A Turning Point

Hello All,

It’s been a relatively quieter kick-off to the week in terms of economic data & following today’s CPI print, headline ended up coming inline at 2.7% whereas Core came in slightly softer than expected, but despite the generally positive face-value inflation print, concerns arose from the rise in goods inflation as tariffs start to filter through & without the decline in autos, Core would’ve posted quite the jump… participants now will be paying even more attention to July’s set of inflation data.

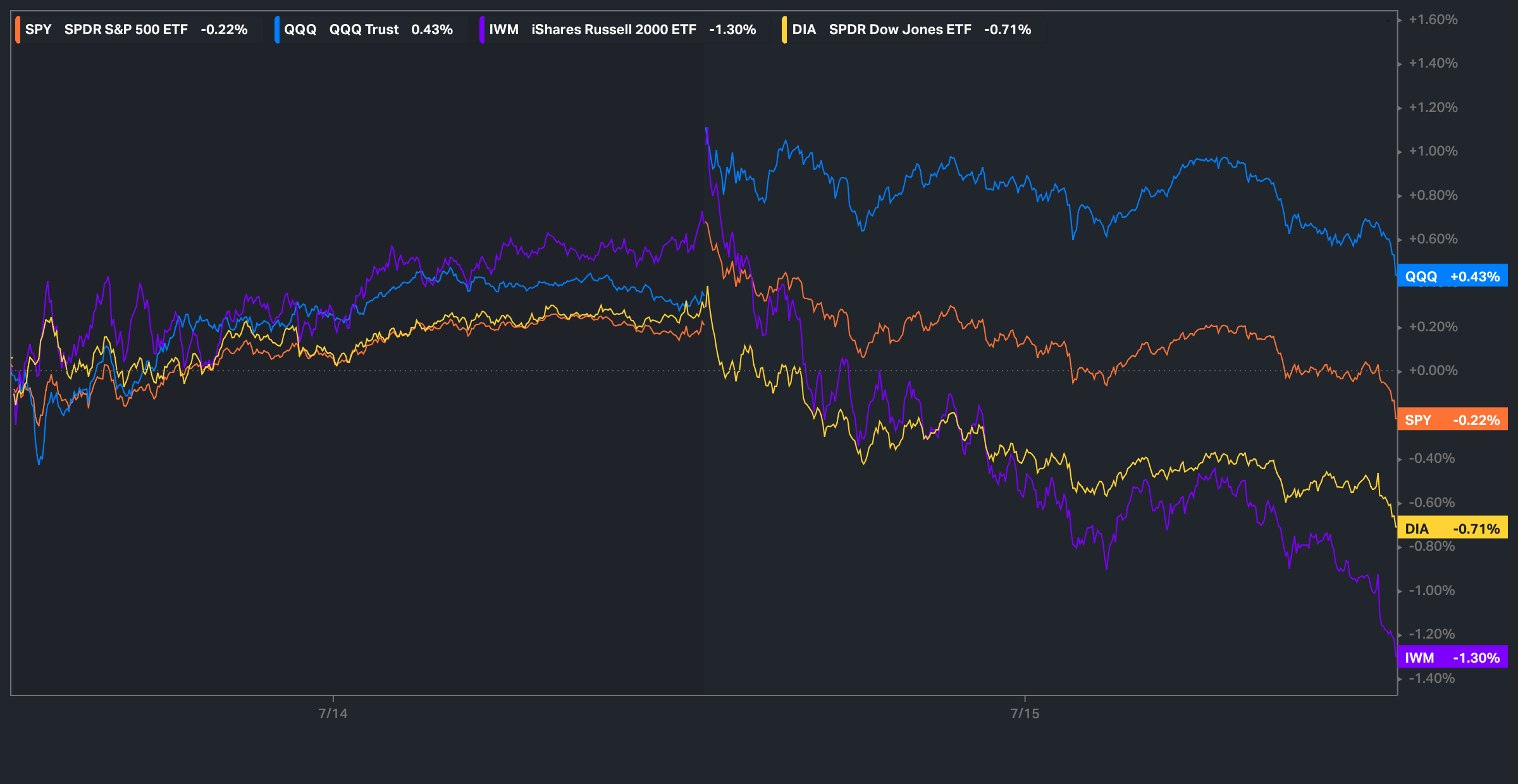

And the other news of today being that the U.S. is allowing Nvidia to sell H20s to China after having been banned in May… following both headlines (CPI & NVDA), the Q’s have thus far been the best performing of the indices, +43bps, whereas small-caps have been the relative laggard, -130bps, with the big contributing factors being the recent pressure in bonds following today’s CPI print along with general liquidity being sucked into Semiconductors / Nvidia / Mag-7 & everything else has since gotten sold.

In April, we wrote about hard assets & the structural framework behind hard assets given recent events & future outlook along with some historical perspective as well… you can check it out below for those whom may have missed… it’s been pretty spot on.

Hard Assets in an Era of Soft Money

As global central banks quietly rearm their stimulus arsenals and fiscal deficits spiral past the point of discipline, the foundations of the global monetary order are beginning to crack. Amid this shift, one question looms larger than ever: Are we on the verge of a new commodity supercycle?

We also published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

- SPY

To jump right into it, it’s generally been a quieter week for Spooz, currently -22bps although there was a bit of vol today following the intraday reversal, but nevertheless, coming into the week markets ended up largely shrugging off the weekend tariff headlines of Trump having threatened both the EU and Mexico with 30% tariffs but given the August 1st deadline, the indices more so took it as there is still room / time for negotiations to take place... And then today, both Spooz & the Q’s pushed to new highs after news broke that Nvidia is expected to receive U.S. approval to resume H20 chip sales to China, following a ban put in place back in May (more on this later), but the gains ended up getting entirely reversed due to poor breadth within the indices & Mag-7 were essentially the only names doing the heavy lifting within the indices whereas majority sectors all got sold.

In terms of the remainder of the week, tomorrow we have PPI #’s & then on Thursday, we have the standard jobless claims report along with retail sales, but in general, its a lighter remainder of the week in regard to economic data.

