Liberated Shock

Hello All,

Liberation Day is officially over & done with & despite the outlined scenarios reiterated by the White House & more so “leaked,” Trump went about his own direction by issuing 10% blanket tariffs on all countries whilst then issuing reciprocal tariffs which is more so where the issues started to stem from as we’ll talk about a bit later.

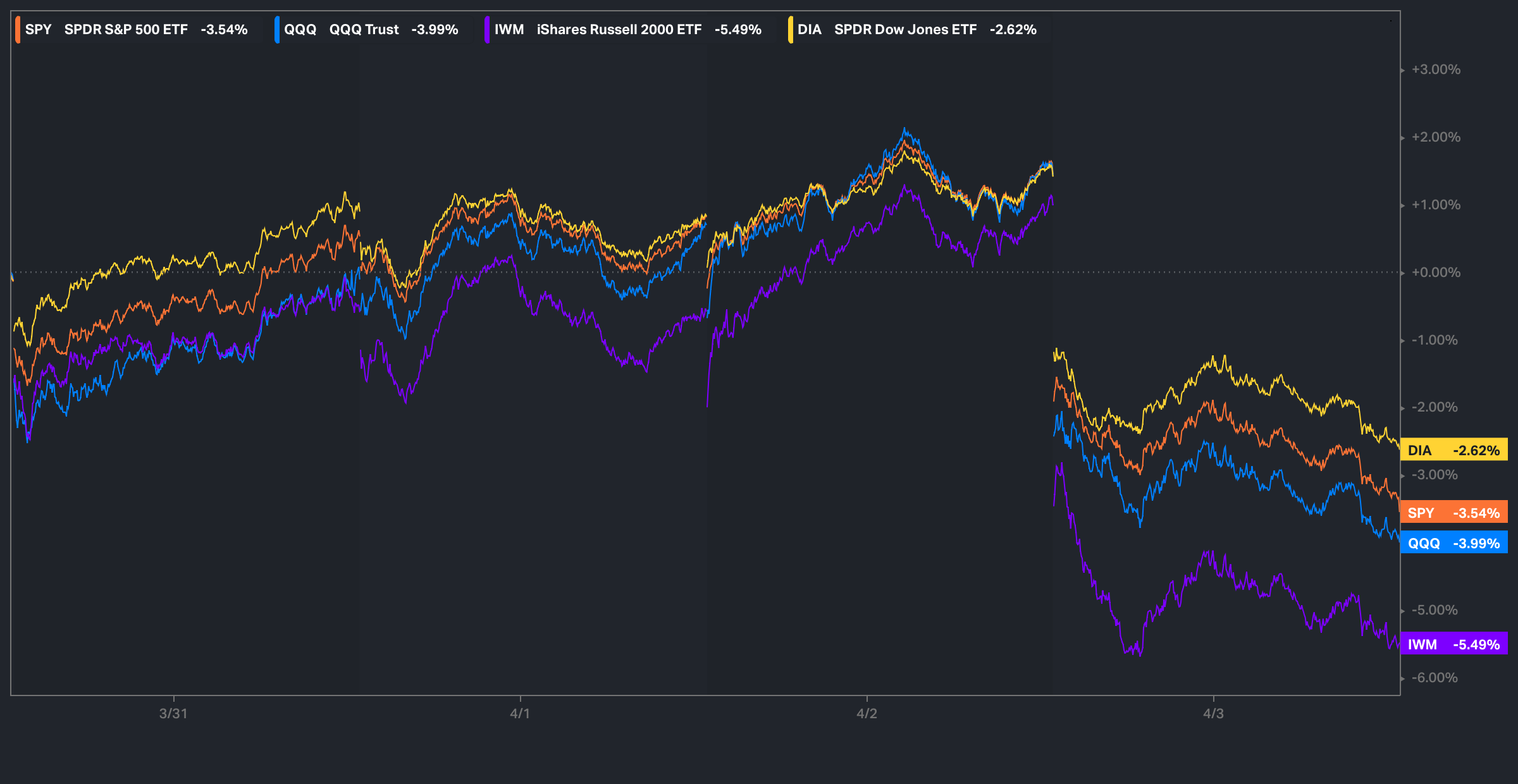

Nevertheless, all of the indices reached new YTD lows & Small-caps thus far have been the worst performing index on the week & nearly reached a limit down today whereas the Dow has been the “best” performing index on the week as it currently sits lower by just over 250bps.

