The Week Ahead 3/15/26

Hello All,

I hope you’re all enjoying the weekend and getting some time away from the screens & wishing you all a successful remainder of ‘26.

This past week was yet another eventful one geopolitically as tensions between the U.S. and Iran continued to escalate. Over the weekend in particular, markets experienced a brief wave of panic as oil prices surged nearly 30%, while equities fell roughly 3-4% across the board in the overnight session heading into Monday. However, rumors of a coordinated global SPR release, along with comments from Trump suggesting the war could be nearing an end, helped spark a sharp rebound in risk assets earlier in the week. That said, the rally faded through the latter half of the week following Iran’s threats to place sea mines in the Strait of Hormuz and continued escalations from both the U.S. & Iran. With traffic through Hormuz still disrupted, markets gradually drifted lower, leading to a slow bleed across the indices into the end of the week.

That being said, the Q’s ended up being the ‘best’ performing of the indices on the week, although still closed lower by just over 100bps, whereas the Dow was the worst performing of the indices on the week, having closed lower by just over 180bps.

- Economic Data for the Coming Week:

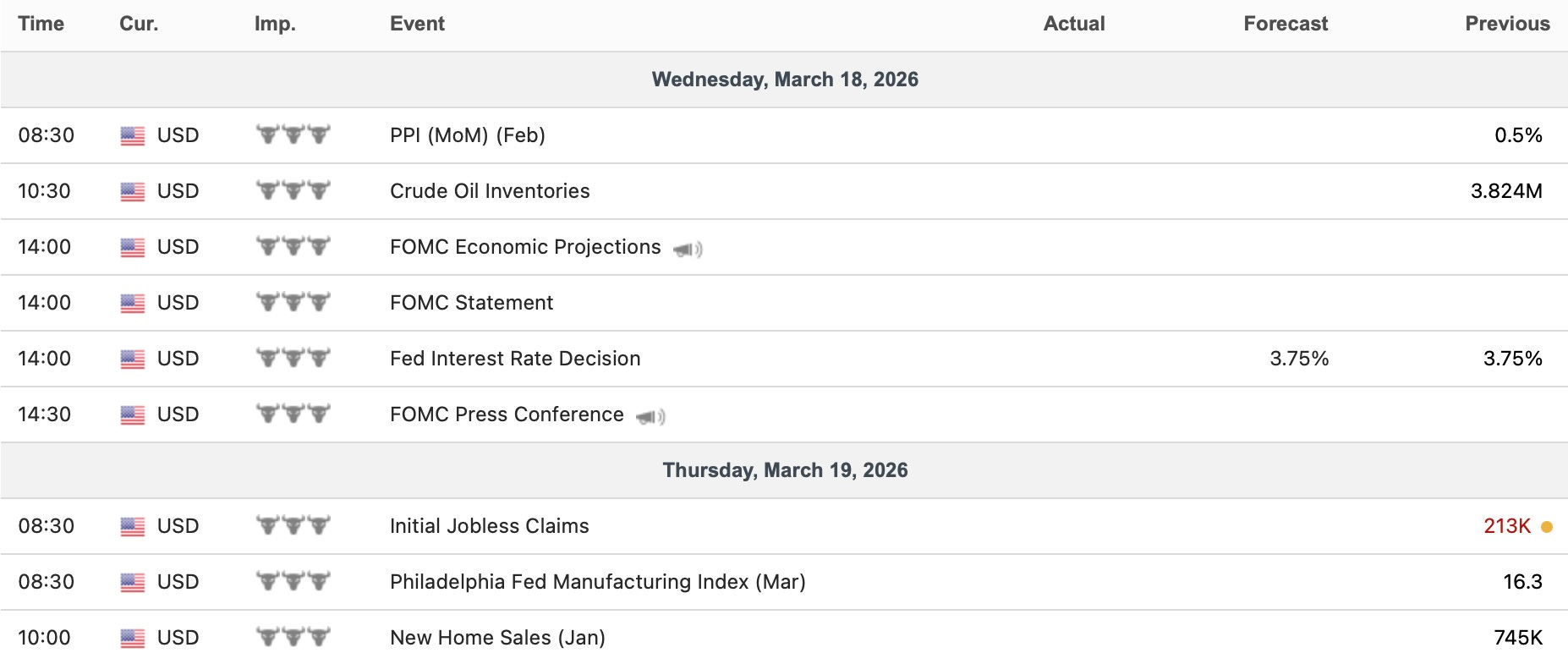

In regard to economic data into the upcoming week, aside from geopolitical concerns, the most important event will be FOMC on Wednesday afternoon, along with the PPI report earlier that morning. Otherwise, it is a fairly quiet week on the economic front, with only a few other scattered datapoints in between.

- STD Channels on Indices for Perspective: Weekly TF

- SPY

- QQQ

- IWM

- DJIA

Since starting this Substack back in June of ‘23, between individual names / tactical trades / baskets, we have netted a 174.01% return whilst in the same period, the Q’s have returned 68.49% / Spooz has returned 58.50% / Dow has returned 44.52% & Small-caps have returned 40.75%, so nice outperformance against all the indices whilst having a 81.8% win rate, averaging a 28.17% return on realized gains / winners & a 15.49% loss on realized losses / losers.

Looking forward to the future & continued success through ‘26.

And for anyone who wants to follow an actively managed portfolio in real time:

I’ve joined Plutus as the cleanest, day-to-day way to track an actively managed portfolio in real time. It’s a live dashboard that’s broader, more diversified, actively managed by me, & updated continuously.

The Eliant Flagship is published on RunPlutus.

