The Week Ahead 12/30/24

Hello All,

I hope you all are enjoying the weekend and getting some time away from the screens & have had a great Q4 as we narrow down to the last week of ‘24 before we get ready to head into ‘25.

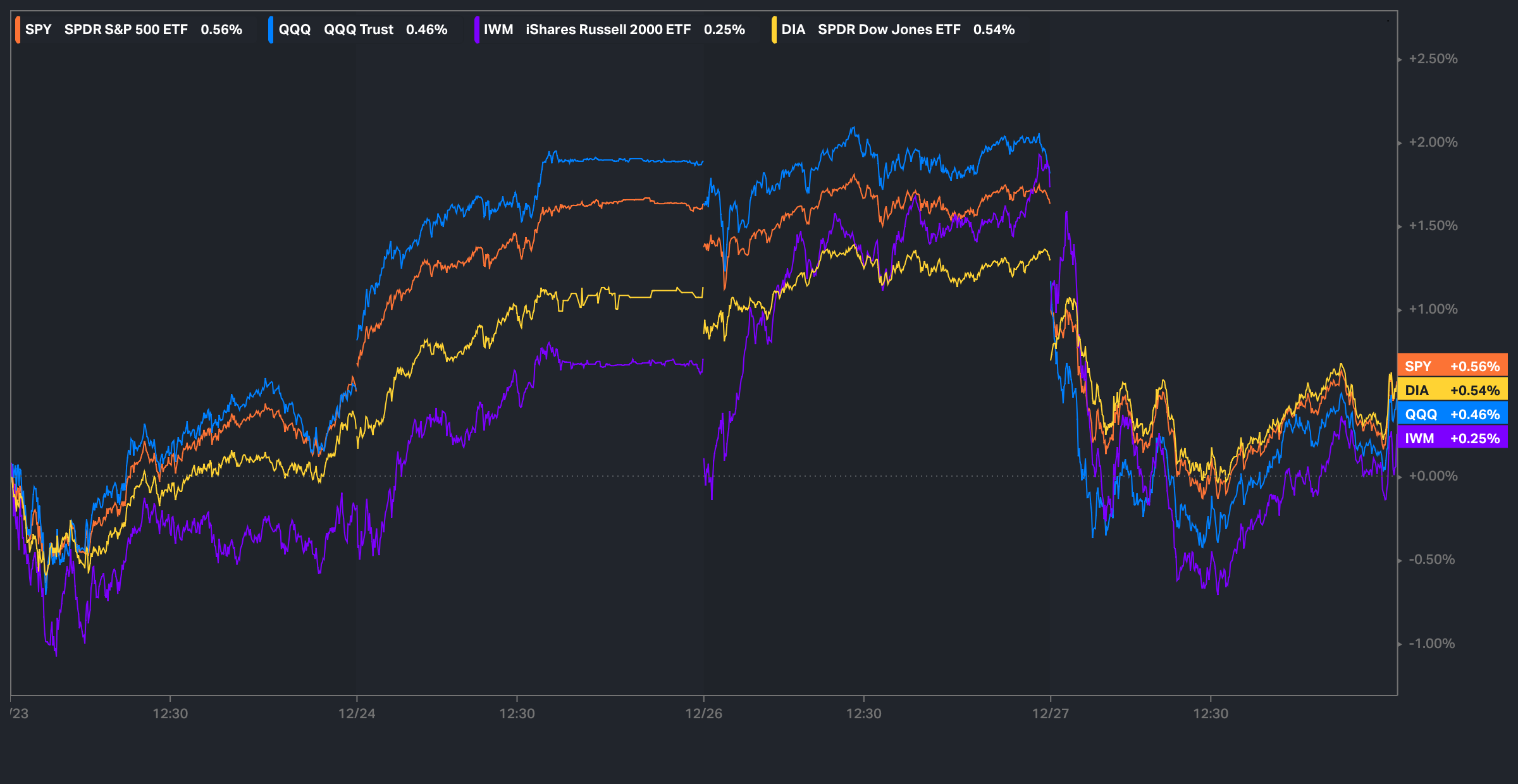

This past week ended up being a quieter week altogether due to the holiday volumes / lack of significant economic data & all of the indices closed fairly in-line up around 40-50bps on the week, but we did see the indices on Friday give back a large portion of the weeks gains & the losses weren’t necessarily derived from any news specifically… could’ve been triggered due to the large pension rebalance / lower volume & illiquidity across the board / term-premium kicking in for risk assets, but otherwise, nothing necessarily specific & do expect similar holiday volumes this coming week as well, but after this upcoming week, we should start to see volumes pick back up as ‘25 kicks off.

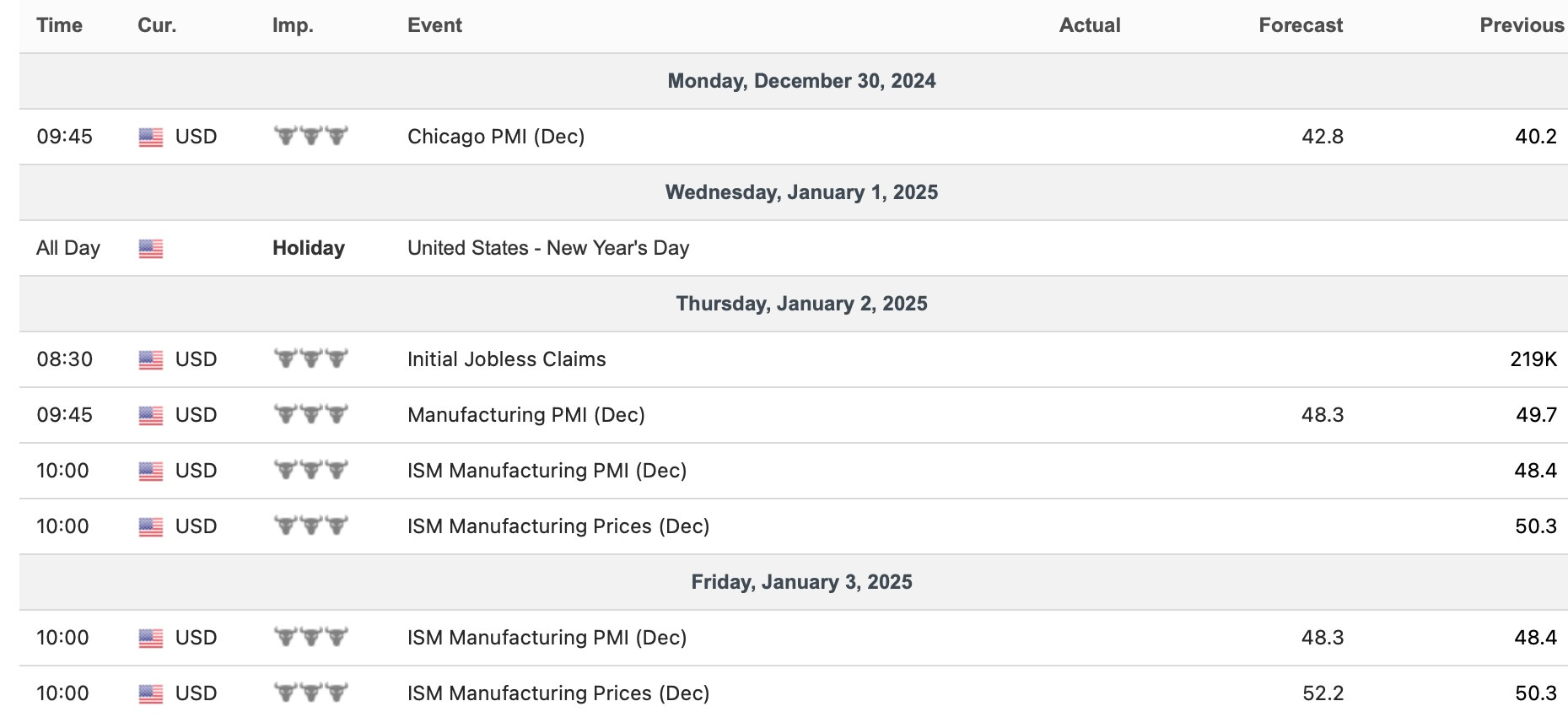

- Economic Data for the Coming Week:

Again, another holiday week is upon with New Years & ‘25 around the corner, so its generally a quieter week altogether in regard to economic data as we just have the standard jobless claims report on Thursday along with PMIs / ISM #’s throughout the week & lastly, markets will be closed on Wednesday for the holiday for New Years Day.

