Credibility Remains in Question

Hello All,

It’s been a bit of a wild week thus far within the indices… as the week kicked off, markets sold off quite aggressively, granted, the selloff was on lower volume, but nevertheless, markets became flustered as no progress & or deals were made in respect to tariffs, but then it all changed today… initially, markets traded stronger & gapped up in the morning & markets were more so trading as if some news was leaked given the resilience & rebound off yesterdays low & sure enough, we got a headline out of Bessent stating that the current path with China is unsustainable & de-escalation is on the way which then was confirmed after-hours by Trump which has led to a rally in the overnight session / post-market.

As of todays close, the indices are all essentially slightly positive / flat with small-caps currently leading the way as the best performing index as they sit higher by just over 50bps.

This past week, we wrote about hard assets & the structural framework behind hard assets given recent events & future outlook along with some historical perspective as well… you can check it out below for those whom may have missed.

Hard Assets in an Era of Soft Money

As global central banks quietly rearm their stimulus arsenals and fiscal deficits spiral past the point of discipline, the foundations of the global monetary order are beginning to crack. Amid this shift, one question looms larger than ever: Are we on the verge of a new commodity supercycle?

Lastly, recently, we published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

- SPY

As we head into the remainder of the week / April , it boils down to two things:

- Can Spooz / General indices reclaim the 20d?

- Can Spooz / General indices make a new high above the 90-Day Delay Highs?

Given the news after-hours of the Trump walk-back, all of the indices in general will open with large respective gaps & the low made on Monday starts to look more and more like a higher low. For Spooz, what we know as of now is Bulls have a clear LIS to work off of (5100ish) whereas bears need to cap 5450 / 5500ish on the upside to continue to solidify this recent wide-range Spooz & the general indices have remained contained within for these last couple of weeks. Given the gap up tomorrow, as always, the most important factor is the gap-up solidifying & or not getting sold off to create / establish a bull-gap. If the gap-up were to stick, do think bulls need to make a push higher towards the 20d near 5400ish whereas if that is firmly reclaimed, I do think we can see a further sustained move upwards to fill the initial Liberation Day gap in the 5500 / 5575ish range above (gap-fill)… & then from there, I could see Spooz digesting the recent upside move & or very much so rejecting & backtesting lower (retest 5450ish & to flip to support) before then trying to resume higher to work upwards to backtest the 200d near 5700ish which is likely a bigger pause spot for a countertrend rally in Spooz if it were to continue to extend further (although do think a liberation day gap-fill can be cause for significant pause as well).

On the flip side, if we were to see the gap-up sold, I do still think bulls need to maintain 5300 / 5250ish on the downside as support, as otherwise, bulls run the risk of retracing right back towards Monday’s lows near 5100s & typically the third test gives better odds for a break lower leading to a full unwind of the 90-Day Delay move. Likely would be driven by weaker hard data & or a walkback of the walkback which is always a wild card given how frantic the administration has been.

