Overdone or Warranted?

Are recent growth fears overdone or are they warranted?

Hello All,

It’s been quite the week in markets thus far as the headline driven volatility remains… we had quite a good day in the indices yesterday, but then today, we saw all of the gains completely unwound in part driven by the volatility / flight-to-safety bid in the Yen (carry-trade unwind), which more so put pressure on U.S. equities.

Thus far, small-caps have been the worst performing index on the week mostly driven by recent growth fears & uncertainties whereas the Dow has been the “best” performing index on the week although still sits lower by just over 250bps & a bigger driver of the recent outperformance has more so been attributed due to some of the components within the Dow being categorized as defensive / flight to lower beta trades.

Heading into tomorrow given we have NFP #’s, the big question at this moment is whether or not recent growth fears are justified & or if they are overdone & if this recent hysteria is indeed a growth scare & not a recession & or vice-versa.

Last night, we wrote about the recent developments out of Germany given the infrastructure plan that was announced earlier on in the week & covered the setup in detail along with potential beneficiaries & for those who would like to go & read, the article can be viewed here.

Lastly, recently, we published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

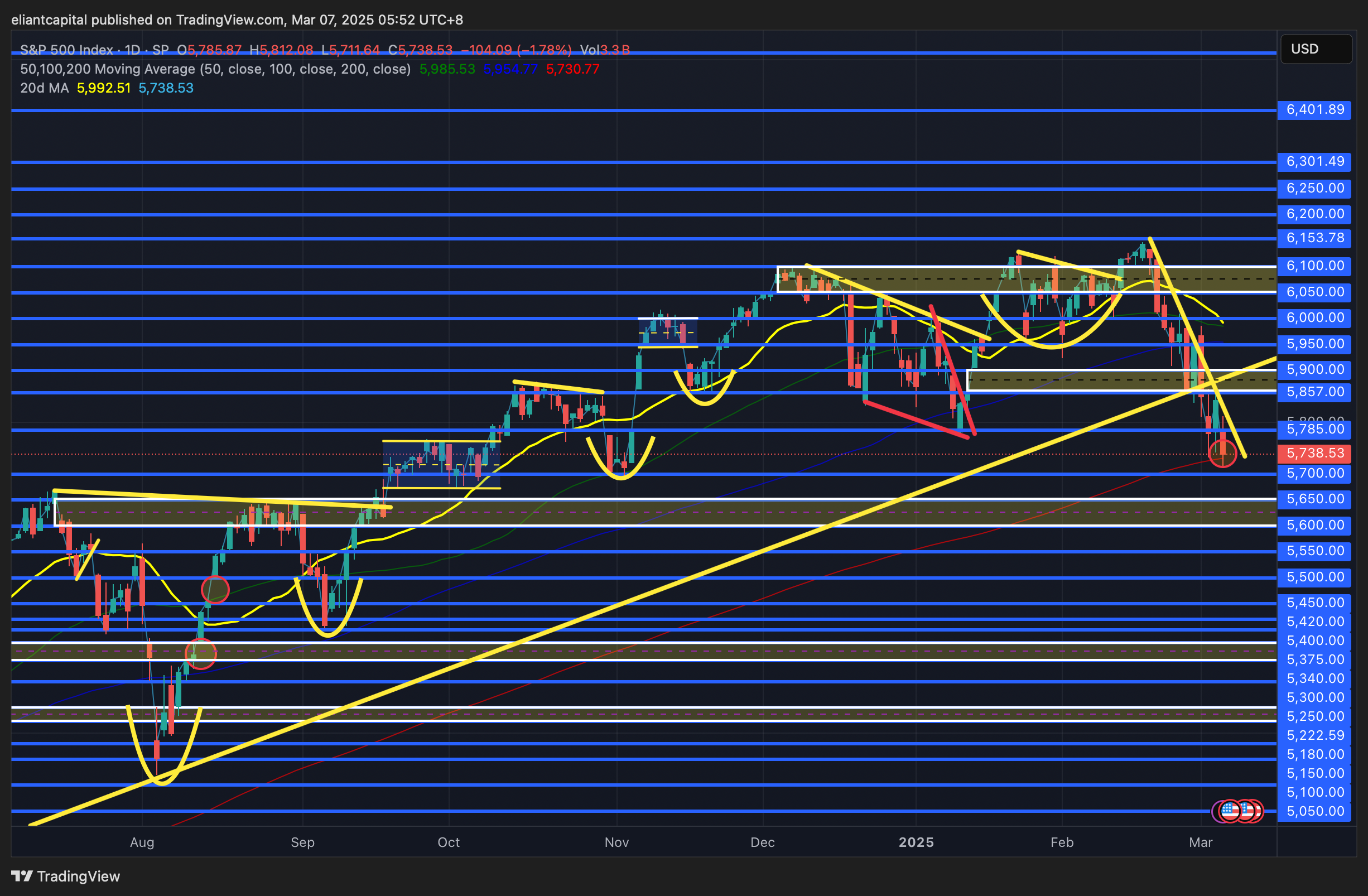

- SPY

The volatility within markets remains as the headline driven madness has continued… the indices actually finished off quite strong yesterday, but following into today, the indices were met with a large gap down on no specific news, but the main contributor was likely due to the sharp rise in the Japanese 10Y which more so caused a bit of flight to safety action within the Yen leading to this general unwind within U.S. equities today.