- STD Channels on Indices for Perspective: Daily TF

- SPY

- QQQ

- IWM

- DJIA

Since starting this Substack back in June of ‘23, between individual names / tactical trades / baskets, we have netted a 98.62% return whilst in the same period, the Q's have returned 47.55% / Spooz has returned 40.74% / Dow has returned 30.98% & Small-caps have returned 25.52%, so nice outperformance against all the indices whilst having a 81.3% win rate, averaging a 19% return on realized gains / winners & a 11.33% loss on realized losses / losers.

Looking forward to the future as we wrap up ‘24 & get ready to head into ‘25.

We recently published our ‘25 Outlook / Year Ahead which has a plethora of coverage on a wide variety of topics / themes as we get ready to head into ‘25 after coming off a strong ‘24 & for those who would like to read & prep for ‘25, I included a link to the report / write-up here.

Lastly, I published an educational post as it had been highly requested. Below is the broad range of topics that were included and requested by subscribers:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the educational write-up can be found here.

Educational Piece Part DEUX, which has been highly requested, will be published by beginning of January, likely first week of January.

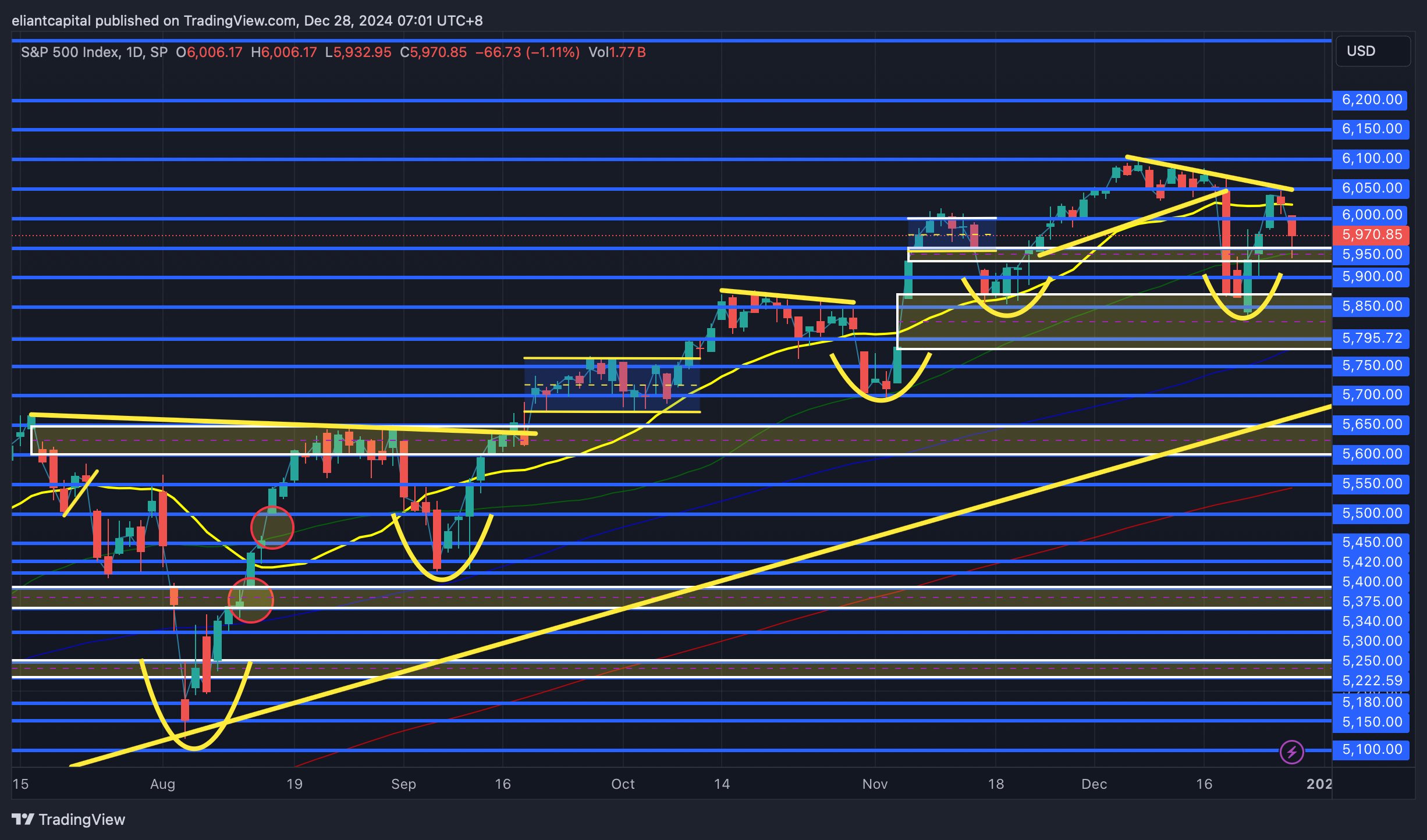

- SPY

In looking at Spooz as we get ready to head into the last couple of days of ‘24 before we head into ‘25, I think the big question from here (keeping in mind last week was a holiday week so hard to put too much weight on price action), but the biggest question is whether or not the indices put in a lower high on Friday this past week. The indices ended up finishing slightly higher on the week altogether, but we had a decent red-day on Friday which wasn’t driven by any news specifically… maybe in part due to the large pension rebalance / term-premium kicking in for risk assets / equities / individuals booking gains to close out the year etc… again, not a specific answer in regard to what derived Friday’s action, but I more so lean it likely had to do with the large pension rebalance & the bond reversal underway that ended up getting completely faded on Friday to close the week out, so that likely weighed in on equites as well.

