The Week Ahead 3/9/25

Hello All,

I hope you all are enjoying the weekend and getting some time away from the screens & have had a good kickstart to ‘25.

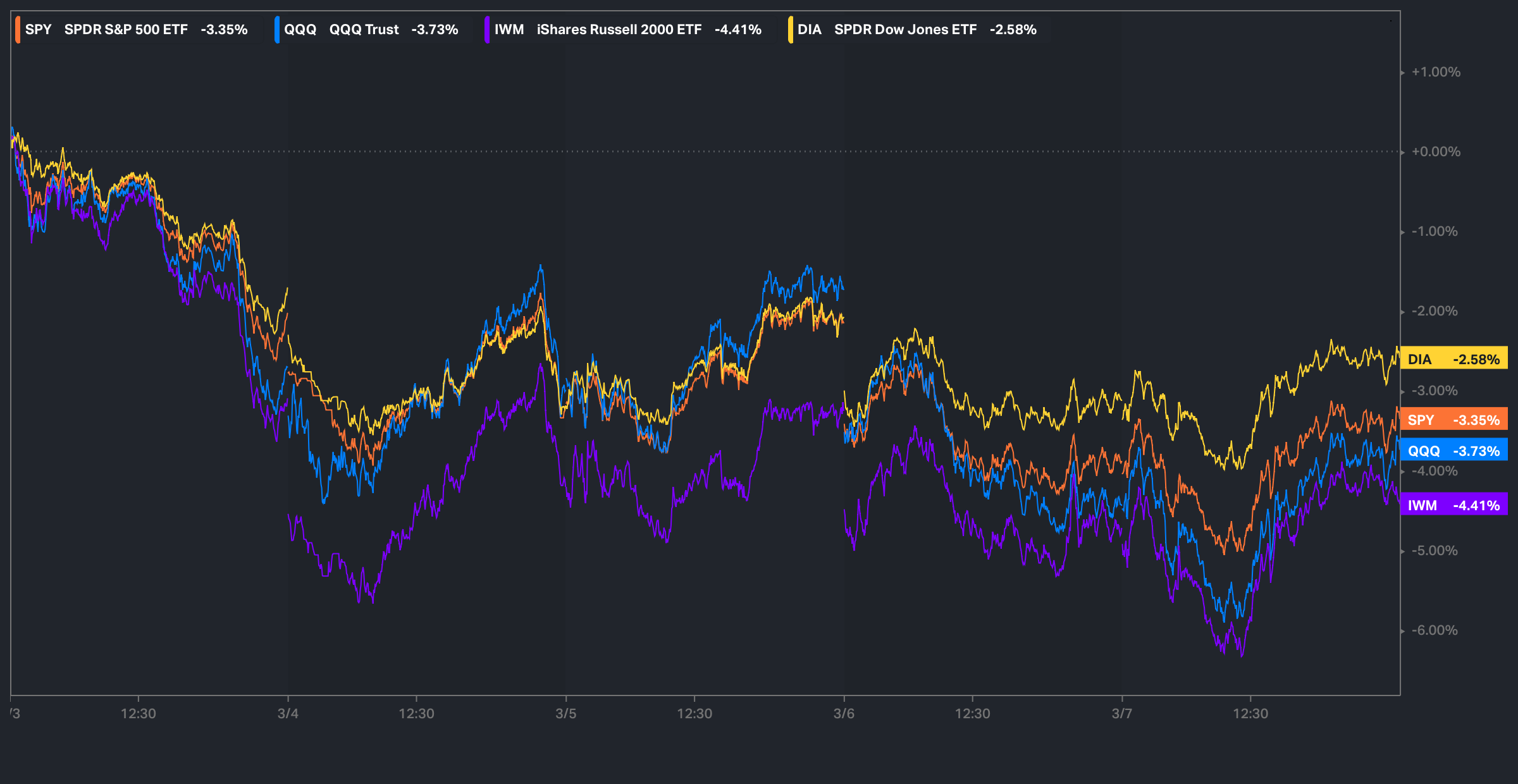

We had quite the week in the indices this past week which was mostly driven by headline volatility… between tariff headlines & recent growth fears along with capital continuing to flock towards ROW, we’ve continued to see this recent pressure in U.S. equites stick as each and every pop has generally continued to get sold.