Heading into the remainder of the week, we have NFP #’s before market open along with Powell expected to speak a couple of hours after market open & of course, likely plenty of tariff / potential negotiating headlines flying across the board as well.

Recently, we wrote about the recent developments out of Germany given the infrastructure plan that was announced earlier on in the week & covered the setup in detail along with potential beneficiaries & for those who would like to go & read, the article can be viewed here.

Lastly, recently, we published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

We have finally made it through Liberation Day & sure enough, Trump did do the impossible & caused a complete shock in markets with the decision made to put forth & implement tariffs with how the administration went about… for starters, heading into Liberation day, as of Tuesday night, there was four “leaked” potential outcomes as follows:

1. Universal Tariffs on All Imports

U.S. imposes a blanket tariff on all imported goods (20% was circulated & more so was worst case).

2. Targeted Reciprocal Tariffs

U.S. implements tariffs that mirror the duties other countries impose on American exports. The strategy seeks to promote fair trade by encouraging trading partners to lower their tariffs to avoid U.S. countermeasures.

3. Middle-Ground Tariffs

As of Tuesday’s close, the U.S. Trade Representative’s office prepared a 3rd option—an across-the-board tariff on a subset of nations that likely would not be as high as the 20% universal tariff option.

4. Sector-Specific Tariffs on Key Industries

This approach involves imposing tariffs on specific sectors, such as a 25% tariff on auto imports, to protect domestic industries. Wasn’t necessarily an “absolute” scenario & more so was a subset of scenarios likely to be implemented in addition.