In regard to headlines… we had plenty of them today, but I included a few standouts below:

- White House Official: US pauses until April 2nd tariffs on Canada and Mexico USMCA trade (Anyone recall back in February when Trump delayed tariffs until March… well, now the can has been kicked another month down the road).

- White House Official: One-month exemptions to 25% tariffs on Mexico and Canada are going to cover all USMCA-covered goods.

- White House: The US could drop tariffs on Canada and Mexico with fentanyl progress (I thought this headline was one of the more important headlines as it seems like a general win-win situation for everyone around… of course assuming the U.S. would actually honor this & drop tariffs if the fentanyl issues did make good progress).

Having said that, we’ve reached another instance where the Trump administration has caved in on tariffs (for now) & to our expectations, Trump continues to be much more lenient on Mexico over Canada & do expect that to continue regardless… the main issue in the interim is the recent drama surrounding tariffs which has provided this widespread uncertainty amongst companies across the board as its hard to necessarily react when a different headline comes in every other day contradicting one over the other which inherently has contributed to recent growth fears.

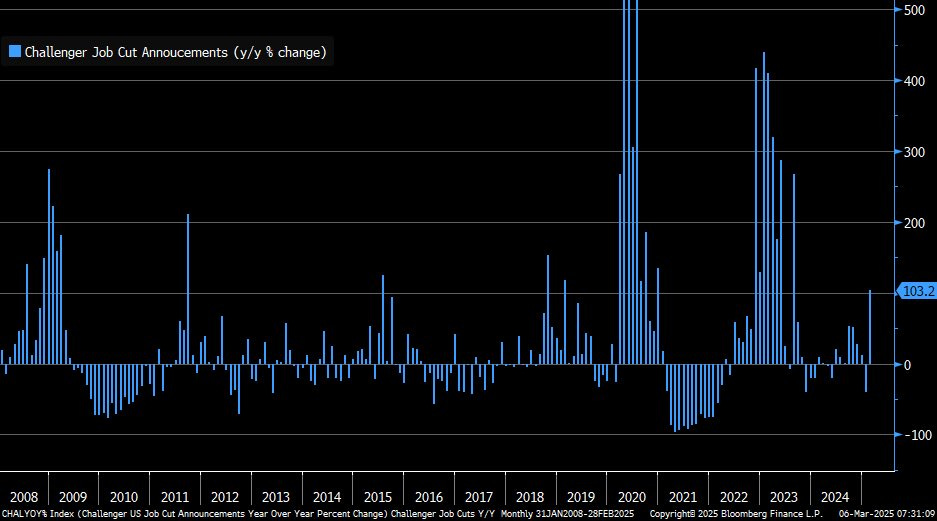

In adding on to recent growth fears, February Challenger job cuts surged to the highest level since ‘20 & was the largest spike since August ‘23… granted, jobless claims came in better than expected at 221k vs. 242k prior, but Challenger job cuts more so got all of the headlines as it tends to be a leading indicator & a big driver of the surge was due to DOGE cutting govt. / federal jobs.