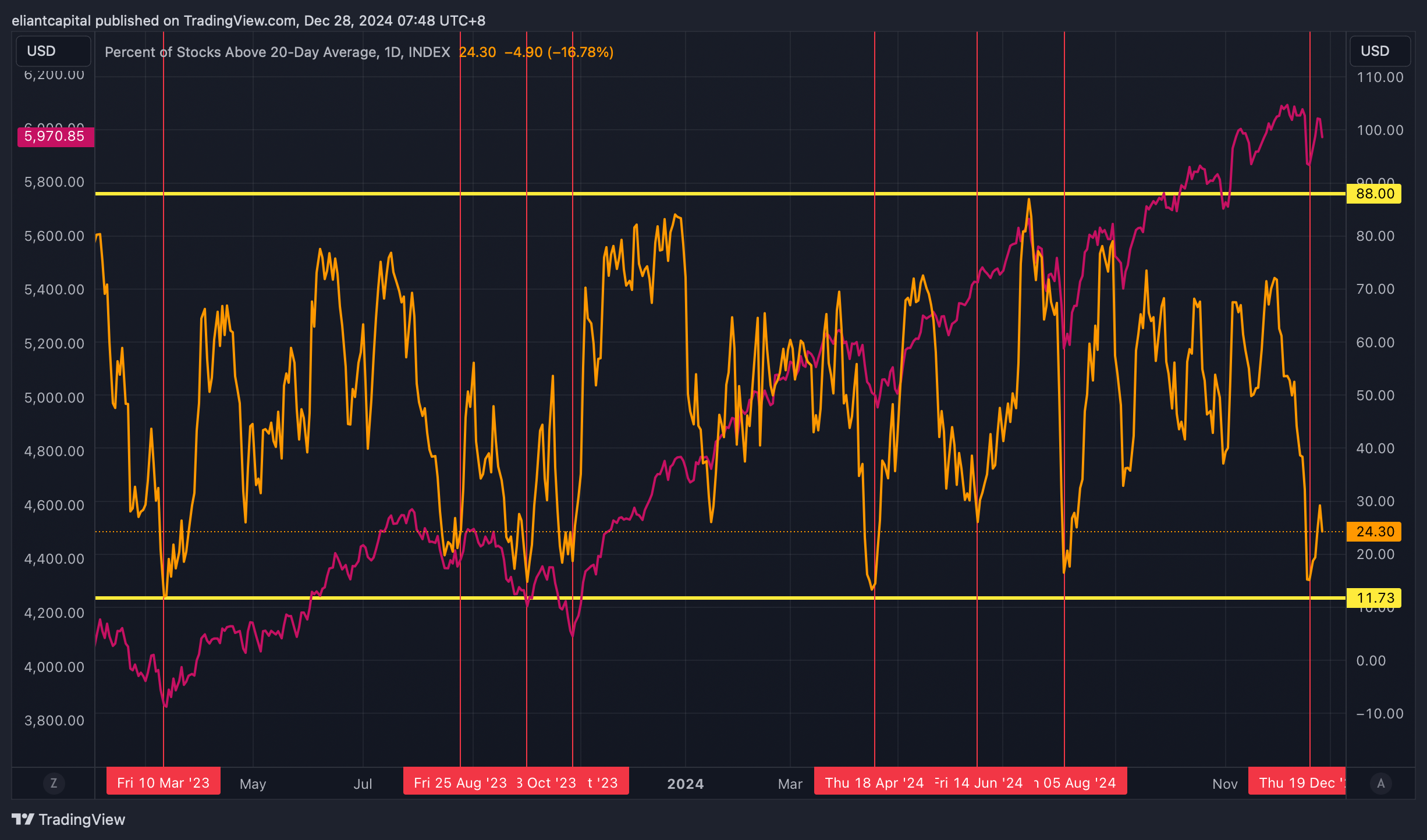

The markets started to get off the mat this past week as the % of stocks above the 20D ticked up a decent bit off the lows (still remains well in oversold territory), but it seems that until bonds can sustain a rally / reversion higher, we may continue to see this lethargic action in markets although given current signals whether it be current sentiment on bonds / dollar being super stretched as we covered last week / % of stocks above 20D / 50D being well in oversold territory, it more so seems like we’re a catalyst / datapoint away from seeing quite the unwinds across several complexes… perhaps in January?

Same story with the % of stocks above the 50D, but we’re essentially at lows on the year in regard to oversold territory (even below the August flash crash levels), but not quite to late ‘23 levels.

Again, the question on Spooz / indices specifically is whether or not a lower high was put in on Friday… Spooz did end up bouncing right off the 50d nearly to the tick whilst holding the highlighted demand zone below for added confluence, but ultimately, I think we need to see bulls firm up above the 20d / 6050ish to start to work back towards highs / new ATHs which that action would likely be derived from an uptick in breadth / expansion, but otherwise, if the 50d falters below (again, held on Friday to the tick), we could go on to retest these local lows around mid-5800s & if bonds don’t let up / pressure remains on the upside on the 10Y, it wouldn’t surprise me if we fill the gap below (election bull-gap) into the Mid / Upper-5700s which also coincides with the 100d & I think theres fairly good odds that those levels could act as a bigger interim / medium-term bottom.