Small-caps ended up being the worst performing index on the week mostly driven by recent growth fears & uncertainties whereas the Dow was the “best” performing index on the week although still ended up closing the week out lower by just over 250bps & a bigger driver of the recent outperformance has more so been attributed due to some of the components within the Dow being categorized as defensive / flight to lower beta trades.

- Economic Data for the Coming Week:

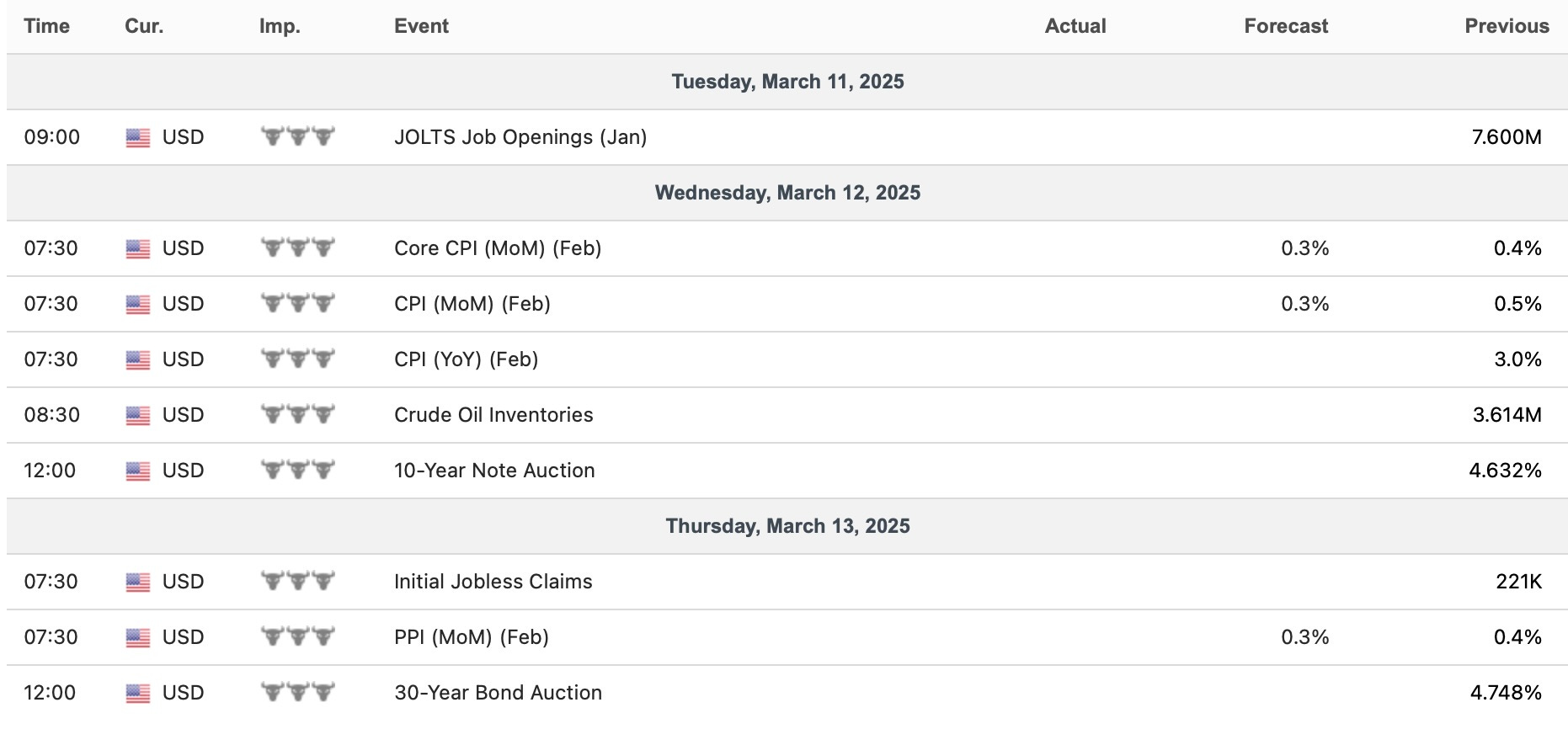

As we look ahead into the upcoming week, the biggest event of the week is CPI #’s on Wednesday although the inflation fears have mostly continued to come to a halt ever since peaking back in January as the fears have completely shifted towards growth / recession fears… the somewhat interesting aspect is we had a fairly decent jobs report Friday (one cautionary flag was the rise in U6, but it was good to see strong private sector #’s considering majority of growth has been driven by both govt. jobs & immigration), but if we were to see a better than expected CPI report this week, maybe the markets shifts back towards goldilocks (disinflation resuming / economy & labor market generally remaining strong).

- STD Channels on Indices for Perspective: Daily TF

- SPY

- QQQ

- IWM

- DJIA

Since starting this Substack back in June of ‘23, between individual names / tactical trades / baskets, we have netted a 108.31% return whilst in the same period, the Q's have returned 38.86% / Spooz has returned 36.23% / Dow has returned 30.69% & Small-caps have returned 16.25%, so nice outperformance against all the indices whilst having a 81.2% win rate, averaging a 19.91% return on realized gains / winners & a 13.19% loss on realized losses / losers.

