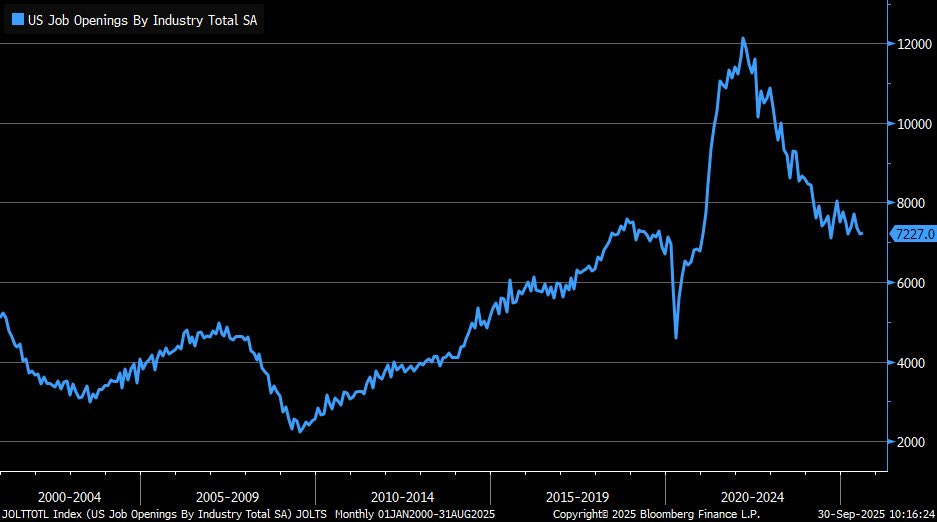

Moving along into economic data, the August JOLTS report yesterday showed job openings at 7.23 million, roughly in line with expectations and slightly above the prior month, whilst the quits rate eased to 1.9% and the layoffs rate held steady at 1.1%, thus signaling a cooler labor market. Hires fell by 114,000 to 5.13 million, the lowest since June ‘24, with July also having been revised lower thus marking four straight months of declines.

Overall, not much has necessarily changed but we’re still within a slow to hire & slow to fire market (Call it stagnation).

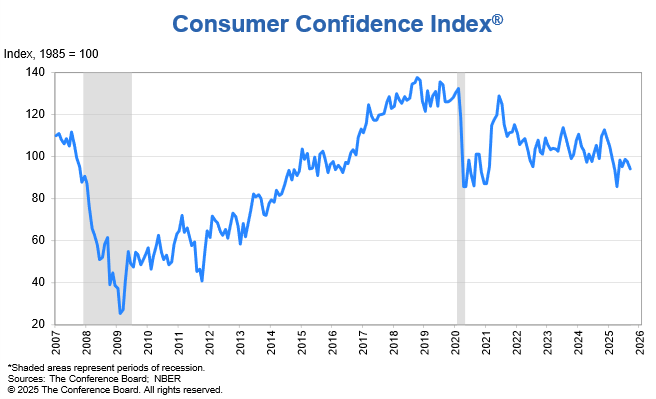

Another ‘gloomy’ datapoint was the decline within Consumer Confidence #’s yesterday following a sharp deterioration in consumers’ views of the current economic situation… this shouldn’t be of too much surprise either as Main Street has been left in the dust & Wall Street more so remains in focus by the administration.