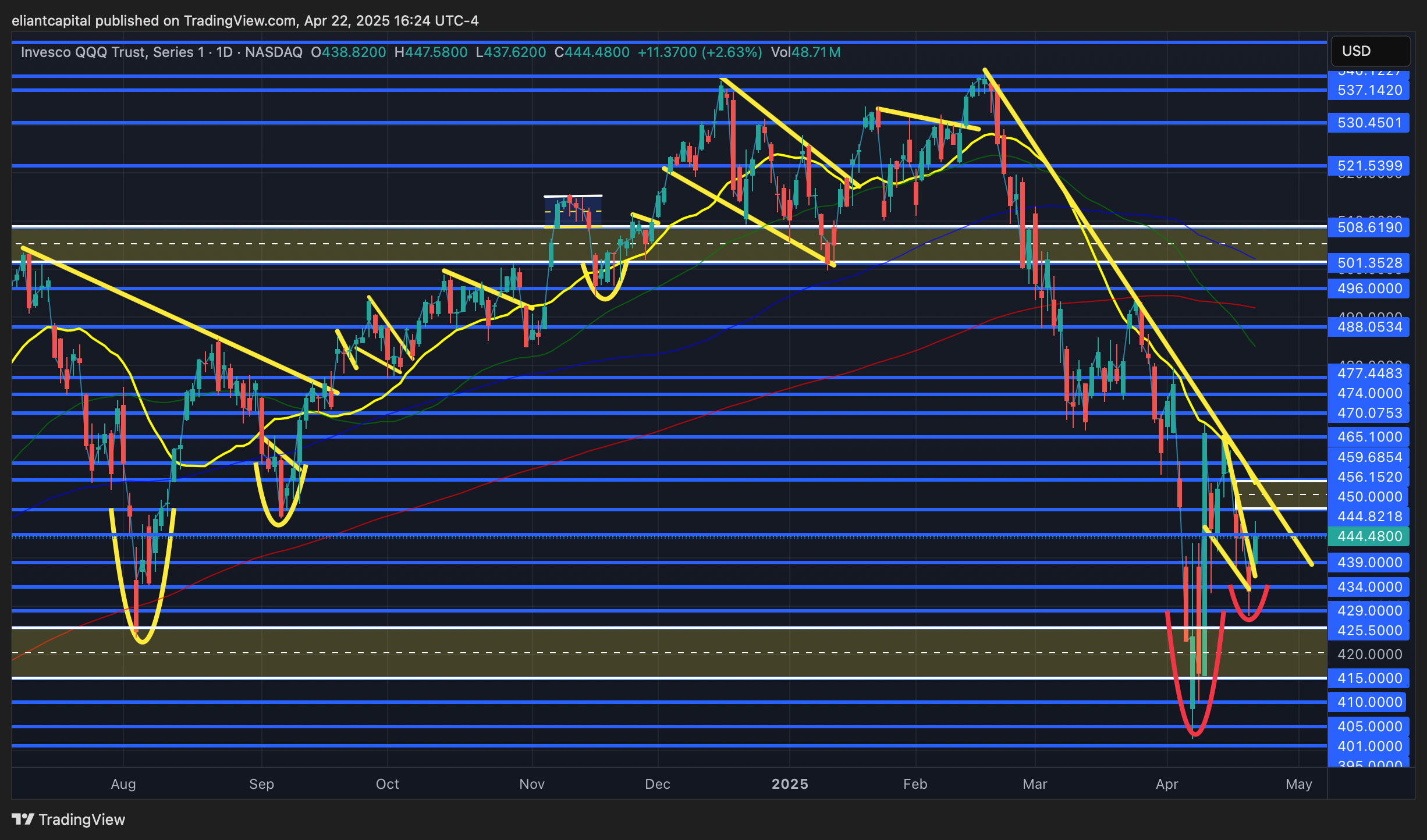

- QQQ

It’s been a wild week altogether & as mentioned above, but do think the biggest factors for the general indices here is if they can firmly reclaim the 20d / make new highs above the 90-Day Delay highs… otherwise, the recent wide-rangebound action may persist.

Nevertheless, action this week thus far has been quite constructive… initially, the indices sold off yesterday due to the lack of progress / announcements on trade-deals & then today, markets completely reversed the entirety of yesterdays sell-off on no news… well, in pre-market, we called out that the indices were clearly trading like some sort of progress / deal was made & sure enough later on in the day, we got news of Bessent calling for China de-escalation & than after-hours today, Trump more so confirmed it…

In respect to the Q’s specifically, again, it all boils down to whether or not we can reclaim the 20d & firm up above & or make new highs above the 90-Day Delay highs… as of now similar as to Spooz, but Monday’s low is a clear LIS for bulls as it established a higher low thus far. If we were to see tomorrows bull-gap fade, do still ultimately think that the Q’s need to remain supportive above 439 / 434ish & as long as that does remain supportive, we should see the Q’s continue to work back higher towards these recent highs in the mid-460s.