Whilst on that subject, tomorrow, we have NFP #’s & it’s a fairly important report given recent growth worries… as of now, Jobs are expected to come in at 170k vs. 143k prior & the unemployment rate is expected to remain unchanged at 4%. There is quite a bit of pessimism into tomorrow as consensus seems to think the setup is there for a potential large miss given recent govt. / federal layoffs & general uncertainties revolving around the job market right now.

Personally not expecting any surprises specifically tomorrow & if anything, govt. / federal job cuts likely wouldn’t start showing up in data until the following month / later on in Spring, & IF the jobs report is good tomorrow (I’d argue as long as solidly above 100k / No spike in UER & generally contained at 4.1% or below), it should help ease recent growth worries which then makes the setup interesting into next week given we have inflation data… IF we get a good jobs report tomorrow & then good inflation data next week… there’s a word for that…

In respect to Spooz, even though Spooz did lose the support TL dating back to late ‘23, it has now tested the 200d / came near it several times these last few days but has failed each time to sustain a breakdown below… bulls are clearly trying to make a line of defense here. I don’t have too much to comment on as tomorrow is fairly data-dependent, but if jobs do manage to not “surprise” the markets given VIX is 25+ & expectations are VERY high into tomorrow… we could see a bigger vol crush as hedges unwind whereas on the contrary, if we were to get softer data, I could see Spooz initially gapping down which then leads to a R/G reversal later on in the day… likely after Powell speaks (Softer Jobs data → Dovish Leaning Powell).

For any sort of material upside, as of now, Spooz does still remain in this steep downtrend, but if we were to get a snapback rally off the 200d, do think we see Spooz rally back towards 5850 / 5900ish before initially pausing & deciding where to go next from there… on the contrary, again, if downside were to see further continuation, I could see Spooz producing a look-below-and-fail move of the 200d as it snaps lower to backtest the ‘24 highs near 5650ish (also coincides with 50wk), before putting in a potential bigger bottom then leading to a potential snapback rally. Again, with VIX at 25+ heading into tomorrow, downside expectations are VERY high, so as long as tomorrow's job report isn’t an outlier print, we should see Spooz / general indices catch a bit of relief.

- QQQ

Quite an ugly day for the Q’s as it closed out the day lower by just over 250bps & as we spoke about earlier, but the main contributing factor was likely due to the general flight-to-safety action within the Yen as we saw tech momentum names unwind although some single names held up fairly well & more so shows that they likely reached seller exhaustion… (MSFT & GOOGL were two clear standouts).

In looking at the Nasdaq below, it still remains within the upward parallel channel it has remained in since late ‘22, so all in all, no “big” technical damage has been done on the bigger picture & thus far, this more has just been a quick & violent pullback to the bottom of the channel as of now.

In respect to the Q’s, as of now, the Q’s closed just below the 200d whilst closing right on the support TL dating back to late ‘22 (Also sitting near pre-election levels so fairly big area of confluence)… still fairly simple from here, but pending tomorrows data, if we were to see the Q’s open with a gap-up tomorrow & it sticks following the jobs data, that likely signals the interim bottom has been established with an island bottom gap-up & that should generally lead the Q’s to revert higher towards the 501 / 508ish range above, but ultimately, until 508ish on the upside is firmly reclaimed, the Q’s still may be in for some more volatility / rallies may continue to get sold in the interim

On the contrary, if we were to see this support TL below cave in as support & the Q’s fail to quickly reclaim it, we could see the Q’s work lower on & potentially fill that gap from mid-September near mid-470s.