Looking forward to the future as progress through ‘25.

This past week, we wrote about the recent developments out of Germany given the infrastructure plan that was announced earlier on in the week & covered the setup in detail along with potential beneficiaries & for those who would like to go & read, the article can be viewed here.

Lastly, recently, we published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

To recap this past week, the volatility once again continued which was mostly driven via headlines out of Trump given the general uncertainties surrounding tariffs as the flip-flopping back in forth seems to change by the day… one day tariffs are going on & the next day they are delayed & then the day after that, tariffs are being raised… quite the rollercoaster of emotions which has more so led to this sustained equity vol, BUT… we did get a bit of clarity in the interim (for now a least) as Trump paused tariffs on both Canada & Mexico until the 2nd of April & the one-month exemptions to 25% tariffs on Mexico and Canada are going to cover all USMCA-covered goods.

I did think this was one of the bigger headlines below from this past week…

White House: The US could drop tariffs on Canada and Mexico with fentanyl progress (Fairly self explanatory, but if fentanyl issues see a quicker resolve / nice progress, tariffs could be dropped thus alleviating recent uncertainties). Do still think Trump will continue to be more lenient with Mexico over Canada & China, but in general, conversations between the bunch have been fairly cordial for the most part as it continues to look like real progress is being made / coming to terms to find a resolution.