On the contrary, if we were to see tomorrows bull-gap fade & the Q’s start to work back towards 439 / 434ish demand below, it essentially comes down to those lows sticking & remaining supportive, as otherwise, we may get another full retrace back down towards Monday’s low in the upper-420s which essentially is a much bigger LIS for bulls to hang on to, as otherwise, bulls run the risk of completely unwinding the 90-Day Delay rally.

- IWM

Shockingly enough, small-caps have been the best performing index on the week as they currently sit higher by just over 50bps whereas at one point, small-caps were lower by nearly 300bps on the week (yesterdays low). The key factor for all of the indices here given the Trump walk-back boils down to hard data & whether or not the weakness materializes… Trump’s pivot today shows a clear easing up on policy by the administration, but the issue is damage has already been done to the economy & if weakness were to start to filter through, it should be taking place these next couple of months.

In respect to IWM, given todays move along with the after-hours move, small-caps are pushing higher up into the 20d & again, if we were to see small-caps firmly reclaim the 20d, that likely extends the rally further to fill the initial Liberation Day gap in the mid-190s & then above that, likely a backtest of the 199 / 202 prior demand zone above which also just nearly coincides with the 200wk as well & IF this were to be a vicious bear market rally (assuming recent structural change of policy doesn’t stick & or interim uncertainties aren’t resolved), that would likely be the logical spot for small-caps to backtest before then resuming back lower.

On the contrary, if tomorrows gap-up were to fade, I do still think bulls need to see 184 / 180ish supportive on dips, but if that falters, I could see small-caps filling right back lower to unwind the 90-Day Delay rally in full to the mid-170s & the move would likely be driven by weaker hard data starting to materialize & or uncertainties around trade-wars remaining in place with no proper resolve despite the easing up by Trump after-hours.

- DIA

As with all of the indices as we’ve discussed tonight, but tomorrow / remainder of the week boils down to the bull-gap being established & sticking & or the bull-gap failing to sustain thus sending the indices back lower as the recent wide-rangebound action within markets persist.

With the decline in DIA / indices yesterday, as of now, it does look like higher-lows across the board have been established, but if we were to see DIA backtest lower, I do still think DIA needs to hold 389 / 385ish on the downside, as if it were to falter, there isn’t too much support below until the lower-380s / upper-370s (essentially where DIA bottomed Monday) & with Monday’s low now being marked off as a clear Bull LIS given the higher-low that was established, a fail below runs the risk of a full unwind of the 90-Day Delay rally… again, likely would be driven by slowdown fears amplifying & or hard data starting to weaken after holding up incredibly strong all year.

On the flip-side, if we were to continue to see 389 / 385ish supported by bulls / bull-gap tomorrow sticks, it more so confirms the recent higher-low setup / established Monday for now in the interim & if we were to see DIA work back higher & push-through 406ish where it struggled this past week, that likely would give edge for DIA to push higher to fill the Liberation Day gap above in the 411 / 416ish range.

/DXY

Now to talk about the news after-hours…

For starters, I included the headlines of significance / ones that stood out below:

- TRUMP ASKED IF HE’LL PLAY HARDBALL WITH CHINA, SAYS NO

- TRUMP: TARIFF ON CHINA WILL NOT BE AS HIGH AS 145%

- TRUMP: IT'LL COME DOWN SUBSTANTIALLY BUT WON'T BE ZERO

- TRUMP: NO INTENTION OF FIRING POWELL

- BESSENT: GOAL IS NOT TO DECOUPLE U.S. & CHINA ECONOMIES

What’s the main takeaway? I arguably thought Bessent’s comment was more important than Trump’s as he outright states that the goal of the U.S. isn’t to decouple away from China… unless he’s lying which it doesn’t seem like he is, that narrative has been debunked.