Once your Plutus account is approved, you’ll have the option to allocate right away. If you do, it’s straightforward: create an account, link your brokerage (Available only for IBKR at this time), & select the Eliant Flagship (or any of the baskets I’ve built). Your money stays in your account, and trades, position changes, and rebalances are replicated automatically so there’s nothing manual to manage. The idea is to make it easier to access an actively managed portfolio run by me without the overhead of traditional fund structures or high minimums, whilst you keep full custody of your assets & I stay focused on research, positioning, and portfolio construction.

And just to be clear, NOTHING is changing with Substack. It’ll stay exactly what it’s always been since we originally launched in the Summer of ‘23: where I share the thinking, research, & select trades behind my personal PA, along with ongoing commentary across all markets.

For those who may have missed, we published our ‘2026 Outlook’ which has a plethora of coverage on a wide range of topics / themes as ‘26 kicks off after coming off a strong ‘25 & for those whom would like to go back & read the report, I included it just below:

Earlier in 2024, we launched a series titled Educational Pieces, covering a wide range of topics, many of which were suggested directly by you all (4-Part Series).

For those who may have missed the first installment, it covered topics including:

General background / knowledge on all option strategies

In-depth talk on risk / reversals & how to go about expressing / utilizing them

Options Structuring

When to used naked calls / puts vs. spreads

Choosing expiration dates

Identifying key pivots / supports / resistance zones

General briefing on stock gaps

What to look for in regards to fundamentals

Implementing fundamental / macro / technicals into a trade

Hedging

Creating risk/reward setups

Taking profits / managing losses

Overall Process

Book recommendations

A link to the original Educational Piece can be found here .

Given the positive feedback and how useful many of you found the first installment, we followed up with Educational Piece: Part Deux earlier in 2025 & for those who may have missed, a link to the piece can be found here & we then went on to release Educational Piece: Part Trois which can be found here.

And finally, the most recent installment, Educational Piece: Part Quatre, can be found here.

‘Risk management is the silent prerequisite for compounding & true wealth is built not by chasing the highest returns but by ensuring the survival necessary to realize them.’