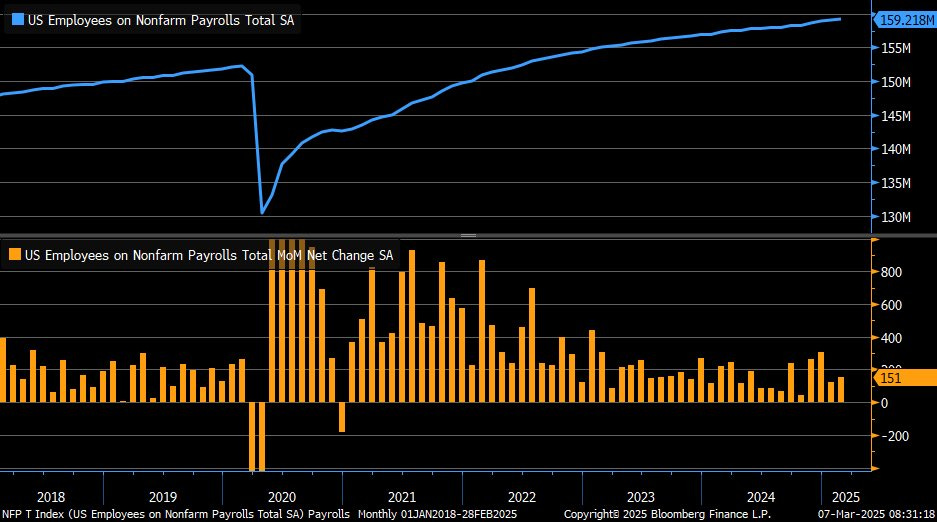

In respect to economic data, we did have a plethora of jobs data, but it was generally a quieter week as there wasn’t necessarily any “surprises” & all of the hype surrounding the jobs report on Friday proved to be disappointing for those whom were looking for a big miss as Jobs ended up coming in just slightly below consensus (151k vs. 160k expected) although we did see a slight uptick in the UER to 4.1% from 4.0%, but in general, the pessimism surrounding the report proved to be overdone & we even saw a nice improvement within the private sector which was more so one of the bigger positive takeaways as growth has more so entirely been driven by both federal / govt. jobs & immigration whilst the private sector has continued to struggle, so it was good to see the positive uptick there.

Lastly, Powell spoke on Friday & he more so kept the same calm, cool, & collective tone… Powell reiterated that the economy is fine & the fed doesn’t need to react & or change course yet as they still would like to see further progress on inflation to resume the cutting cycle & Powell re-assured that hysteria surrounding tariffs is likely to be short-term noise over signal & the Fed won’t react to one-time price spikes.

Heading into this upcoming week, again, the biggest event of the week is CPI #’s on Wednesday & as of now, headline is expected to decline from 2.9% from 3% the prior month although core is expected to remain unchanged… if we were to get better than expected inflation data this week along with the combo of recent growth fears potentially proving to be overdone if economy / labor market data in general continues to hum along, I do think we could start to see the market shift back towards the “goldilocks” narrative (disinflation resuming / economy & labor market generally humming along).