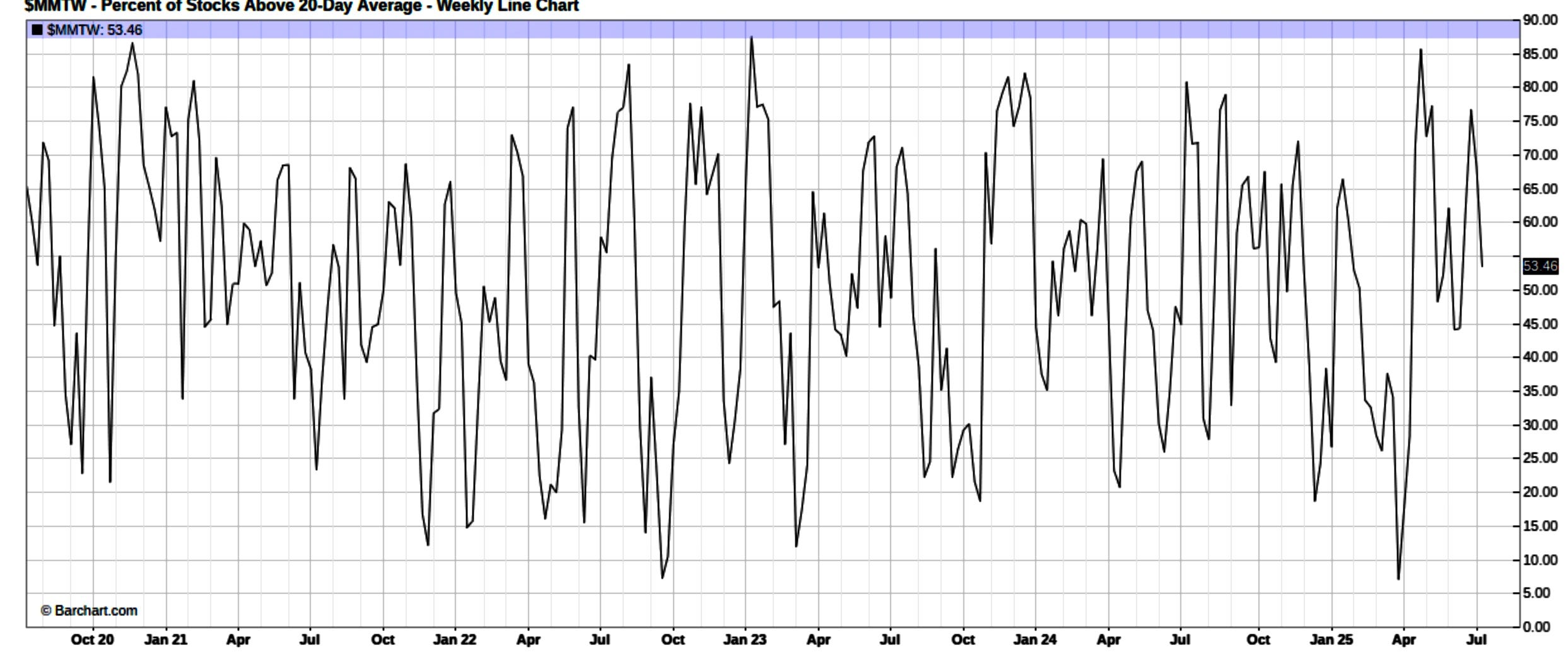

Now, more specifically in regard to the indices but given the general poor breadth that took place within the indices today, we saw a bit of a drop-off in the % of stocks above the 20D which is arguably a ‘good’ sign as it allows recent overbought conditions to reset as conditions move back towards neutral… and a large part of the poor breadth has been due to liquidity being sucked into Semiconductors / Nvidia along with the poor action within bonds following todays CPI print which we’ll talk about more later as well.

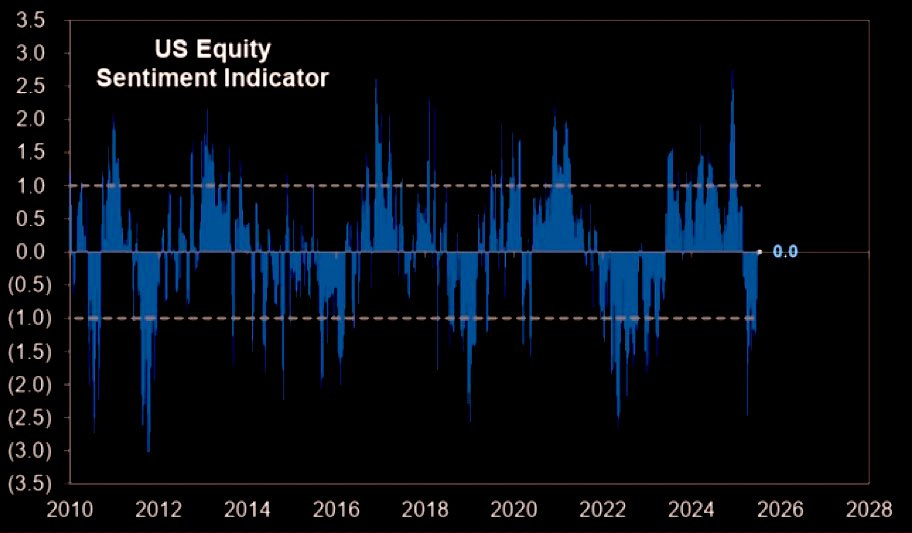

And in terms of positioning, after being UW for over 2+ months, positioning has finally made its way back to neutral although still remains well off the late ‘24 highs following the election… again, just an added testament in terms of upside complacency & likely the only reason positioning has moved up towards neutral is HFs / PMs have been forced to chase due to performance reasons / trying to maintain their job.