From Liberation Day to Multipolarity

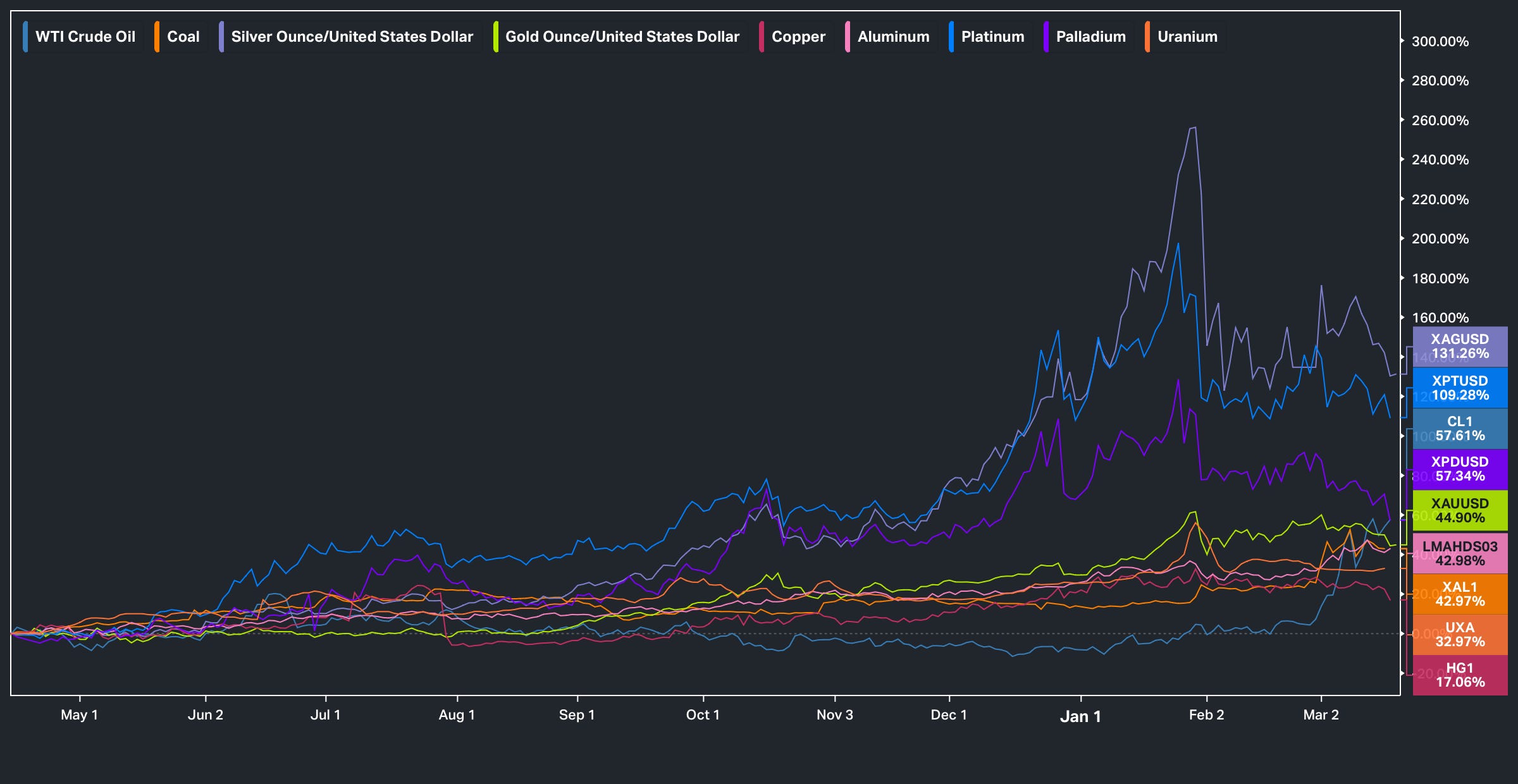

Back in April ‘25, in the aftermath of Liberation Day, we laid out the case for why the world was likely entering the early stages of a new commodity supercycle.

The call was never just about commodities looking statistically cheap relative to equities (as commodities always tend to look cheap relative to equities), nor was it simply a reflexive bullish view on inflation hedges but it was instead rooted in a broader macro judgment: that the global policy regime was drifting back toward persistent stimulus, that fiscal discipline had largely become political theater, and that the physical economy was becoming strategically important again in a way markets had not yet fully priced.