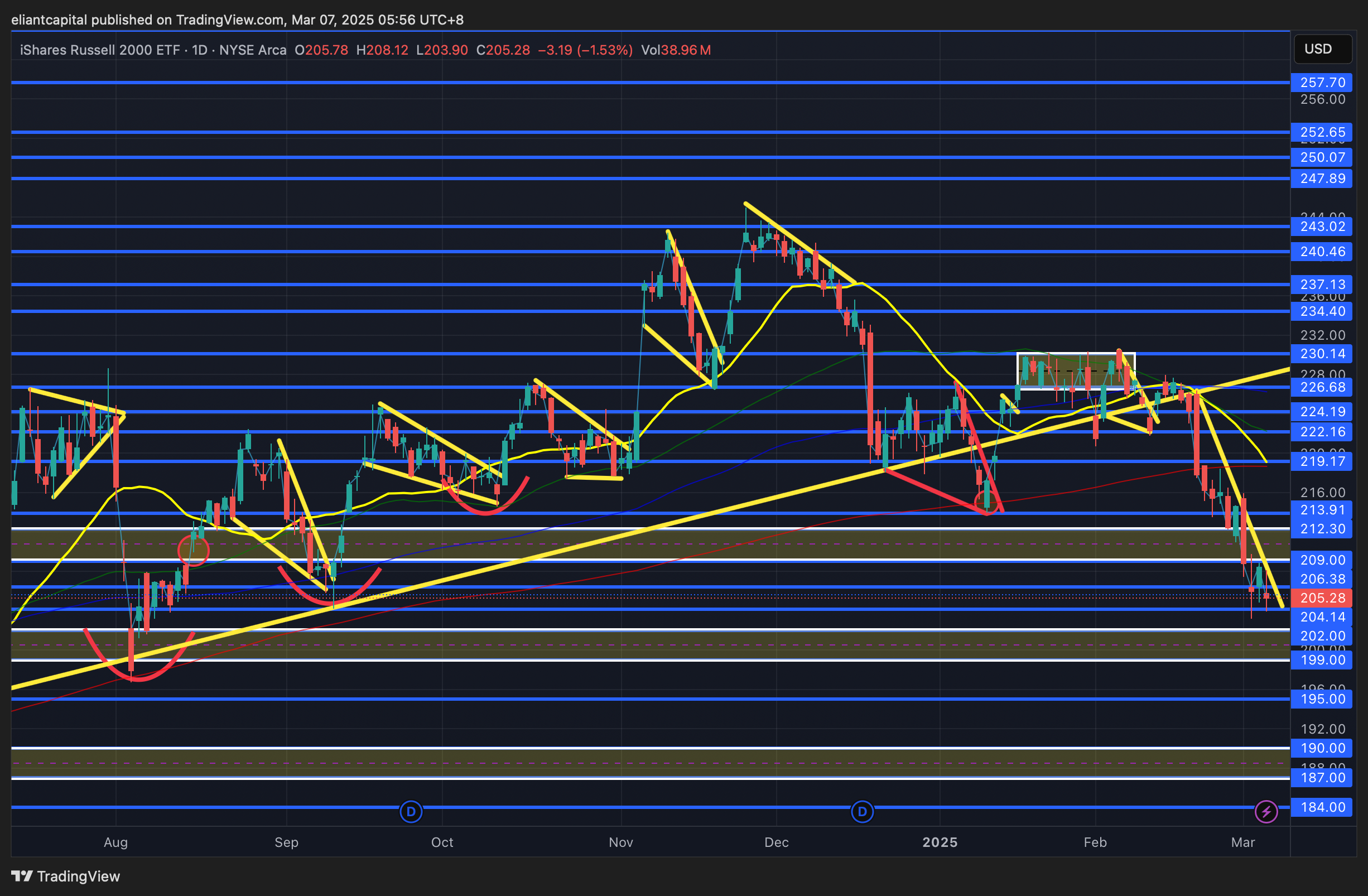

- IWM

As we discussed earlier, but we have NFP #’s tomorrow & it’s a fairly important datapoint given recent growth worries & hysteria revolving around the report. As of now, jobs are expected to come in at 170k vs. 143k prior & the unemployment rate is expected to remain unchanged at 4.0%. If jobs / UER were to come in-line & or generally near this same range, it would be a GREAT report for small-caps & markets in general as it would help ease recent growth fears… as discussed earlier, but I do think as long as jobs remains above 100k & or the unemployment rate remains below 4.1%, growth fears in general should remain contained given pessimism is quite extreme heading into tomorrow.