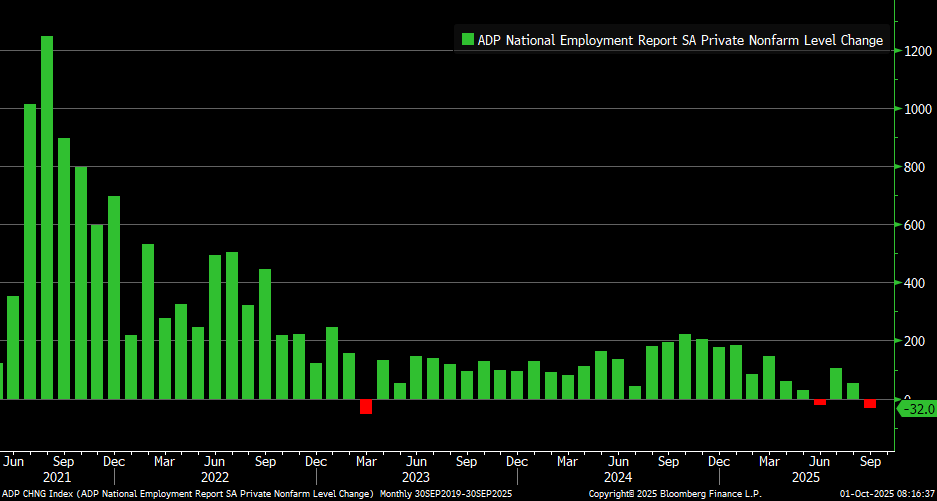

And finally, likely the last datapoint of the week given the government remains shutdown, but ADP #’s ended up coming in softer than expected at -32k which was the largest decline dating back to March ‘23 during the brief regional banking crisis & I wouldn’t necessarily say ADP is a good measure in terms of predicting NFP #’s as the correlation has actually been quite off (Running joke of strong ADP = Weak NFP & vice-versa) but do think the bigger signal here is it’s clear there’s been continued weakness within the private sector as ‘Main Street’ continues to suck wind in the economy.

And following the recent softness in data this week, odds for an October rate-cut jumped higher essentially solidified at 99% & we’re right back to the debate on whether or not the Fed should be cutting 25bps as an insurance cut & or 50bps to try & get ahead before the labor market cracks / deteriorates even further (Fed is late).

Heading into the remainder of the week, again, given the government is shutdown, we likely won’t have an NFP print on Friday but I do feel the subject is still worth touching on briefly given the recent softness in data along with continued slowing growth concerns but as of now, Jobs for the month of September are expected to come in at 51k, up from 22k the prior month whereas the UER is expected to remain unchanged at 4.3%. IF that were to be the # reported & or around that general ballpark, it would be quite a great report considering the lingering fears on growth at this given moment, but as a reminder, Powell had stated at FOMC that the breakeven for jobs is within the 0-50k range hence 51k is above the upper-end & is more so a signal that the economy is still likely slowing but it’s likely more so attributed to normalization within the labor market due to the immigration factors which we’ve now highlighted several times for the last few months along with AI likely starting to have an impact on the job market as well. And let’s just say hypothetically that the jobs # were to come in negative, we’ll call it -15k, I’d still argue that the # wouldn’t necessarily be considered ‘soft’ enough to bring about recessionary worries given it’s just barely below Powell’s breakeven range that he had highlighted at FOMC, but instead, do think the UER will remain much more important in terms of paying attention toward as it’s already distorted due to a tightening of labor supply hence IF we do see a meaningful uptick (Call it 4.5%), that’s a bigger signal of a labor market that is in fact materially weakening & could potentially start to stir up recessionary worries rather than just the recent & continued slowing growth concerns.

But in the meantime & as long as recent & continued slowing growth concerns remain, as Powell had stated at this recent FOMC but inflation in general is expected to be a one-time price shock rather than persistent whereas the labor market deteriorating further more so remains as the bigger risk & further weakness from current levels remains unwanted (Fed put is active).