At the time, a set of macroeconomic shifts was already becoming difficult to ignore:

Fiscal discipline across much of the developed world had effectively disappeared

Sovereign debt burdens were rising faster than economic output

Central banks were drifting back toward accommodative policy

Policymakers continued to signal normalization, but behavior suggested dependence on intervention

That matters because environments like this tend to favor real assets. When financial claims expand rapidly through monetary & fiscal policy while the supply of physical resources remains constrained by geology, permitting, labor, and infrastructure, scarcity begins to reassert itself. Energy cannot be printed. Copper cannot be manufactured through policy decree. Strategic materials remain subject to physical limitations regardless of the monetary regime. That tension has been at the core of nearly every commodity supercycle.

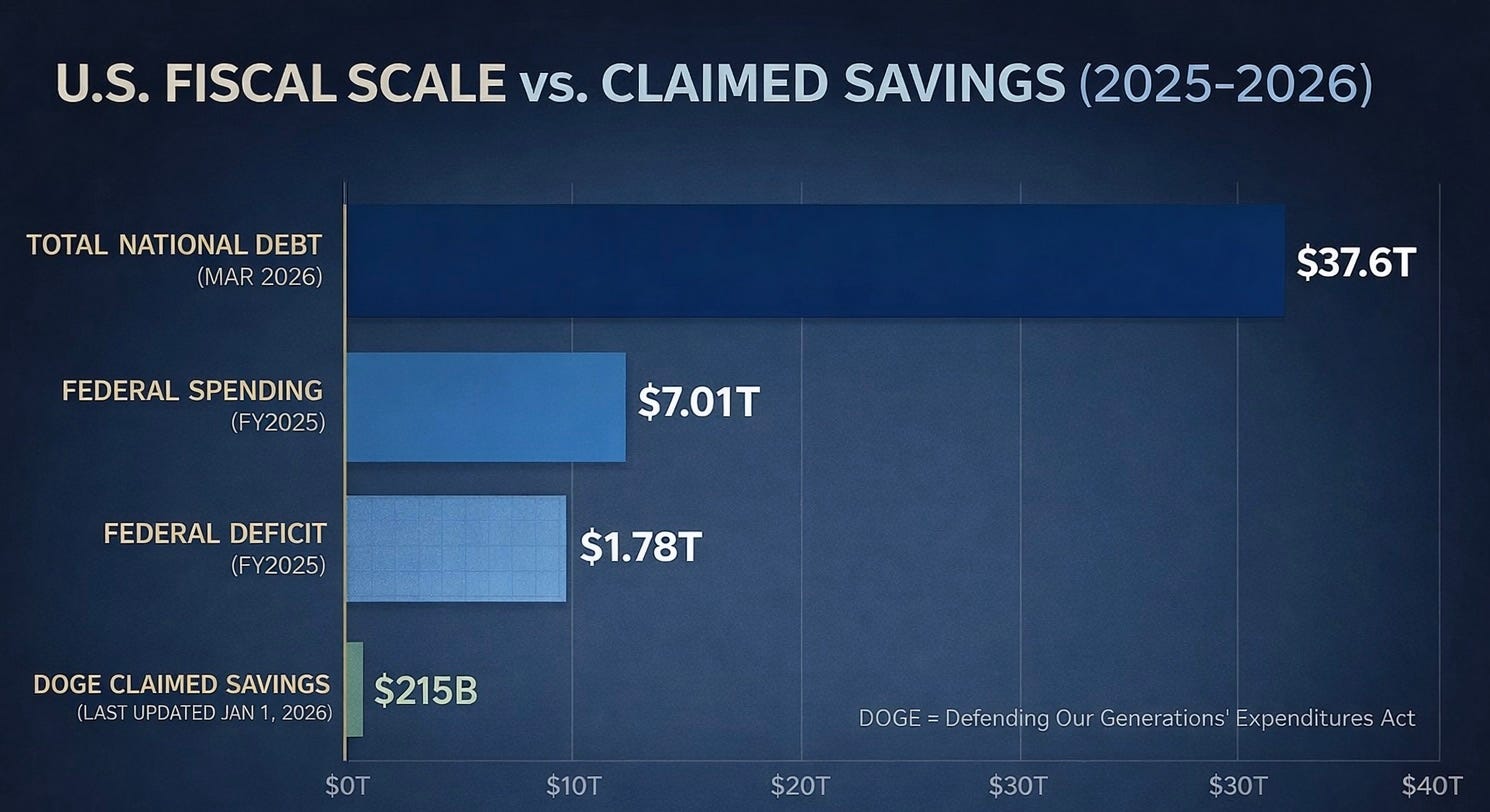

But there was another reason we focused on the theme when we did: the market was still entertaining the idea that a genuine turn toward fiscal restraint might emerge in the United States. In our view, that belief was misplaced. Even back then, it increasingly looked as though DOGE would amount to a nothingburger and that the broader push for spending cuts would prove more cosmetic than real. The rhetoric around restraint was loud, but the structure of incentives pointed the other way. Between industrial policy, defense spending, the structural persistence of mandatory spending programs (such as Social Security, Medicare, and Medicaid), election-cycle considerations, and the growing unwillingness of policymakers to tolerate economic pain, it seemed far more likely that spending would remain elevated than that Washington would suddenly rediscover discipline.