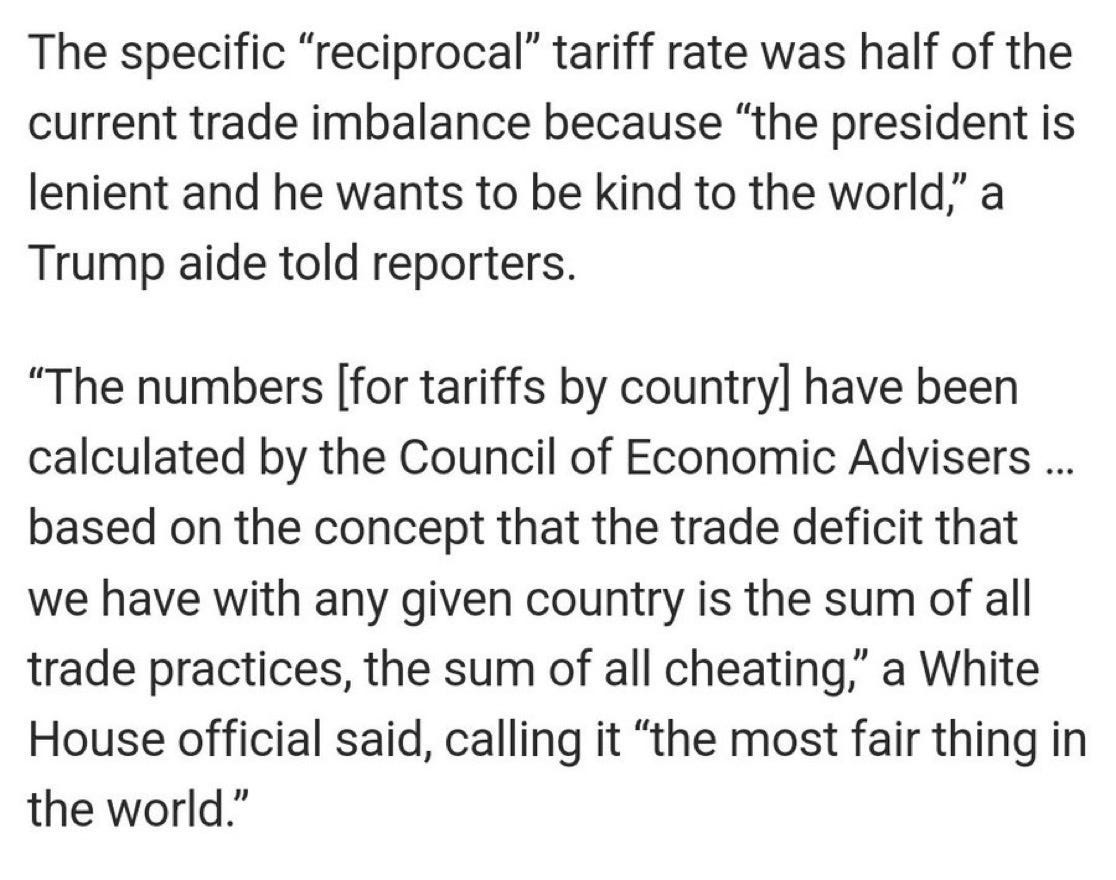

What did Trump end up choosing? He initially kicked off the speech with announcing the implementation of 10% blanket tariffs across the board for everyone… this was initially seen as a HUGE positive, as for the worst case, markets were expecting 20% blanket tariffs but then… Trump announced reciprocal tariffs which were *supposed to be kind & lenient & in the administrations eyes, they were “kind”& “lenient” but that’s due to the flawed methodology with how they went about calculating the reciprocal tariff %.

What was the issue? Well, the tariffs aren’t actually reciprocal for starters… The U.S. is essentially calculating reciprocal tariffs based on the trade deficit as a percentage of U.S. imports from each country whereas reciprocal tariffs should match the actual tariff a country imposes on U.S. goods, not a calculated penalty based on a trade gap… not what a “reciprocal” tariff is at all… (included White House interpretation below).