In respect to the headlines out of Trump, it is a clear walk-back regardless what people say. Yesterday within markets, we once again had another instance of bonds lower by nearly 200bps along with the dollar down another 100bps as it traded a 97-handle & then today, we get a walk-back from the administration? Not coincidental at all & it clear shows that a Trump put remains within markets & the bond / fx market likely made them feel a bit uneasy yesterday. In respect to the walk-back, as we have reiterated for a couple weeks now but the market doesn’t need an OFFICIAL trade-deal with China… the main interpretation was that the soft response to other countries by the administration would likely start to rollover and translate to China & sure enough, we got that answer today. Yes, we don’t know the exact tariff rate %, but as we’ve been stating, do expect the tariff rate %’s on China to eventually settle in the 25-35% range & for the ROW, likely near 10% with some countries likely being fully exempt. The administration has completely showed their hand & overplayed it & with the Mexico president getting off the phone yesterday, which was supposed to be an easy deal for the admin, failing to make progress, that more so seemed like a wake-up call for the administration that the U.S. was essentially cornered, & sure enough, we got the walk-back today after-hours which also reiterates that we likely have seen peak-escalation.

The other headline besides the walk-back of aggressiveness on China is the statement from Trump that he has no intention of firing Powell… again, another risk that has been removed off the table for now & it was likely due to calm heads prevailing because of Bessent.

So, where are we at now?

- The White House stated there is 18-deals on the table although none have been totally solidified / confirmed.

- It’s been concluded that these deals are going to take longer than the 90-Day tariff delay as some may take months / years to be fully worked out.

- We’re either going to see another delay & or like today, concessions from the U.S. / a general walk-back against everyone to ease up on policy as deals get worked out in the interim.

- The bigger risk given it seems that trade tensions have eased for now as the administration has backed off on their firmness of policy is hard data weakening from here.

- Despite the walk-back from the administration, U.S. credibility has already been damaged.

The two biggest points are the last two… as we’ve noted earlier, but with Trump easing up on policy & or recent firmness, focus is likely going to shift back towards hard data weakening given the damage that has been done to the economy, although given the administrations pivot, I do think the U.S. has avoided a deep-recession & again, Trump / administration has made it pretty clear that a “put” still remains active.

In respect to the dollar, we initially saw a pop higher following the walk-back from the administration but the pop has since nearly sold off entirely… again, it seems like markets have affirmed that there is a clear credibility issue with the U.S. & damage has already been done & can’t be reversed so easily. Nevertheless, I do think there’s a good argument to be made that the recent dollar rut may have found an interim bottom in the 97s / Mondays low, but for any sort of upside, do think we need to see the dollar reclaim 100.5s on the upside to start to pushback higher towards 102 / 102.8s, as otherwise, each & every pop will continue to get sold given the structural change in U.S. credibility these past few months. If we were to see the lows near mid-97s falter, it likely would be quite negative for the indices in general & signal that mid-90s is next up on DXY.

/TNX

Given the walk-back from the administration after-hours as they look to de-escalate with China, bonds have finally caught a bit of a bid & it’s pretty clear that yesterdays action within bonds & fx once again made the administration feel uneasy hence the pivot after-hours today to signal a softening on policy on China. It does still seem like 10s could’ve established an interim high in the 4.5s, but ultimately, I do still think we need to see 10s flush below 4.25 / 4.2ish, as otherwise, the recent stubbornness / weakness may persist in bonds.

The issue with bonds as of now, is once again, credibility is being called into question & we’re already seeing it with the after-hours fade given the pop in the dollar has subsided quite a bit off the highs. Do think these next few days will be telling in regard to action as IF we do see the dollar work right back lower along with bonds, the pivot by the administration will have held no meaning & something else will need to be done further to re-instill confidence back into the U.S.

Still continue to view bonds as a range-trade (3.65 / 3.8 low-end & 4.75 / 5.0 high-end) & we’re more so stuck in the middle-ground as of now, but I could see bonds catching relief in the interim due to the walk-back from the administration but think for a more real sustainable bid, we likely need to see the dollar sustain a bid / hard data weaken from here / inflation worries & or expectations to simmer back down.