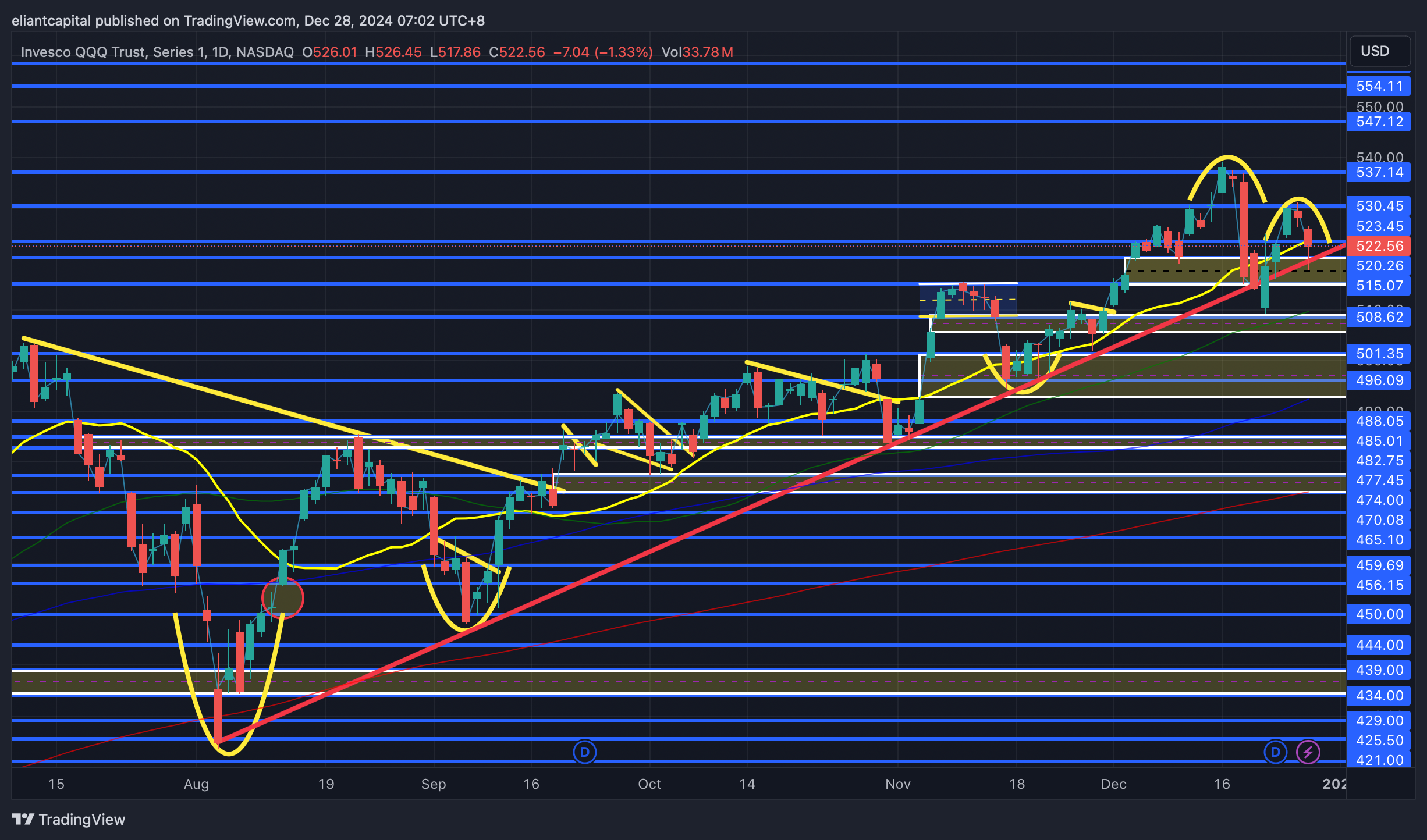

- QQQ

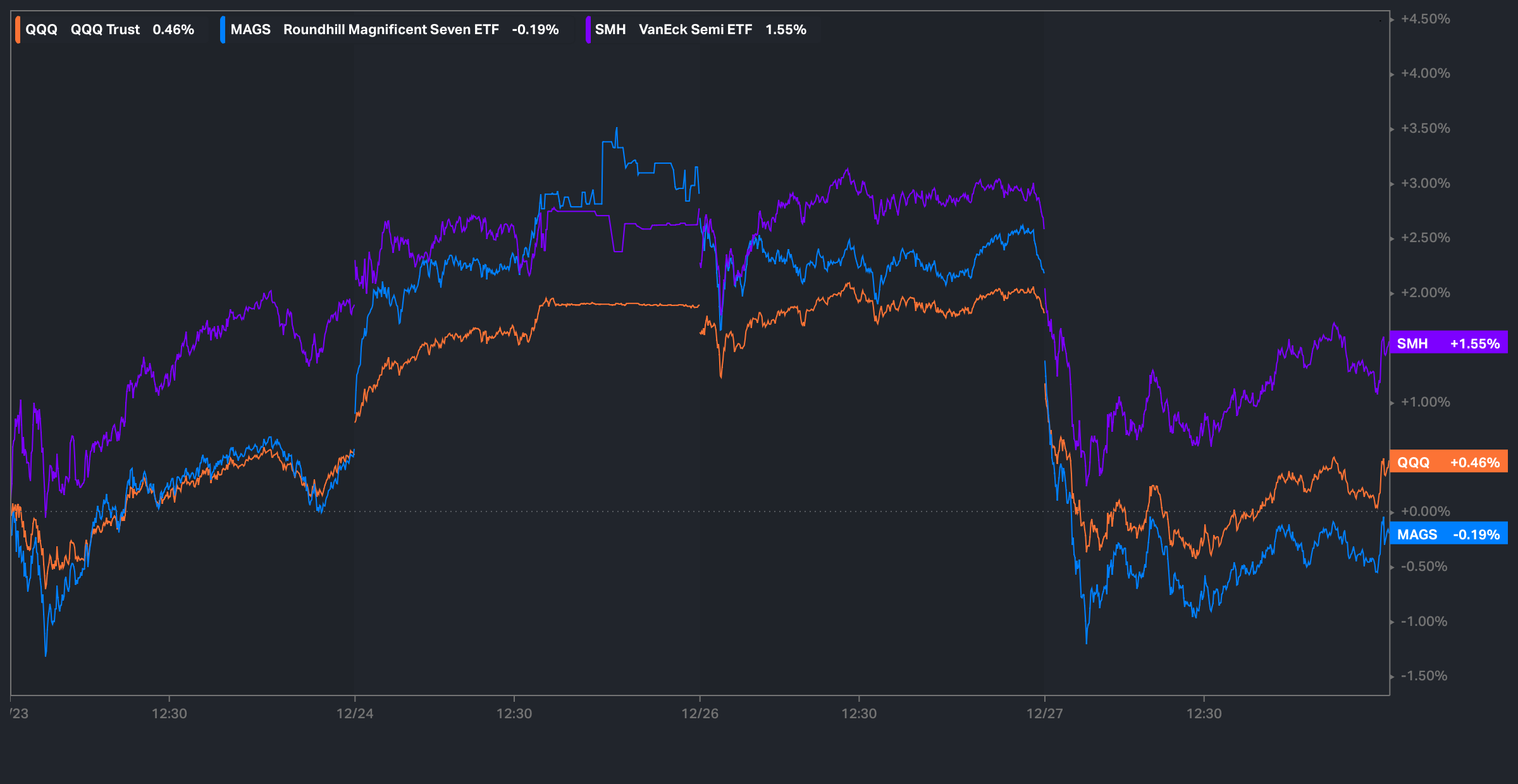

The Q’s ended up finishing off the week on a quiet note, closing up around 40bps after being up over 200bps on the week at one point & majority of the strength came from a select few Mag-7 names along with semiconductors as well.

The Q’s ended up closing the week out just slightly above this support TL dating back to the August lows which has held & acted as support in several instances prior whilst also closing the week out right on the 20d as well.

Fairly simple moving into next week / ‘25, but I think the big question is whether or not the Q’s put in a lower high this past week which could signal a potential retest of the local lows below made the other week near the 50d (508ish) & or if this support TL dating back to the August lows once again comes in and acts as support along with the 50d which then allows the Q’s to go on and invalidate this lower high put in last week to then go on and trek for new highs.

If we were to see this support TL below falter along with the 50d / most recent local lows, I think we could see the Q’s trek lower towards the election gap / 100d (mid-490s) before finding a more firm support, but otherwise, have to assume bulls remain with edge given the 20d has remained supportive along with this TL dating back to the August lows, but again, the one cautionary sign is the fact the Q’s put in a lower high this past week & failed to get any traction above 530s, so bulls would like to see that lower high invalidated fairly quickly, as otherwise, we could see the Q’s pullback a bit more & that could even be led by capital rotating out of the Q’s into other sectors / indices allowing for a bit of a cooldown / consolidation given recent action / outperformance as of late.

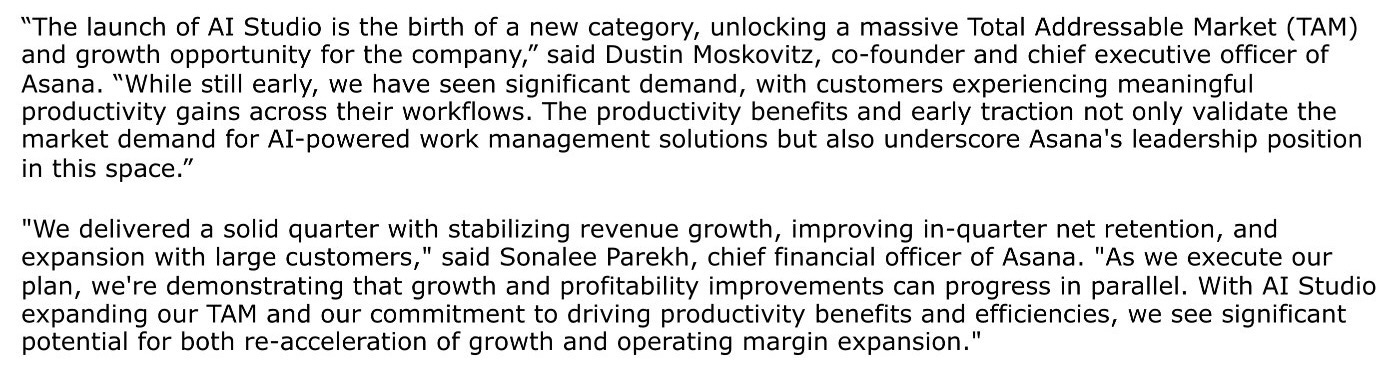

It’s not often you get the “turnaround” phrase thrown around in tech land as it tends to be prioritized to small-caps, but ASAN recently reported earnings & had a large surge as they have been counted out as an AI / Software loser, but with the recent trend of Ai Agents taking shape / announcement & plans of their launch of AI Studio, they’ve shown that they can partake in the trend & this more so is the “turnaround” narrative at play here…

Some commentary from Mgmt. below from this recent ERs:

Well, what is AI Studio & what’s the hype about?

AI Studio was designed to enable teams to create and deploy AI-driven workflows, known as Smart workflows, directly within the Asana platform.

Key Features:

- No-Code Workflow Creation: Teams can design workflows without programming skills by providing natural language instructions to AI agents.

- AI Integration: AI agents handle tasks such as work intake, planning, execution, and reporting, automating repetitive tasks to enhance productivity.

- Customization: Workflows can be tailored to specific team needs, allowing AI agents to perform designated tasks across various stages of work.

What’s the conclusion? ASAN seems to be a clear beneficiary of the AI Agents trend… again, clear potential for a turnaround here.

In regard to technicals, ASAN has cooled off from the highs ever since the big earnings gap up & has created a PEG setup (post earnings gap). ASAN is trying to work out of a 2+ year base & is currently backtesting the most recent breakout of the base & a big positive would be this prior highlighted zone flipping to demand from prior resistance.

Risk on the setup essentially being a loss of the highlighted demand zone below with interim and extended targets above for a 4.49 risk-reward ratio (long against 19 to target 33).