In respect to IWM, as of now, small-caps are right up against the downtrend which initially kicked back off in February with the 200wk sitting just below… it is a ripe setup for a snapback if jobs were to be ok tomorrow / better than feared, but ultimately, we do still need to see IWM reclaim 213 / 214ish to start to work higher towards 219ish, as otherwise, interim rallies may continue to be faded.

On the contrary, if we were to see these recent local lows falter, we likely will see small-caps get the test of the 200wk just below near 200ish which should be a fairly big & reactive support & do not necessarily expect that support to give in easy & at the very least, it should produce some sort of violent snapback rally.

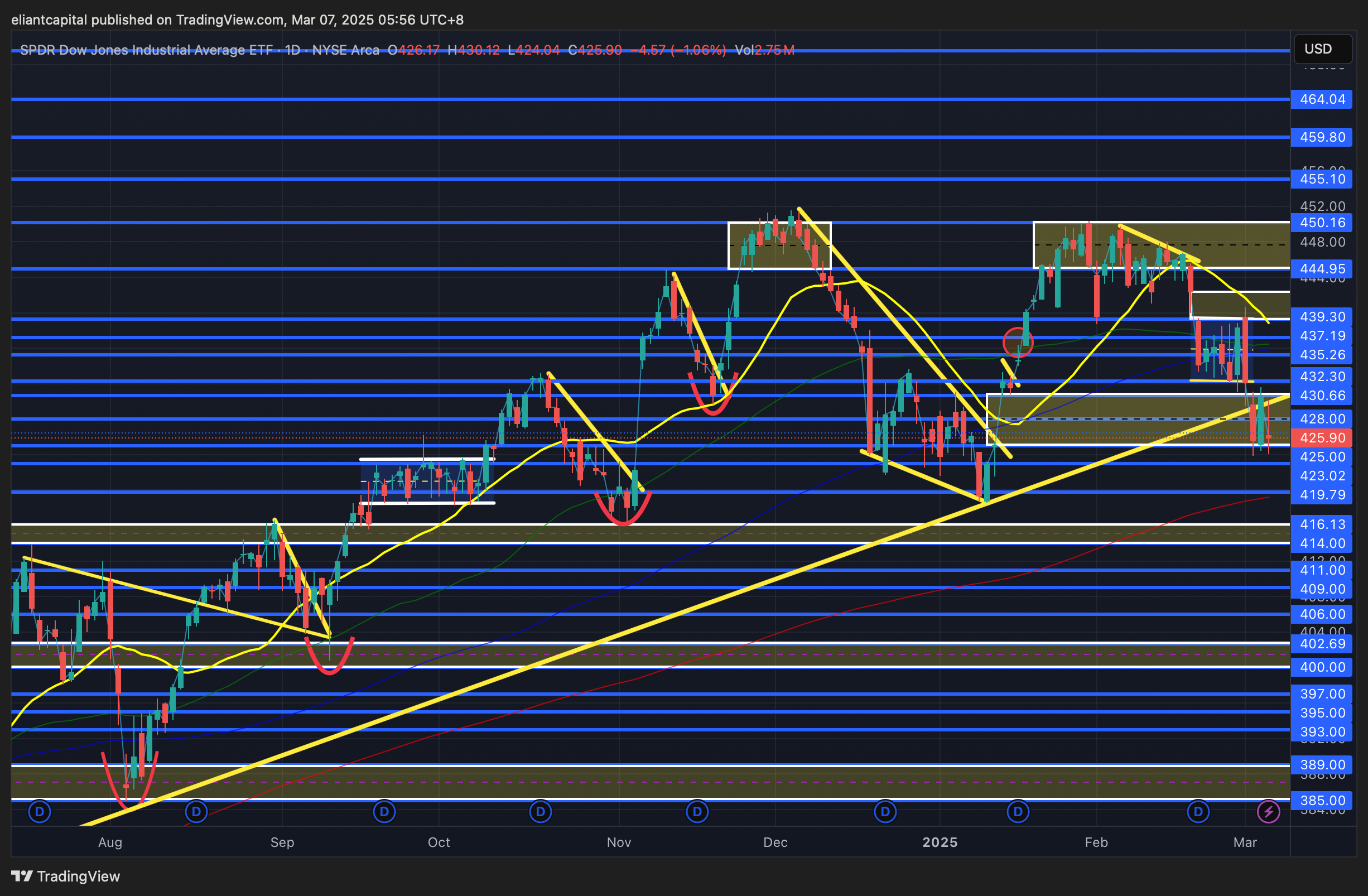

- DIA

The Dow has been the “best” performing index on the week, but still sits down just over 260bps on the week & a part of the larger outperformance against the other indices has more so been due to some of the defensive components within the Dow.

In respect to DIA, on Tuesday, we finally saw DIA fill the CPI bull-gap from early January & since, the gap-fill has continued to remain as support… as long as these lows do continue to hold, DIA will likely look to retrace towards 432ish, but ultimately, still do need to see 439ish taken out on the upside to get some further upside momentum going, as otherwise, the market will still likely remain in “all rallies being sold” mode (of course barring a headline).

On the contrary, if we were to see these recent local lows falter as support, the 200d is sitting just below on DIA & more so will likely act as a magnet that leads DIA to test the 200d which also happens to coincide with the January lows, so in general, it should be a more firm support if it were to be tested & potentially lead to a more sustainable interim bottom.