- SPY

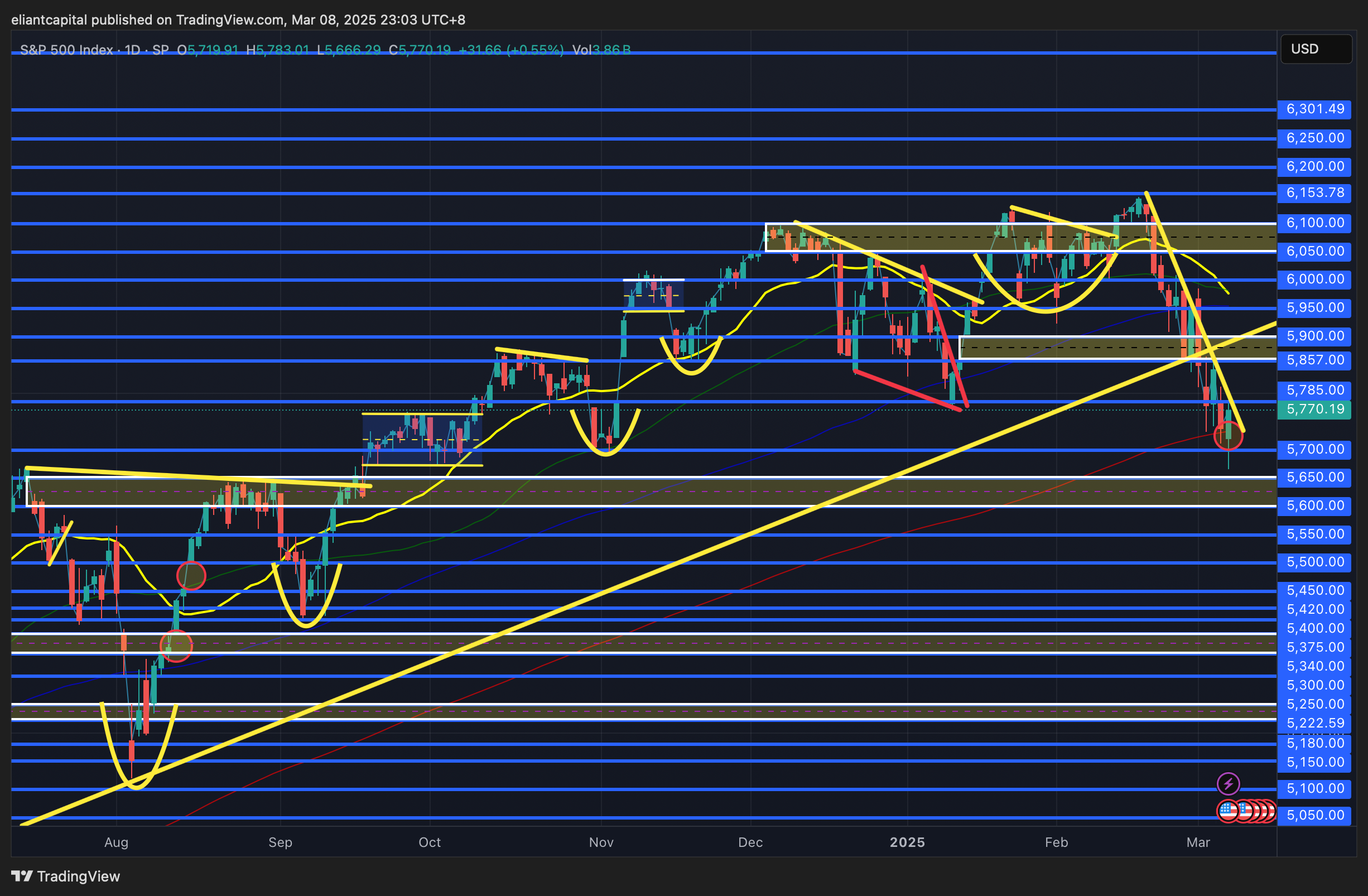

In respect to Spooz, on Friday, we had quite the reversal off the lows as at one point, Spooz was down around 60-handles & Spooz ended up reversing aggressively off those lows & closing out the day green (that action typically signals interim bottoms being in).

Spooz ended up bottoming right off the 50wk whilst also finding support right at the Summer ‘24 highs… an instance of prior resistance flipping to support.

This week is an important one as there is a very good case to be made that Spooz could’ve found its interim bottom on Friday & is now ready for a snapback rally higher… again, not TOO much event risk into this week barring more headlines out of Trump / Bessent etc… but as of now, VIX still remains just under 24… why does this matter for markets? Vol at the end of the day needs a reason to stay elevated & hedges / puts in general are quite expensive… what do we know now? The jobs report Friday alleviated recent growth worries given pessimism was quite high into the report as majority excepted a very soft report… Tariffs were delayed & pushed back to April 2nd & Trump / White House has continued to reiterate that if the fentanyl issues see big progress, tariffs could be dropped completely… Disinflation is looking set to resume after the recent blip these past couple of months… Dollar weakness should be a general tailwind for ERs this next quarter… so where does that leave us in regard to uncertainties? Given the Federal / Govt. jobs that were cut, we’ve yet to see that show up materially in economic data so still are unsure of the entirety of the impact & then lastly, we still have plenty of headline driven volatility although that does look like it could settle down a bit given the interim resolution regarding tariffs / delay until the 2nd of April. With that being said, with some recent uncertainties starting to be cleared up, I think that does make a case for a snapback rally in indices / VIX to come off these recent highs & unwind a bit of the recent rally.