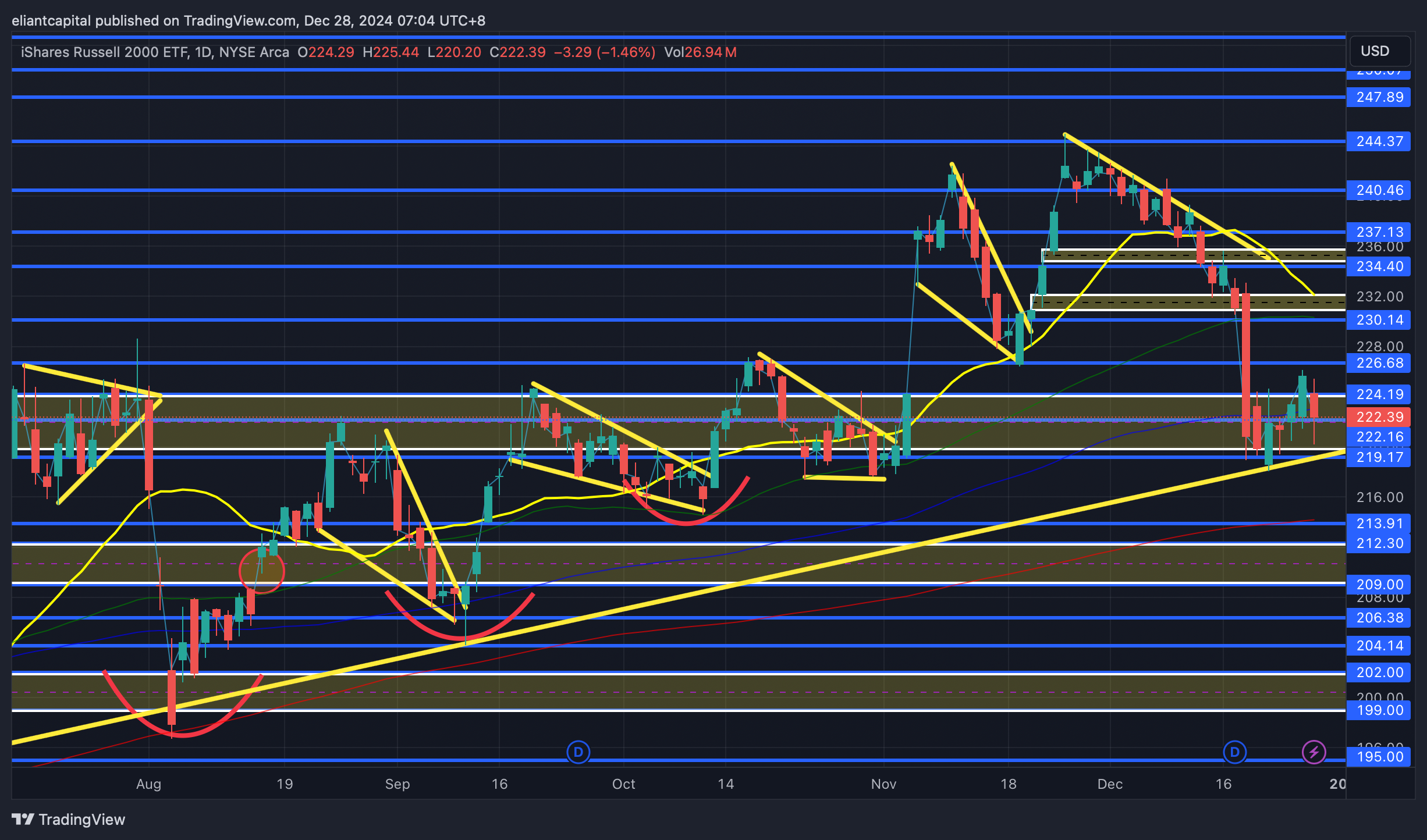

- IWM

Looking ahead into the last remaining days of ‘24 as we get ready to head into ‘25, small-caps have struggled this December (currently down just over 7.5%) & a large part of the underperformance has been driven due to the pressure in bonds / relentless upside on the 10Y & as you can see below, correlation has essentially been 1:1 between small-caps / bonds for nearly the entirety of December.

For some sort of sustainable rally in small-caps, we likely need to see some pressure relieve from bonds, as otherwise, this underperformance will likely persist (keeping in mind sentiment is very stretched on bonds down here & they are a catalyst / data-point away from flipping & unwinding the negative sentiment).

Small-caps still ended up closing out the week above the support TL dating back to the late ‘23 lows & it has acted as support in several instances prior & it remains a key point of confluence along with small-caps sitting on the 20wk as well which has pretty much acted as support for the entirety of the year.

If we were to see bonds stabilize around these levels / potentially revert higher as small-caps hold this area of confluence (support TL dating back to late ‘23 lows / 20wk / 100d), I think we could see small-caps mean revert higher towards 230ish (20d / 50d) before potentially being met with resistance & for further upside to start to work back up towards the highs, I think we will need more firm confirmation that this recent blip in inflation was indeed a blip & disinflation is now back intact along with economic data continuing to be generally supportive as well (goldilocks).

On the contrary, if the pressure in bonds continues / goldilocks data gets invalidated (bad jobs data / higher inflation data), I think we could see IWM flush below this longer-term support TL dating back to the ‘23 lows to go on and retest the 200d below around 213ish which also pretty much coincides with a bigger demand zone (209-212ish highlighted demand zone below), so it generally should be a bigger area of support if it were to be tested. Small-caps do still remain in a trend of higher lows & higher highs & barring recessionary data, I still think small-caps are a favorable risk-reward around these levels, again, given the facts that we’re likely at peak hawkishness & or right about there (need to see disinflation resume in ‘25) / along with the technical confluence lining up as we’ve covered & lastly, a big driver of the selloff as we’ve noted has been due to pressure in bonds & with sentiment remaining stretched, it doesn’t take much to see a complete narrative shift (softer data likely needed) to see a bigger snapback in bonds which would then lead to relief across all markets, but especially small-caps specifically.

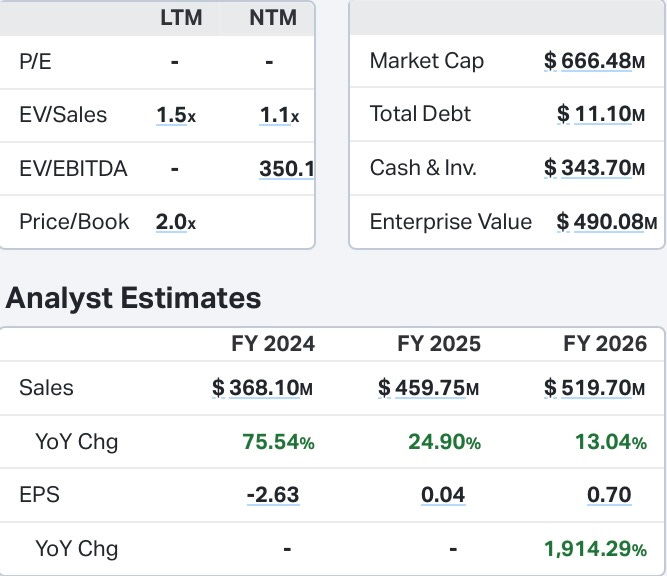

A name we ended up getting long this past week & adding to the rate-cut beneficiary basket was HIPO. We’ve briefly covered this name before in the 16s before it went on to double into the 30s, but it continues to look like HIPO could be poised for a larger turnaround story.

In looking below, theres one big positive to note… HIPO hardly has any debt & they have a plethora of cash & in ‘25, EPS should finish off positive along with #’s continuing to accelerate as well.

For those completely unfamiliar with HIPO, Hippo is a home protection company that offers homeowners insurance and related services in the United States.

The company operates through three segments:

Services: Offers home maintenance and other related services.

Insurance-as-a-Service: Provides insurance products through partnerships.

Hippo Home Insurance Program: Directly underwrites homeowners insurance policies.

Hippo's approach includes leveraging real-time data, smart home technology, and a suite of home services to create an integrated home protection platform.

In regard to technicals, it’s about as textbook as it gets… HIPO is currently backtesting an IHS breakout & is flagging into the highlighted demand zone along with the 20wk sitting just below for added confluence… risk on the setup essentially being a loss of the highlighted demand zone / 20wk with interim and extended targets above for a 5.78 risk-reward ratio (long against 23 to target upper-40s).

A great technical setup with another company looking to progress through the “turnaround” phase with a fairly clean balance sheet as #’s look to continue to accelerate as well into ‘25. We’ve seen some wild moves out of other insurance names this year… LMND / ROOT etc… & I don’t see why HIPO can’t continue to see progression as well with potential for a much larger rebound / turnaround as well.