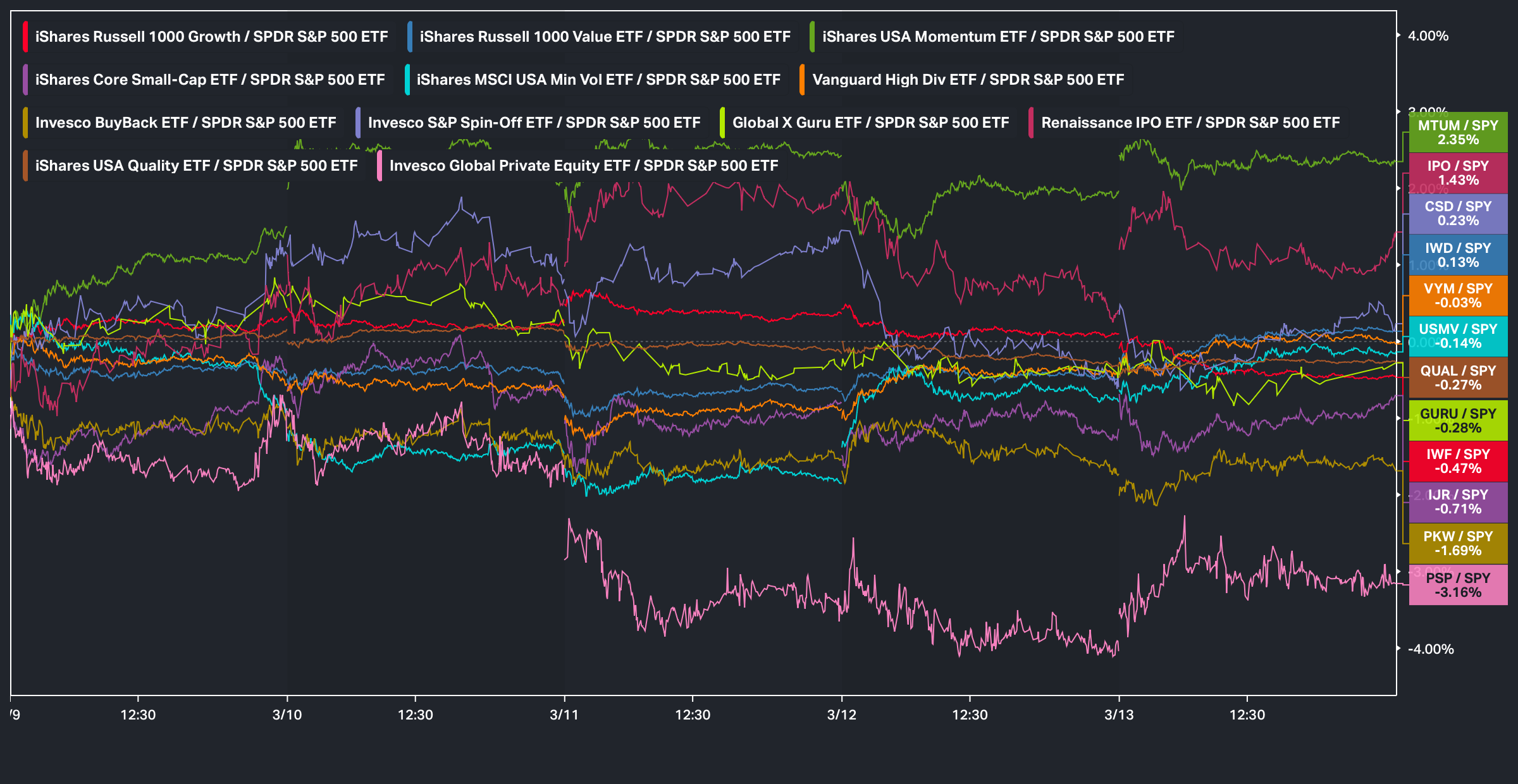

Before we jump into the week ahead, looking back at this past week, in regard to factor performance, Momentum along with IPOs were among the best performing groups, whereas Private Equity was once again among the worst performing factors on the week:

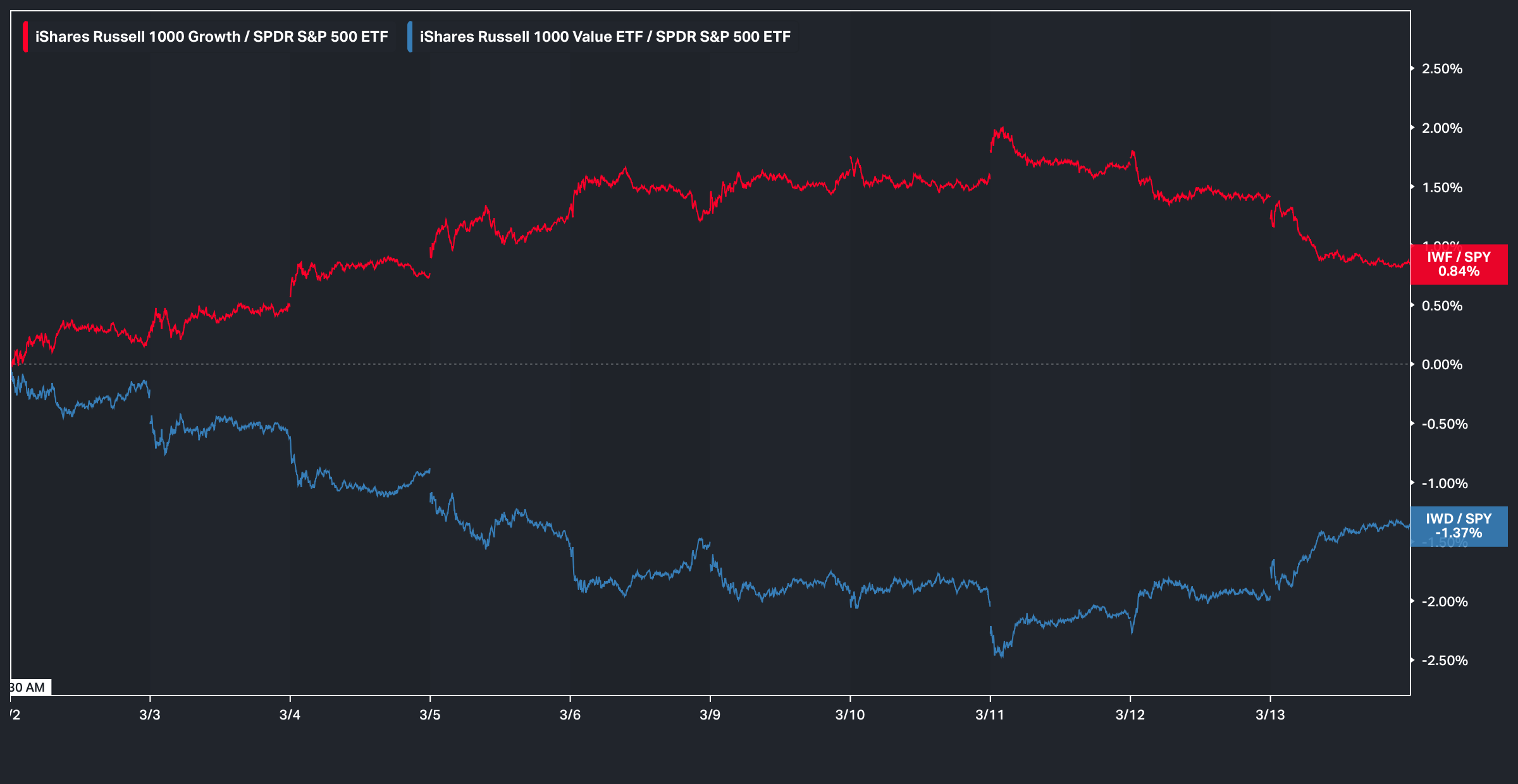

That said, earlier in the week, following the announcement of a coordinated global SPR release along with Trump stating that the ‘war was pretty much over,’ risk assets staged a sharp rebound, leading Growth to outperform Value, with the spread between the two reaching roughly 180bps at one point. However, into the latter half of the week, the de-grossing resumed as the rally in risk faded, leaving Value to close slightly higher on the week and ultimately outperform Growth by roughly 60bps.