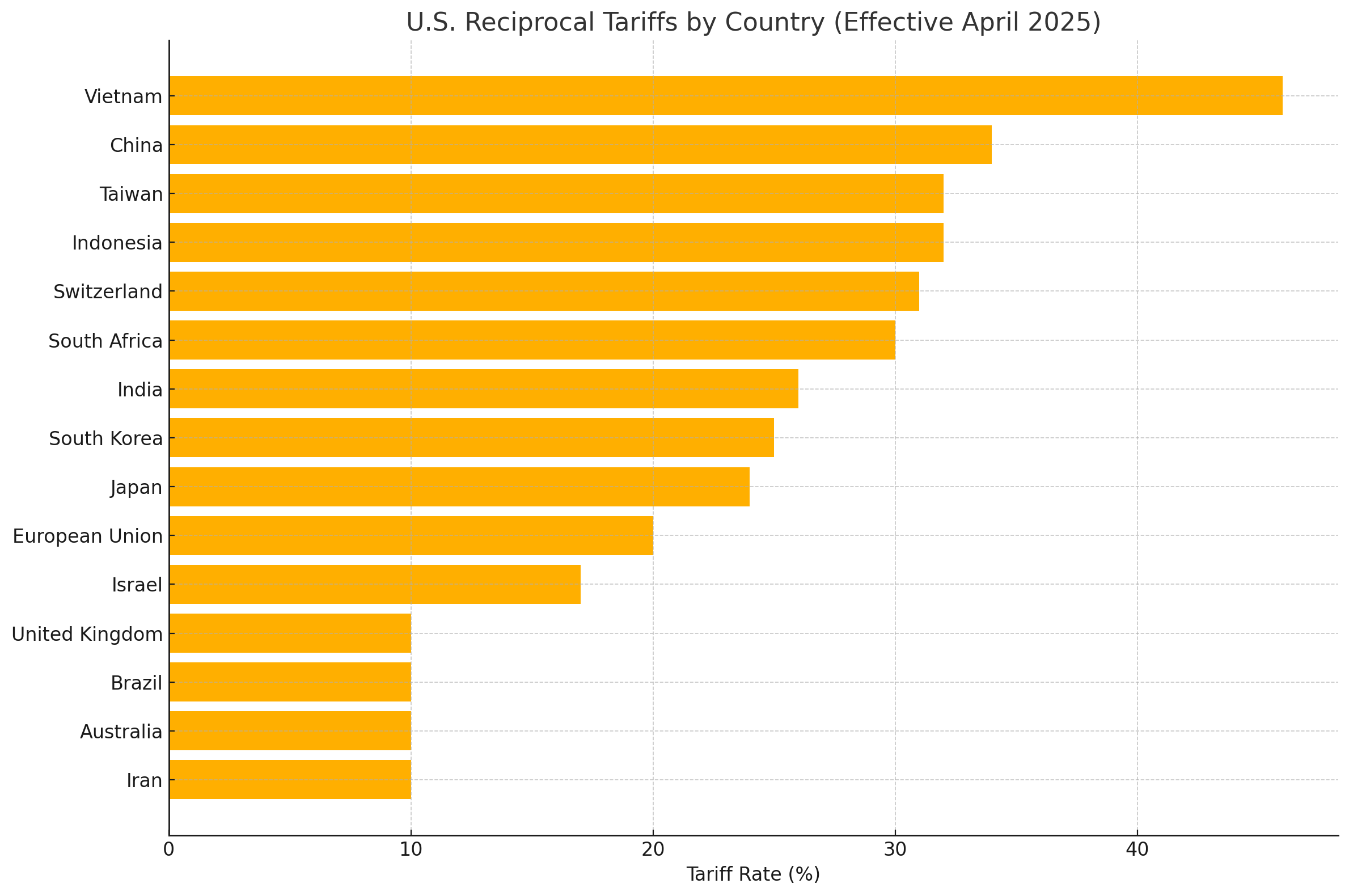

And because of that, it created obscene tariff %’s on a number of countries & I included the bigger countries with respective tariff %’s below:

Why is this methodology so wrong? Well, to use Israel as an example, the other week, Israel took down tariffs to 0% on U.S. imports, but due to the calculation by the White House on reciprocal tariffs, Israel got hit with a 17% reciprocal tariff despite having no tariffs on the U.S. at all… Vietnam is another example as they got hit with a 46% tariff despite working out a deal with the U.S. a couple weeks back to completely avoid tariffs, but again, due to the calculation, the White House “thinks” Vietnam has 90%+ tariffs on the U.S. hence they essentially took that # & cut in half & called that “kind” & “lenient”… in all honesty, quite incredible how the White House doesn’t have an economist to understand how wrong the methodology is.

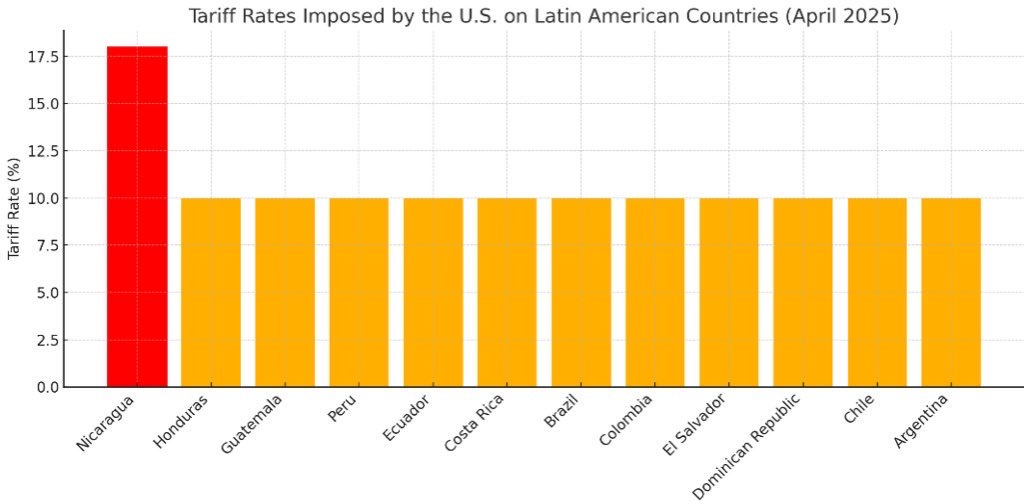

Are there any positives out of all of this? If any at all? Well, Canada and Mexico were left unchanged & weren’t charged an additional reciprocal tariff… I would argue Mexico benefits the most from all of this & this was probably one of the best outcomes that could’ve been made for really both Canada & Mexico as the White House then stated that IF the fentanyl issues make progress, the current 25% tariffs will be cut in half to 12.5%… would not surprise me if Mexico is first for that as well given how their president has handled the current situation.

Who else benefits from all of this? Well… Latin America. Besides Nicaragua, Trump hit the entirety of Latin America across the board with a 10% tariff… considering what other countries received, it’s quite a big positive as they essentially were given the baseline, & Argentina is already looking to be the first of Latin America with tariffs completely removed.