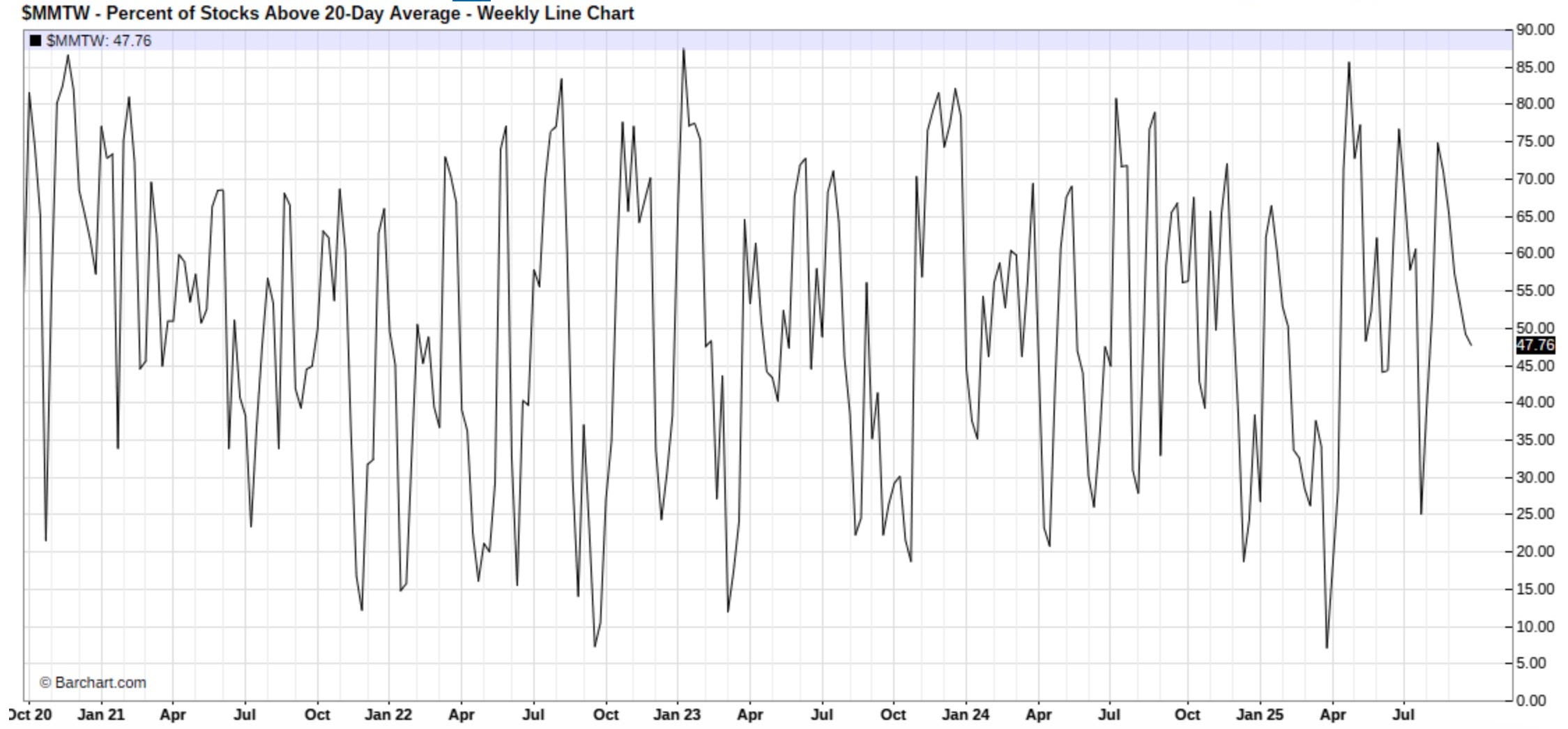

Moving along into the indices, there isn’t necessarily TOO much to discuss as all of the indices are essentially sitting near & or are at ATHs (Another new ATH made on Spooz today) but the most interesting factor continues to be the rotations under the hood which has more or less helped keep the indices bifurcated & has more so led for a correction via time rather than price & a pretty clear example of that is despite all of the indices sitting at & or near ATHs, the % of stocks above the 20D still sits at just 47% which more so points to a market that isn’t necessarily entirely overbought in the shorter-term & instead remains at more ‘neutral’ conditions & the main reasoning in terms of why this is happening is because one day, Small-caps / Cyclicals are outperforming & then the next day it’s Tech & or the AI-trade & the day after that it’s rotation back to Small-caps & Cyclicals & so on… general point being, the distortion is more so due to the continued dispersion / underlying rotation within the indices rather than ‘everything’ rallying all at once.