- DIA

The Dow ended up having a modest week this past week, closing up just over 50bps, & action I’d argue was more constructive & we even nearly filled the FOMC gap as well.

Something interesting to point out as we get ready to head into ‘25 is DIA/QQQ looks to be bottoming & potentially forming a higher low... maybe a sign of more rotationary forces underway in ‘25 given how hated value / cyclicals in general are at the moment

In regard to technicals, not much has changed on DIA, but if the local lows below from the other week were to fail / 100d fails to come in as support, I think we could see DIA retrace to 416 / 414ish (November local lows) before finding a more firm support. For firm upside, I think we need to see DIA overtake the FOMC gap highs (50d / 434ish) to start working back up towards 437 / 440ish, where ultimately, a weekly close above that pivot likely leads DIA to trek back towards the highs / go on to make new ATHs into the 450s… similar story as to small-caps / general markets outside of Mag-7, but do think we need to see bonds stabilize / find a bid for capital to rotate elsewhere outside of Mag-7, as otherwise, this lethargic action without a real & sustainable bounce may persist.

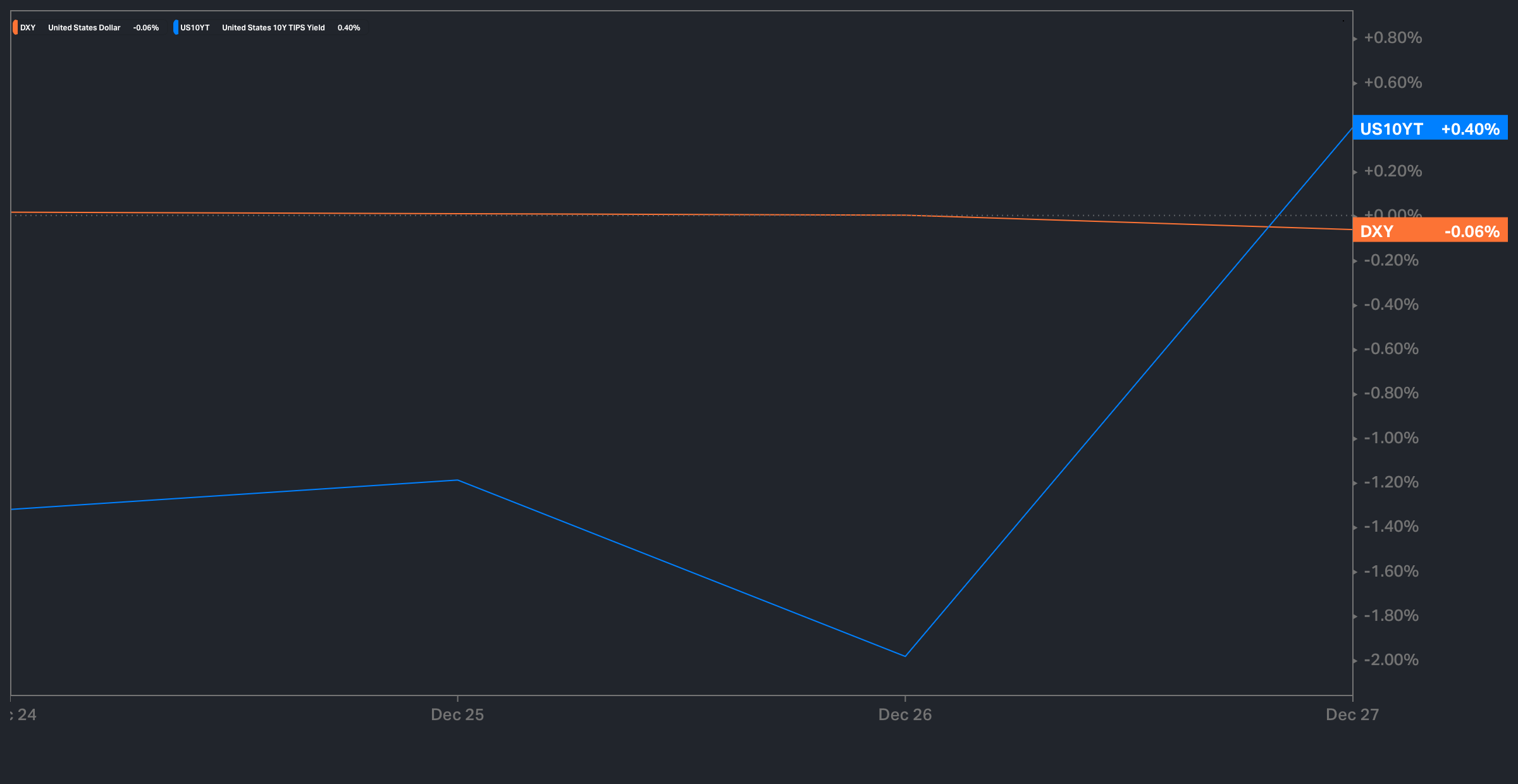

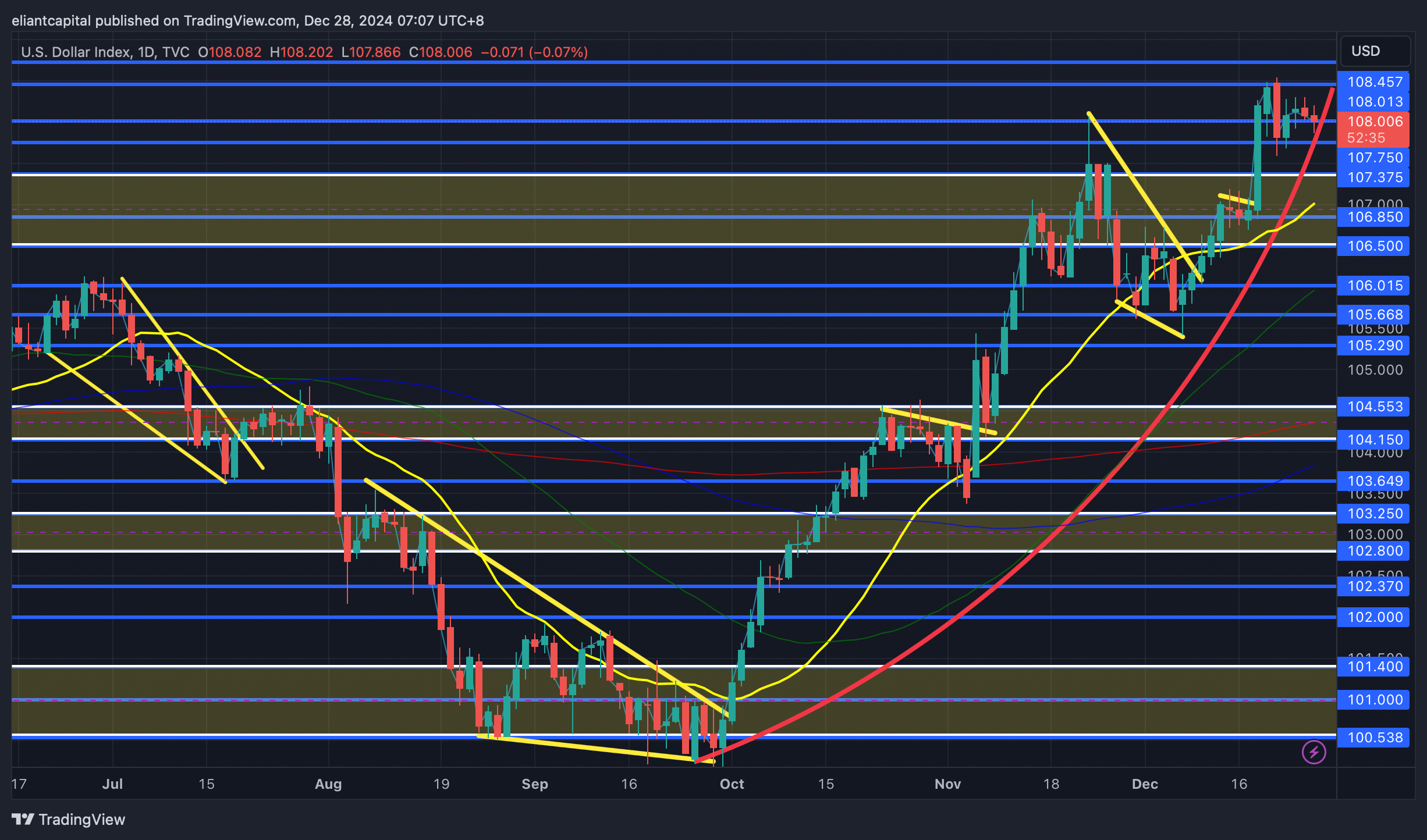

/DXY

The dollar did a whole lot of nothing this past week given we didn’t have much economic data, but it did end up closing a tick lower, -6bps on the week so essentially flat. Heading into this upcoming week, its a slight holiday week given its New Years week (markets closed Wednesday) / first week of ‘25 as well & we don’t have much data at all besides the standard jobless claims report on Thursday along with PMIs / ISM #’s throughout the week as well.