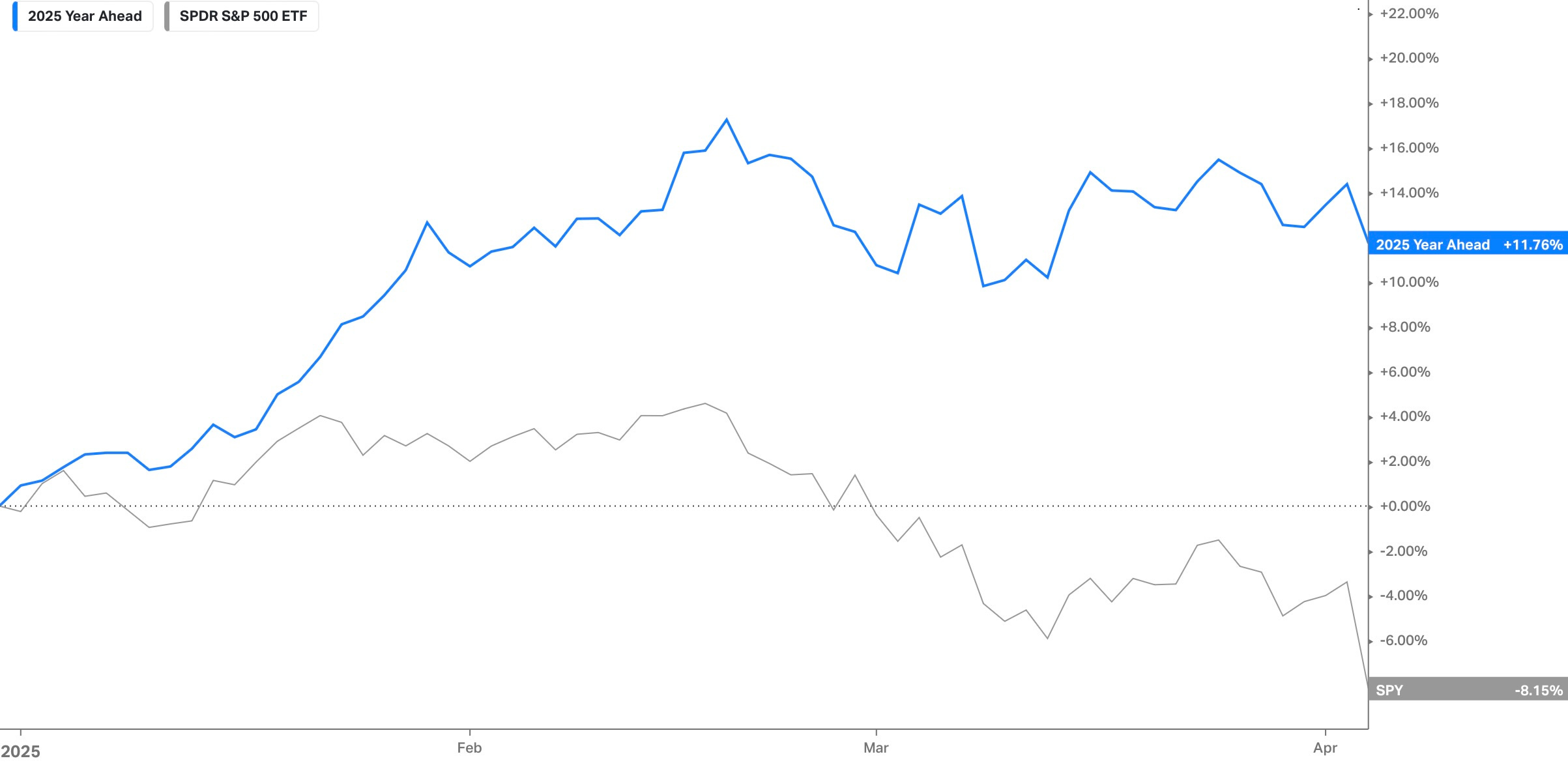

South America was a fat-pitch for us coming into ‘25 & was a major topic covered within the Year Ahead ‘25 which we released back in November ‘24 & for those who want to go back & read the extensive piece, it can be found here.

Nearly a 20% spread between the Year Ahead ‘25 basket & Spooz YTD.

And even the 1-Yr spread has been quite impressive & this year especially, the names have been a nice buffer / diversification hedge for performance.