And in speaking about the indices, the feared & ‘treacherous’ September seasonality didn’t hold true:

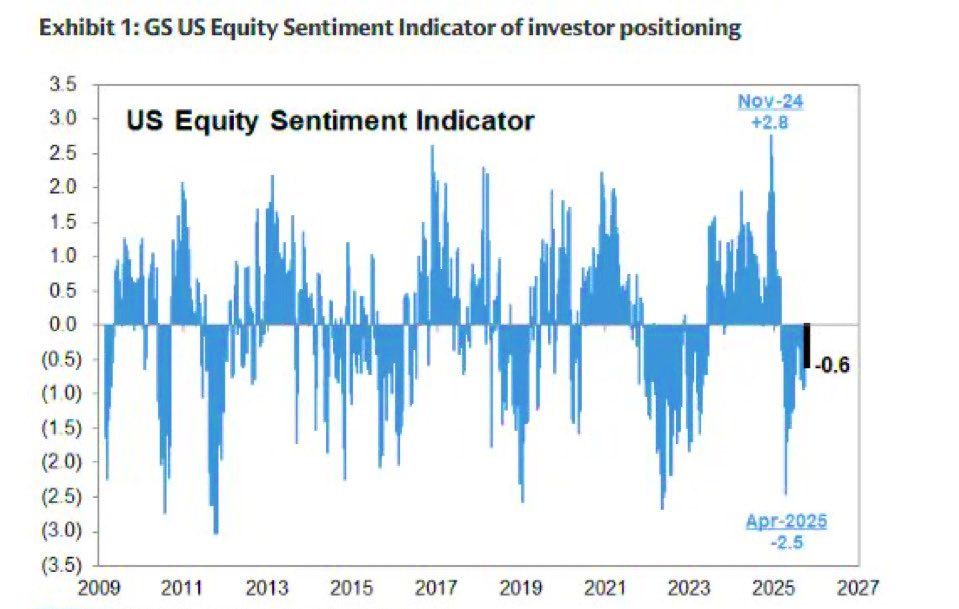

And even with indices continuing to slow churn / grind higher to new highs despite ‘weak’ seasonality, it’s continued to be met with doubts as GS recently reported yet another negative equity sentiment reading which makes it the 3rd longest stretch of negative readings since ‘15…

Why does this positioning standpoint matter even more here? Well, we’re in the final stretch of the year with Q4 finally in action & in terms of seasonality, October can be mixed although leans positive whereas as we near November through December, that’s when positive seasonality really picks up. Again, why is this worth paying attention to into Q4, especially this year specifically? Well, as we’ve talked about since April endlessly but despite Spooz & the general indices sitting near ATHs, institutional investor positioning STILL remains relatively LIGHT & again, this is the 3rd longest streak on record in regards to consecutive negative readings in the history of the Sentiment Indicator data set which dates back to ‘15. When individuals have discussed positioning, they’ve only brought up systematics as they’re quite full in length but of course they are… CTAs for example are trend followers & what’s the market been doing since April? Trending UP nonstop in a slow churn / grind higher pattern so why wouldn’t they be very long here? Whereas HFs / Discretionary have instead remained UW equities in hopes of a pullback / another entry as they de-grossed their exposure into the April lows & failed to jump back in with exposure in full following the administrations pivot. In taking a simplistic view, how do you think their clients will feel if they find out they’ve been not only UW equities but also under-performing the indices on the year (Whilst paying a fee)? Again, pressure is going to start to mount through year-end if there is no material pullback to derail this continued pattern of dips being shallow and bought in a trending upward market & the potential Q4 chase could be another tailwind for equities. And in terms of what can derail the potential chase, again, I’d argue to break the pattern of dips remaining shallow & bought, we’d have to see a correction more than the standard 3-5% range & it likely would have to be attributed to slowing growth concerns instead turning into recessionary fears.