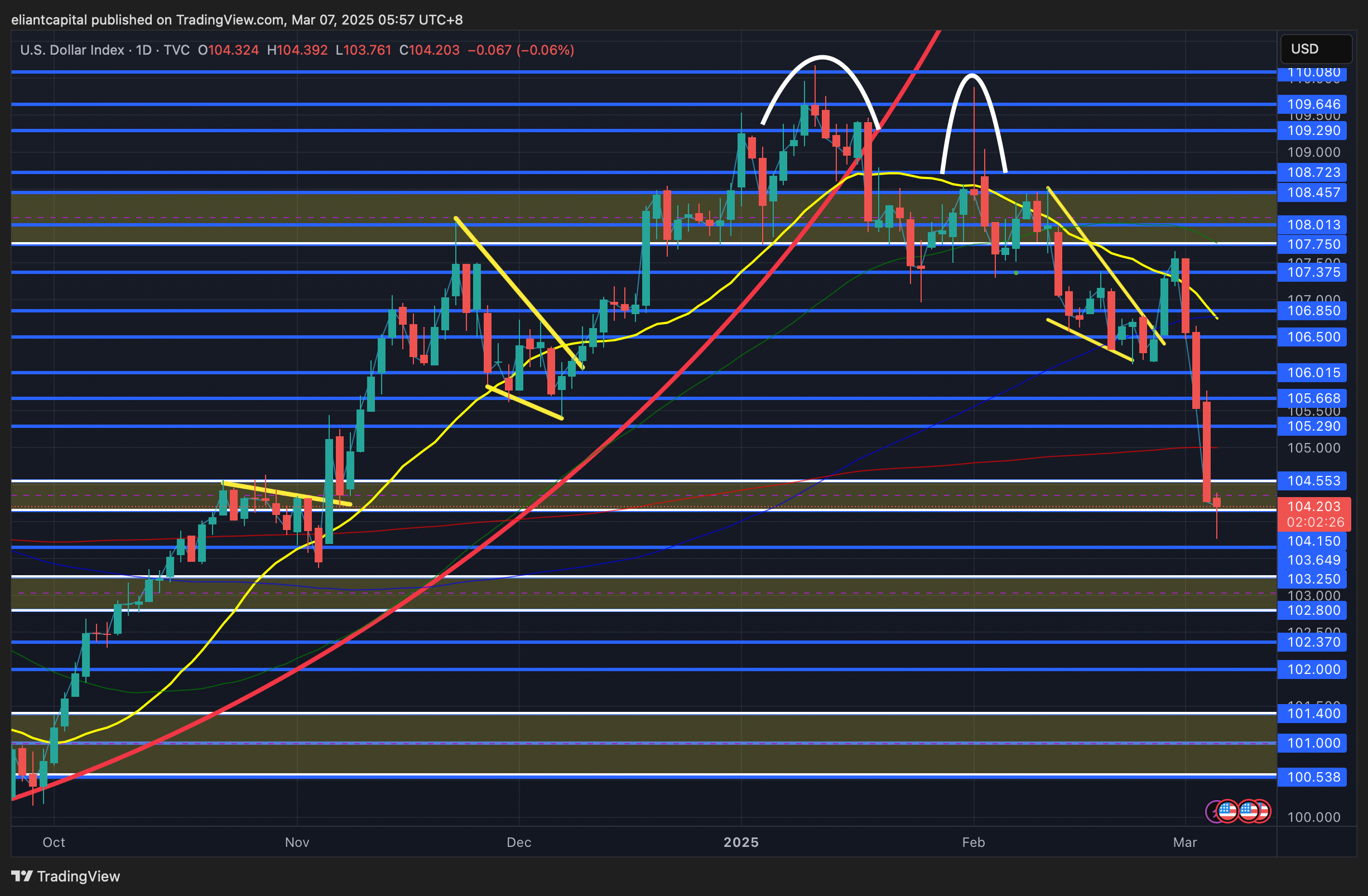

/DXY

It has been quite an interesting week in FX land… we have continued to maintain a bearish stance on the dollar & a positive stance on EMs / ROW & it’s been one of the best trades year-to-date as capital continues to flow out of U.S. equities & rotate to other parts of the world.

In respect to headlines today excluding the tariff ones we covered earlier, there was one other standout headline today as shown below:

Trump Special Envoy Witkoff: We are trying to get a framework for peace agreement and initial ceasefire for Ukraine.

Recently, a big contributing factor to the dollar weakness has been due to the outperformance out of the Euro… in part driven by Russia / Ukraine peace hopes (which look to be advancing as shown above) & more recently, the fiscal impulse / plan out of Germany which more so looks like an entire narrative shift. Last night, we published a piece on Germany & the infrastructure plan, so I am not going to get to into detail here, but do recommend going to read as we started buying the basket of names today at a 5% weight. Link to the write-up can be found here.

Again, not much has changed as the dollar has continued to remain under pressure due to recent optimism on the Euro (after it was going to parity in January) & then in regard to tariffs, they have turned out to be bluff which has led both CAD & MXN to maintain a bid against the dollar & more so also driving down credibility of the U.S. which has also likely been an added contributor of recent weakness. The dollar is VERY extended down here, but besides a technical bounce / work off oversold conditions, still don’t necessarily see a clear catalyst to shift this momentum anytime soon as the path of least resistance continues to be lower on the dollar.

Tomorrow, we do have NFP #’s & if the report were to be better than expected, that may bring about a bid in the dollar & we could potentially see a retrace towards 105 / 105.29 (backtest the 200d), but otherwise, unless the dollar starts to firm up above mid-105s, we likely will continue to see the dollar gradually drift lower towards 103.25 / 102.8s below (potentially on softer inflation data next week).