Looking back at this past week, again, the dollar essentially closed flat on the week, but the 10Y ended up closing higher & even tried to stage two intraday reversals after bonds ended up having large bounces off the lows, but both reversals couldn't sustain & we ended up seeing bonds close on the lows on the week whereas the dollar closed slightly off the highs so a TAD divergence, but nothing too notable… especially considering it was a holiday week.

Again, the question into ‘25 is whether or not the recent dollar breakout of the 3+ year range proves to be a false one or a firm one. Maybe the dollar has a tad bit more upside (does feel like its trying to stall out here), but given the fact that we’ve pretty much reached peak hawkishness / sentiment is stretched (of course barring a scorching inflation print), it does seem like the dollar has priced in quite a bit of pessimism against other currencies & oddly enough, when Trump was elected in ‘16, the dollar ran up into the end of the year before peaking right into ‘17 & declining 14%+ that following year.

Again, not much has changed on the dollar since last week as it essentially closed flat, but ultimately, for any sort of firm downside, we need to see the dollar lose 107ish / 20d to start to work lower out of this parabolic move it has had off the lows, but otherwise, the dollar will likely be supported in the interim (as long as 106.5 / 106.85s remains bid).

Again, we don’t have much economic data at all of significance this upcoming week & the next bigger datapoints will be the upcoming jobs report in January along with the next CPI / inflation reports. As we’ve discussed previously, but the fed gave themselves very little room for error (essentially projected inflation to trend higher & the UER to remain contained at 4.3), so if disinflation starts to resume & or the UER ticks up past 4.3 to the 4.4s & so on, the Fed is going to look quite foolish… maybe thats the expectations they wanted as it then allows the Fed to have a TON of wiggle room to be accommodative given current expectations are priced in such a hawkish manner… we’ll have a better gauge post January data / FOMC in regard to if the Fed made another mistake with their hawkish cut & or if it was indeed warranted.

/TNX

Bonds ended up having another sluggish week & they even staged two large intraday reversals in what looked to be a nice bottoming process, but the lows ended up getting taken out on Friday & bonds ended up closing on the lows for the week.

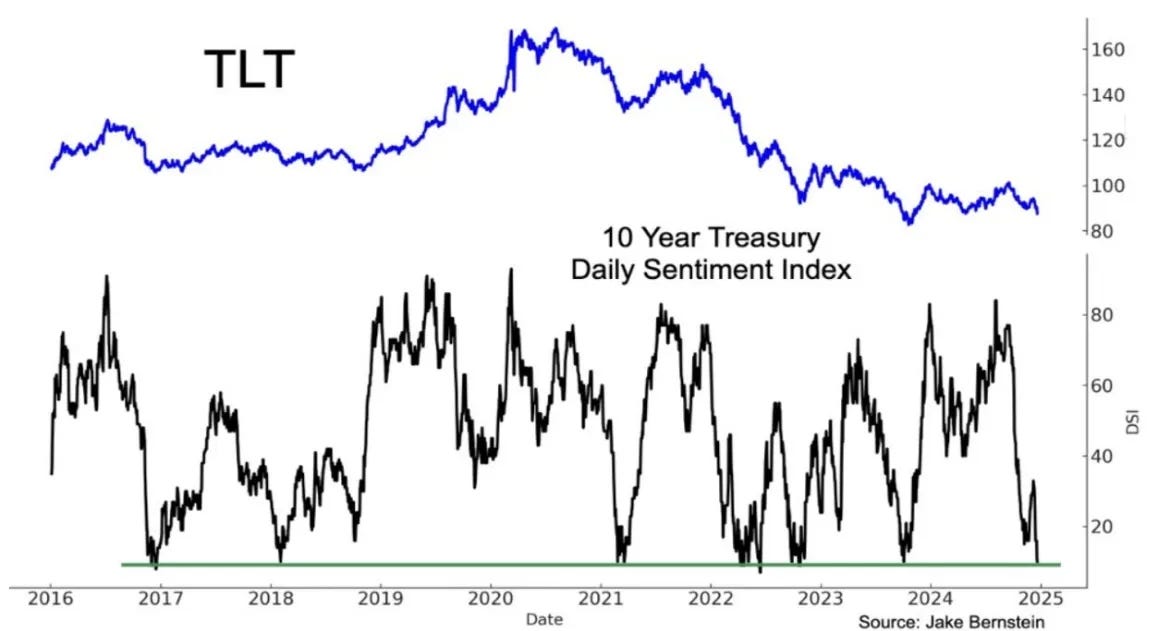

As we covered in the last week ahead, but to reiterate, the boat is very lop-sided on bonds here, & as we’ve seen in the past, it doesn’t take much for narratives to start changing & for the boat to flip the other direction… I do think the biggest factor to get a more sustainable bid in bonds is likely going to be due to inflation fears being put to rest (this recent blip does indeed prove to be a blip & disinflation starts to resume in ‘25) & or we see the Fed once again misjudge the markets as the UER ticks up further above their ‘25 estimates to 4.4+… disinflation resuming would be the biggest positive (as long as inflation doesn’t start to drop off too much as then deflation fears will appear), but the UER ticking up to 4.4+ very much so could spook the market just as it did in early August of this year as we all know, but there hasn’t been any screaming signals that labor is drastically cooling off… more so just the same normalization with the labor market generally remaining intact across the board.

The breakout in the 10Y continued this past week & the question continues to be if this breakout ends up being a true breakout to test the late ‘23 highs / potentially even higher towards 5.2s & or if this ends up being a fake breakout before resolving lower. Again, we don’t have much economic data at all this coming week & the next bigger datapoints won’t be until the next jobs report / CPI data, but the one recent positive for bonds is auctions have actually gone fairly well as of late & thats actually what led to the intraday reversals this past week in bonds, but as we mentioned earlier, the pops ended up getting faded as bond bears still remain in control & it seems that until we see disinflation start to resume & or real economic weakness starts to set in, bond bears will likely continue to press until a change of narrative is at hand.

The 10Y is essentially back to the early ‘24 spring highs… don’t expect this to be an easy level for the 10Y to overcome & if it does keep a lid on the 10Y around these levels, I think we could be due for some quick reversion in January towards 4.5 / 4.4ish range, but again, to get a more sustainable bid in bonds, we likely need to see the Fed’s worries of inflation subside which would be due to softer inflation data & or we need to see weakening in the labor market / uptick in the UER to get the narrative shift going back towards the other way. With how negative sentiment is into ‘25 & bonds being negative now for the past few years, it does seem like ‘25 could finally be a positive year for bonds.