However, the most surprising development is that Growth is still outperforming Value since the war first began, with the spread between the two groups having peaked at roughly 450bps, though it has since narrowed to around 220bps following the fade in risk assets during the latter half of this past week:

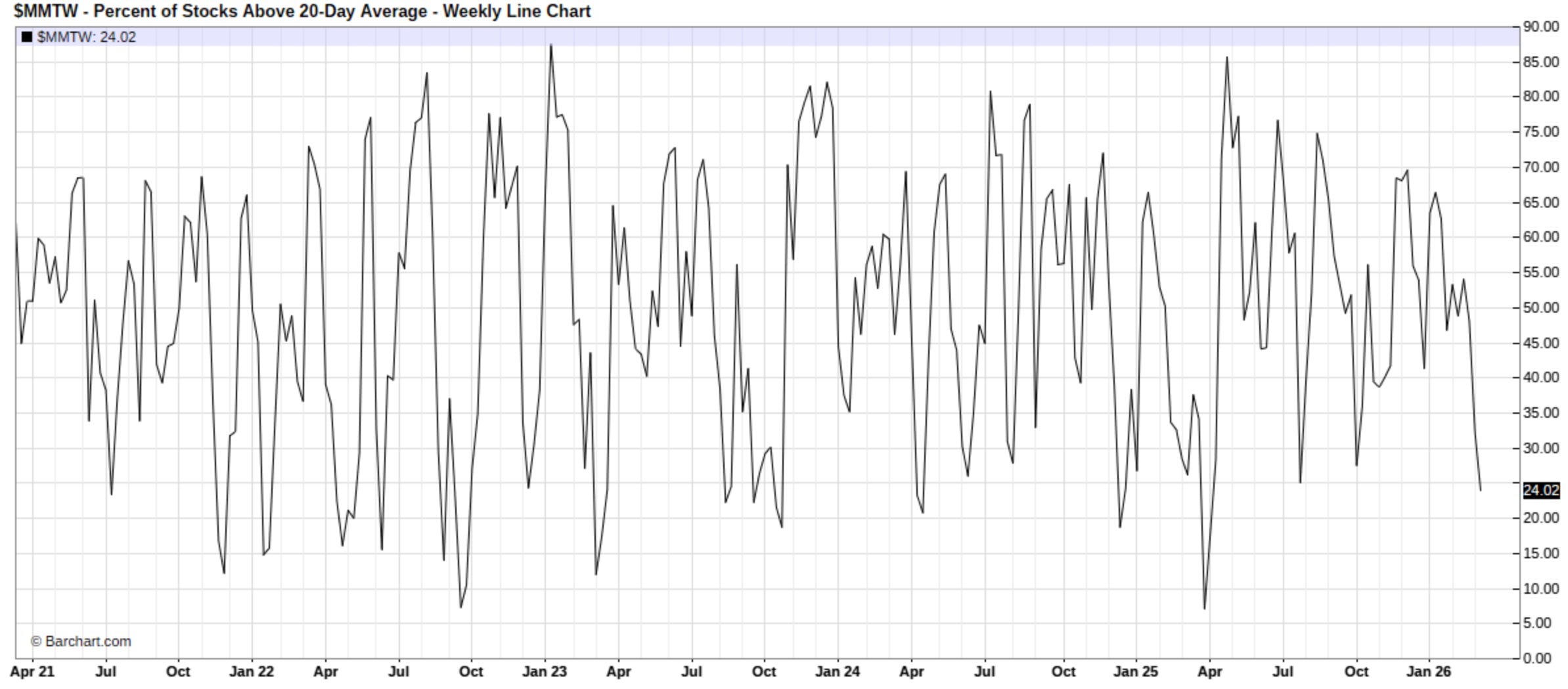

Moving along, despite the choppy downward tape with all of the indices now officially negative on the year and majority sitting lower by just over 3% (Excluding Small-caps), the most notable development has been the deterioration under-the-hood, which has quickly pushed the indices from ‘neutral’ conditions to now oversold & as of now, just 24% of stocks remain above the 20D.