Looking at the actual scale of U.S. fiscal flows makes this dynamic obvious:

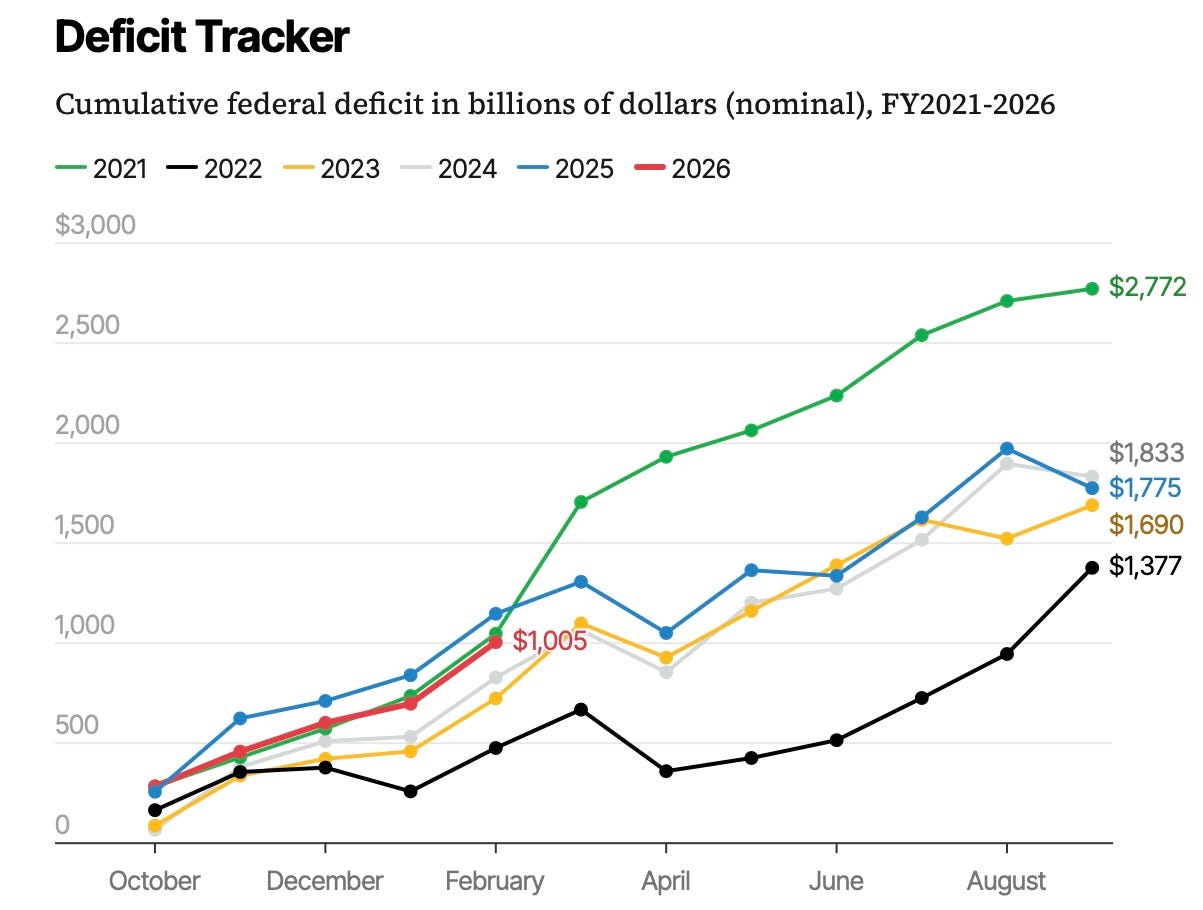

Nearly a year later, the macro conditions that originally supported the thesis remain firmly in place. Global deficits continue to expand, public debt levels are reaching historic highs, and central banks remain cautious about tightening policy aggressively for fear of destabilizing financial markets. In other words, the system still appears dependent on stimulus, even if officials remain reluctant to say so outright.

What was once considered crisis-driven fiscal expansion is now becoming a structural feature of the system.

Even after the post-pandemic peak, deficits have not normalized back toward pre-2020 levels. Instead, they have settled into a persistently elevated range, with annual deficits consistently running well above historical norms despite the absence of a recession or acute crisis. The key point is not simply the level of deficits, but their persistence. These are no longer temporary responses to economic shocks. They are becoming embedded features of the system.

In practical terms, this implies a steady increase in debt issuance, greater sensitivity to interest rates, and a reduced ability for policymakers to sustain restrictive conditions for extended periods of time without destabilizing the broader system. Over time, that dynamic reinforces the same conclusion: financial claims continue to expand while the supply of physical resources remains constrained. As that gap widens, the relative value of scarce, real assets begins to reassert itself.