Moving along… so what else was negative? Well, again, this was a total shock to the markets & was not one of the three scenarios that was highlighted by the White House & in even looking at Bessent, it seemed like he was totally caught off guard by all of this. The “good” news is that the baseline tariffs will be implemented on the 5th which isn’t TOO big of a deal & we may even see some deals worked out prior, but more importantly, the 9th is when reciprocal tariffs are supposedly going to go into effect. Why did Trump give a week & not implement them on Liberation Day? Surely it wasn’t to leave room to negotiate right? One would assume that it likely was the reason & within the coming days, would expect there to be a plethora of headlines of countries negotiating to try and strike deals & or countries dropping tariff %’s in full in hopes the U.S. does the same. The one other added point is Trump is starting quite high in terms of tariff %’s & he likely knows that, so it really gives the White House plenty of room to work with if they were to negotiate whilst also motivating countries to try and talk up the White House, as otherwise, it likely will be quite detrimental for several countries & especially the U.S. specifically.

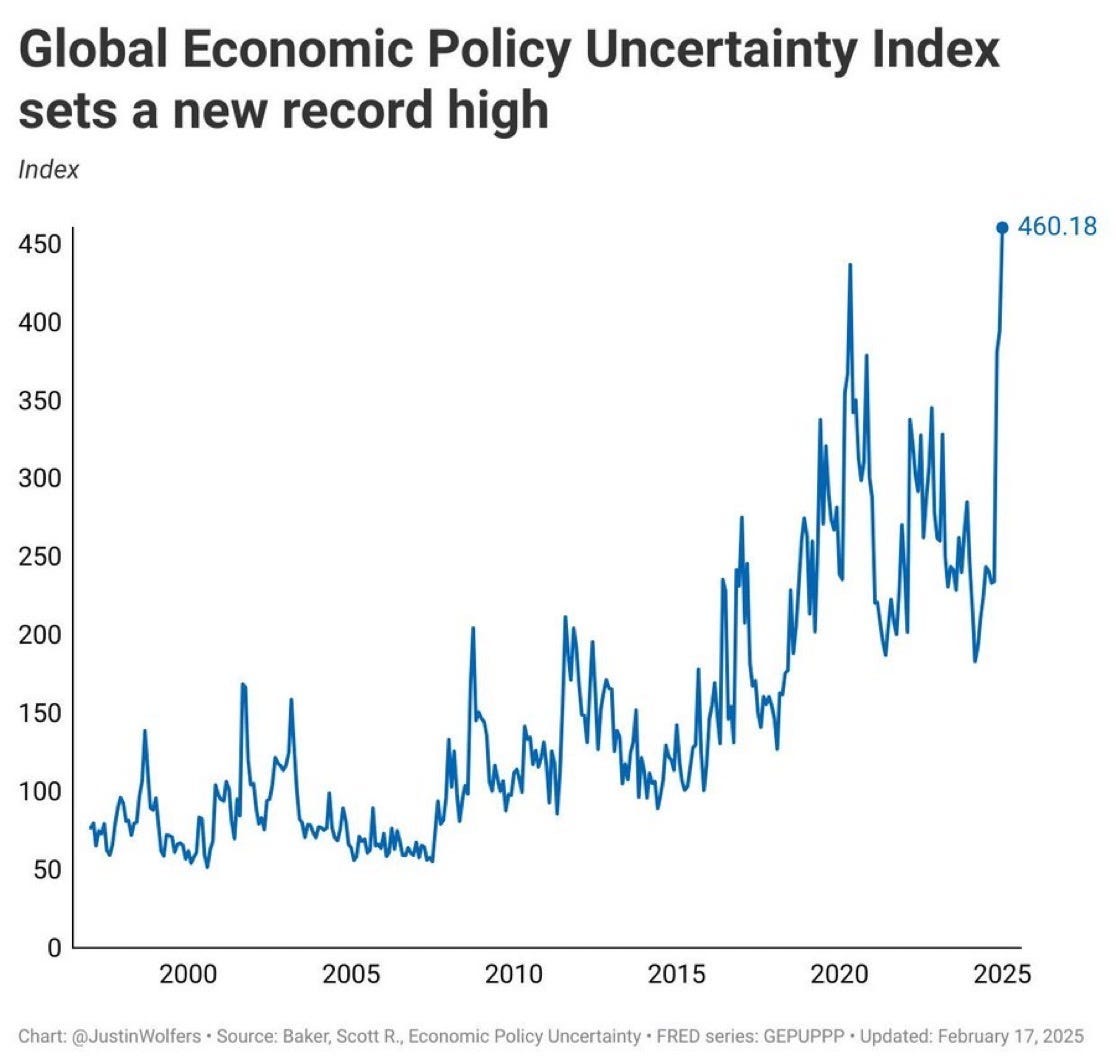

Having said all of that, the administration did achieve a new record as uncertainty surrounding policy has surpassed the Covid Crash levels… sentiment is quite pessimistic & rightfully so given the general shock that the administration has caused to the markets.