Looking back historically, readings can occasionally fall into the single digits during more extreme washouts, but generally speaking levels in the 15–30% range tend to signal that the market is becoming increasingly oversold, although not yet at full ‘washout’ levels.

And a similar point can be made on a broader timeframe, as roughly 29% of stocks remain above the 50D, which again emphasizes that the market is firmly within oversold territory & while conditions are not yet at ‘extreme’ levels, they are beginning to approach what could be considered near ‘washout’ territory.

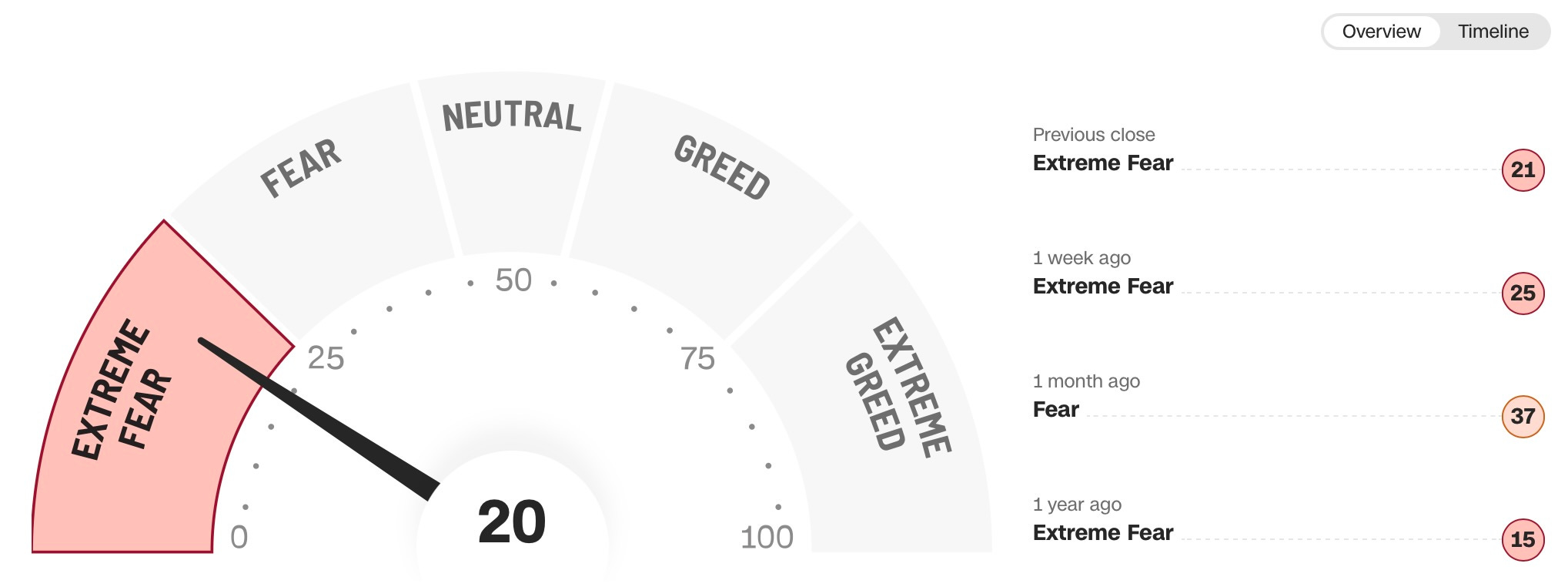

And continuing on that note, even with the S&P sitting just 5% below all-time highs, recent action has pushed markets into ‘extreme fear’ territory.