Put differently, if this is what deficits look like during stable growth, the question is what they look like in a downturn.

And over time, that dynamic feeds back into the same structural pressures…

At the same time, the case for commodities is not only being reinforced from the supply side, but increasingly from demand as well.

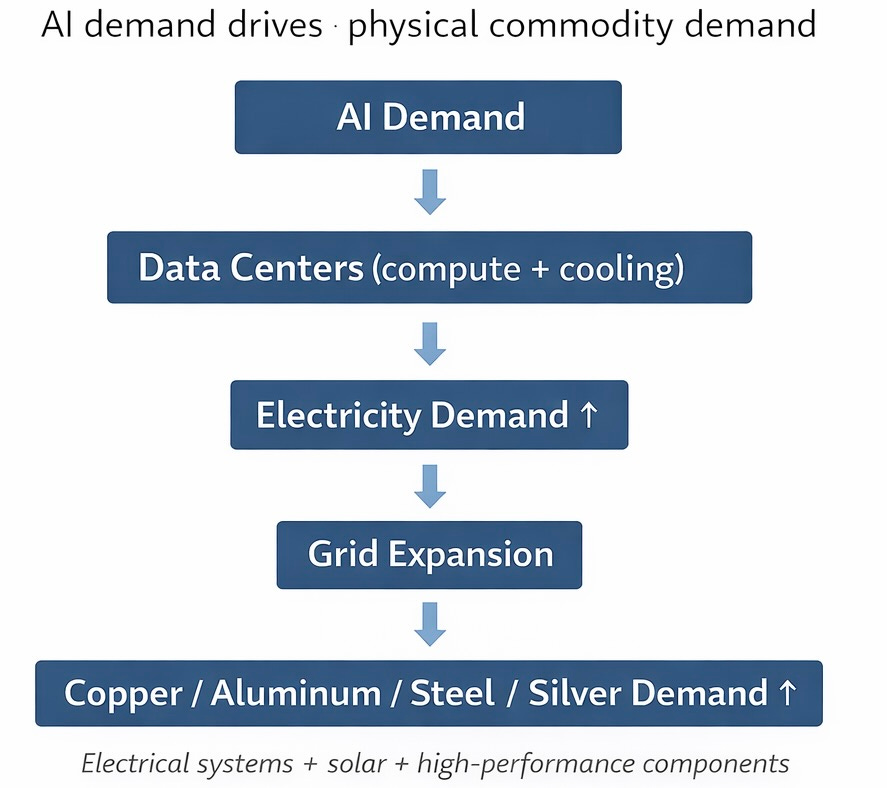

AI is often framed as a digital or software-driven revolution, but in practice it is an extraordinarily commodity-intensive buildout. Hyperscale data centers require enormous quantities of electricity, copper, aluminum, steel, silver, cooling infrastructure, semiconductors, rare gases, and power equipment. The grid upgrades needed to support that buildout are themselves metal-intensive, relying heavily on materials such as copper, aluminum, and silver for high-efficiency electrical systems. Even the supposedly intangible parts of the next cycle are resting on a very tangible foundation of mined, refined, transported, and manufactured inputs. That point is critical because it means the next leg of commodity demand is not dependent solely on a traditional housing boom, an emerging market construction wave, or a one-off policy stimulus cycle. It is also being driven by the buildout of digital infrastructure itself. AI can’t replace the physical economy (unlike the recent fears surrounding software); it amplifies demand for it (scarcity).

Since Trump returned to office, the global economic backdrop hasn’t necessarily “broken,” but it has continued to shift in a direction that’s becoming harder to ignore. The world still runs through the U.S. in many ways, but it’s gradually becoming less singular, less centralized, and more distributed.

That doesn’t mean the dollar is going away or that U.S. leadership is disappearing. The U.S. is still the largest economy, still has the deepest capital markets, and still sits at the core of the global financial system. But what is changing is the behavior around it. More countries are starting to think in terms of optionality, not dependence.

And that shift doesn’t happen all at once. It’s subtle. It shows up in reserve allocation, in trade relationships, in how supply chains are structured, and in where capital is directed. On its own, none of it looks that dramatic. But taken together, it starts to move the system.

That was really the broader point behind the original thesis. It was never just about commodities in isolation, it was about the environment those commodities exist within. A world where fiscal discipline is more talk than reality, where central banks are increasingly constrained, where AI is beginning to translate into real, physical demand, and where geopolitical fragmentation is making control over resources matter more than it has in decades.

That was the setup back in April ‘25.

Nearly a year later, those same forces haven’t faded, if anything, they’ve become more visible, more coordinated, and harder to dismiss as temporary.