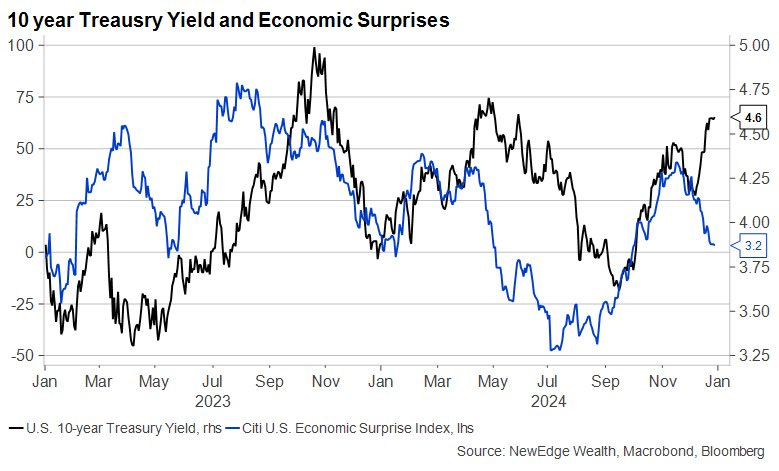

Thought this was an interesting chart from @CameronDawson, but it essentially shows the divergence between the 10Y / Economic surprise index & as we’ve discussed earlier & previously, but it seems pretty clear that the Fed could be too ambitious on focusing on inflation over growth given they gave themselves very little room for error (UER essentially needs to remain contained at 4.3 which is where it sits now) as otherwise, the Fed could end up looking quite foolish in ‘25 & this divergence may already be signaling that.

/CL

Another quiet week for crude this past week as it continues to remain rangebound for nearly 4+ months now. Again, not much has changed on crude as the range continues to remain very tight between 67 / 72ish, but it does continue to look like crude is basing before breaking higher rather than consolidating before breaking lower given how supportive 65 / 67ish has been, but ultimately for a firm breakout, we need to see crude overcome 72 / bbl. which then likely sets crude up for a test of 74 / 75.35ish (testing the 200d from below), but otherwise, this rangebound action may persist.

As we’ve noted, but despite crude being in this base formation, energy stocks have still been underperforming drastically against tech (funding short aspect) & XLE/QQQ has now pretty much retraced the entire ‘21 - ‘23 rally… feels like a similar setup in energy as it did in January earlier this year, but still likely need to see some sort of fuse to light the trade and get it going… China Stimulus? Geopolitical Issues? Rotation out of tech to value / cyclicals? Again, many possibilities, but barring a recession / serious slowdown, energy stocks look well setup for at least some reversion into ‘25.

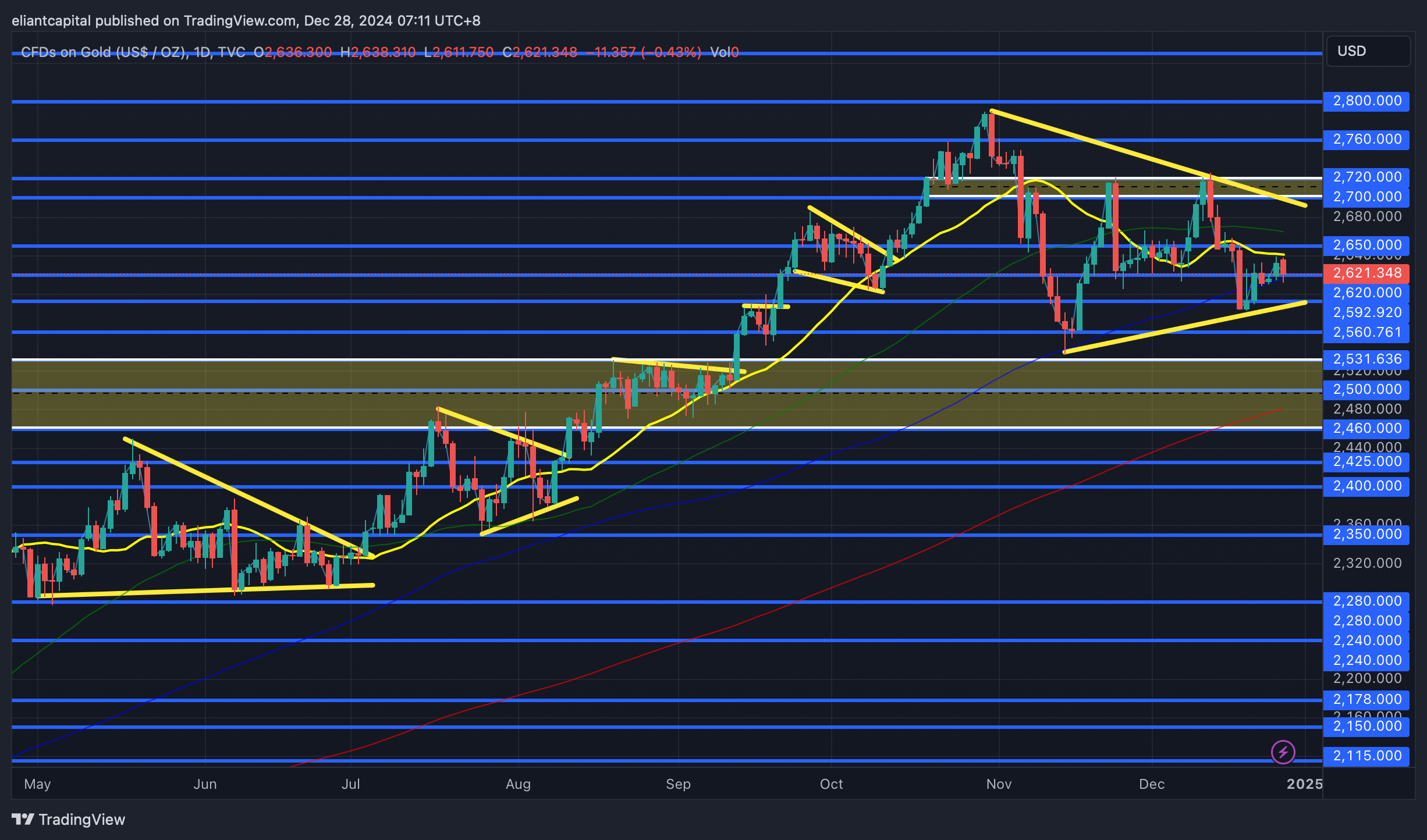

/GC

Not too much action in gold this past week, & as we discussed earlier, but the dollar was flat on the week, but one thing to point out & as we’ve discussed previously, but despite the continued rally in the dollar, gold in itself has held up very well (although miners not so much as majority have corrected 7-10%+ from highs / in-line with recent small-cap underperformance).

Gold is still building out a wedge pattern (although does remain below the 20d as of now)… but similar to what we saw in the summer before we saw continuation higher (July / August TF), Gold looks to be consolidating before a move higher, but we do still need to see gold firm up above 2720 / 2700ish to start working back up towards the highs / new highs into 2800+ as otherwise, we may be susceptible to more rangebound action, potentially even see gold break lower towards 2530 / 2500ish (200d) before finding a more firm bottom.

If recent hawkish pricing is indeed not warranted, we likely will see quite the surge higher in gold whereas if jobs / inflation data does continue to come in hotter than expected & the Fed continues to keep up with the hawkish tone, I do think thats the ultimate downside trigger for gold / metals & we could see a bit of an unwind of the ‘24 move, but again, if the hawkish pricing isn’t warranted / dollar & bonds start to revert, we likely will see a snapback in gold right towards the highs & likely onwards to 3k+ as the debt situation in the U.S. is not improving & DOGE has already proven that they likely won’t make much of a dent in reducing spending (I’ll believe when I see it kind of thing).

/SI

Silver ended up having a quieter week as well this past week & silver ended up closing the week out just slightly above the 200d / right on 30 / oz. essentially. Continue to think this 28.4 - 30 / oz. zone on silver should remain supportive & will remain key into ‘25, but if we were to see that zone falter (likely would happen on further reiteration from a hawkish fed due to hotter data driving the dollar higher & or even a deleveraging event), that would undo quite a bit of progress on the bigger picture for silver & we could even see a backtest of the August lows.

In looking at the bigger picture, ultimately, the story hasn’t changed & for further upside, we need to see 35 / oz. (high of year) flip from resistance to support as that would then signal that Silver is ready to start working back up to the ‘11 highs, but otherwise, do think we need to see 28.4 / 30 oz. protected into ‘25 as it essentially coincides with a backtest of this recent 3+ year breakout, as otherwise, this recent move in ‘24 could prove to be a false breakout.