What about the indices?

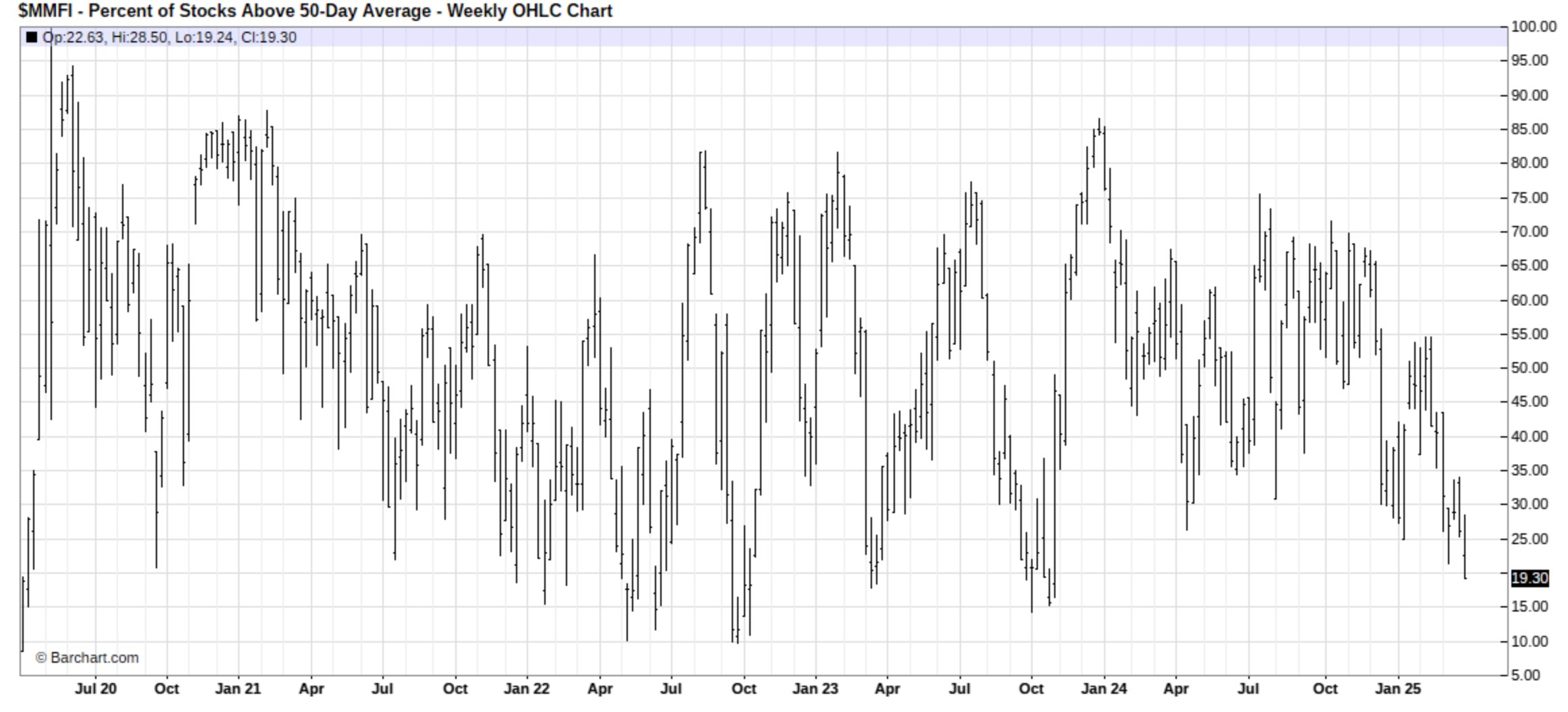

As of now, 81% of stocks are sitting below the 50d… essentially approaching the late ‘23 bottom levels & just below being the ‘22 bear market bottom levels.

In respect to the 200d, only 28% of stocks still reside above the 200d & majority are all likely defensive / recessionary stocks & we are just shy of late ‘23 bottom levels (25%) whereas the ‘22 bear market bottom levels are still a ways away at 15% below.

Nevertheless, point being, things are very extended to the downside at these levels & we’re likely approaching a trade-able bottom sooner than later.