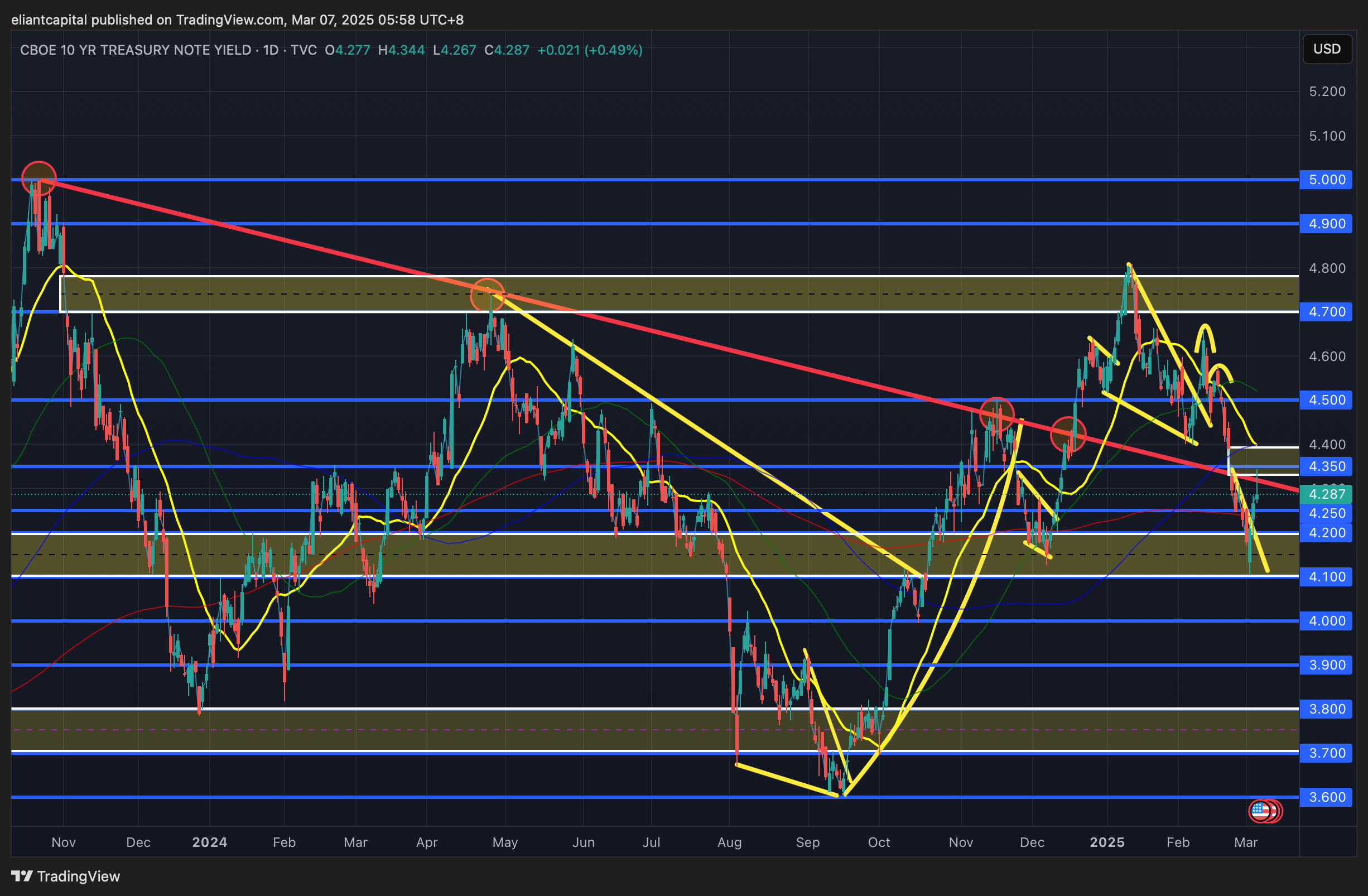

/TNX

On Tuesday, we decided to exit our long bonds position (right near HOD) which turned out to be a fairly good call as the 10Y ended up bottoming out at 4.1ish & as we suggested, we did indeed see a snapback in the 10Y right back up towards 4.35ish.

This week has been an interesting one as Spooz has been down over 100 handles these past few days consecutively, but bonds still can’t manage to find a bid as the recent panic bid has nearly completely deflated… I do think the recent action in bunds is in part playing a role given the big spike due to the fiscal plans out of Germany (VaR-Shock).

In respect to tomorrow, before close, did reiterate that the best hedge for tomorrow in case there were to be an outlier job report / miss was Bond / TLT calls. As of now, we did see the 10Y reject 4.35ish & if we were to get a softer jobs report tomorrow, I think we could see the 10Y right back near 4.1ish… potentially even near 4.0ish if it were a BIG miss (seems unlikely as of now), whereas on the contrary, a “good” jobs report (100k+ jobs added / UER contained below 4.1ish), should continue to unwind the recent flight to safety bid in bonds, although I don’t necessarily expect a rapid rise in the 10Y if growth fears were to ease, as for next weeks inflation data, it should be a generally softer report from the prior month / disinflation should start resuming which should be a general tailwind for bonds (4.0 / 4.5 interim range on the 10Y).