The key question in regard to Spooz / general indices is can we see followthrough to the upside & a break of this interim downtrend… if so, I do think its likely we see Spooz revert higher towards 5850 / 5900ish above to at least backtest this most recent breakdown & then that likely leads to a pause in Spooz before then deciding where to go from there… again, softer & or better than expected inflation data could start to bring back the “goldilocks” narrative back into equites… especially if the recent hysteria surrounding federal / govt. job cuts doesn’t turn out to be anything of significance in the interim / growth fears prove to be overdone.

As mentioned above, but we did see Spooz bottom right off the 50wk whilst finding support at the Summer ‘24 highs & producing a look below and fail of the 200d… again, a very constructive look with significant confluence of support here & I do think the argument is there for Friday to have been the interim bottom… contrary to this being if Fridays reversal ends up unwinding (likely would take a headline of some sort), we could see Spooz work lower towards 5650 / 5600ish, but in general, I do think these lows & or 5650 / 5600ish are a very significant support zone that should lead to a tradeable bottom / snapback rally higher in Spooz & general indices.

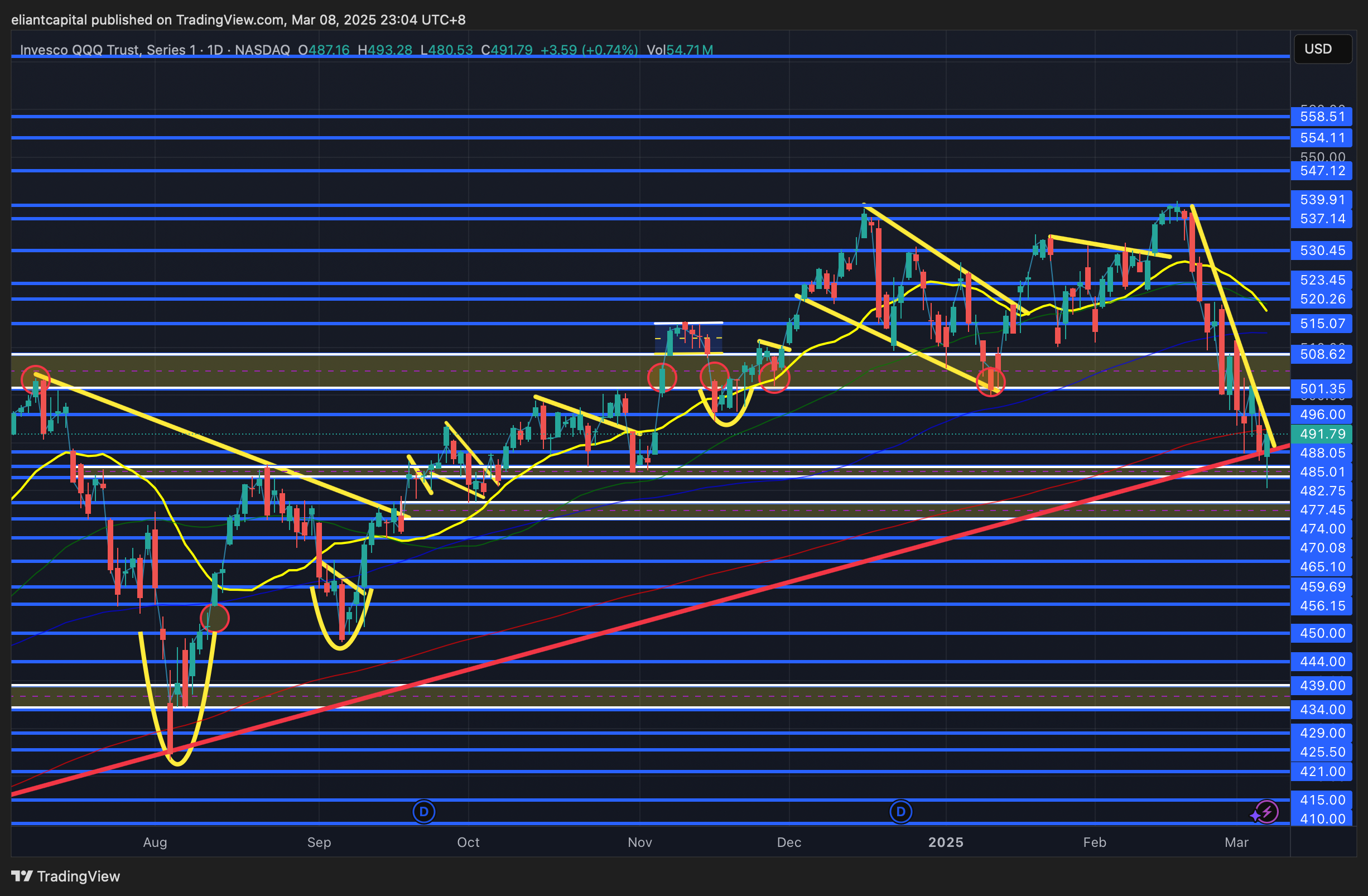

- QQQ

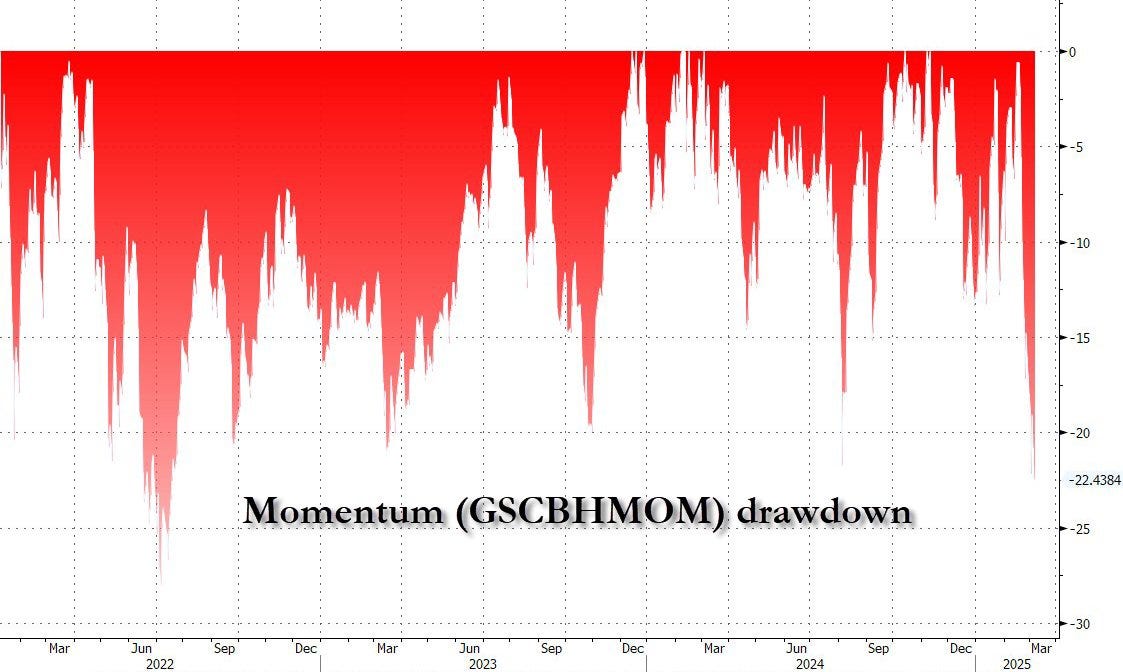

Quite an ugly week for tech this past week as the Q’s ended up closing lower by 370bps on the week along with momentum having it’s largest drawdown since ‘22…

In regard to this past week, despite the aggressive selloff in the Q’s, the Nasdaq still remains within the upward parallel channel it has remained in since late ‘22, so all in all, no “big” technical damage was done on the bigger picture & thus far, this more so has just been a quick & violent pullback to the bottom of the channel as of now.

In respect to the Q’s, again, despite closing out the week just below the 200d, the Q’s have still remained supportive above the TL dating back to late ‘22 whilst also continuing to find buyers near pre-elections levels & given the large intraday reversal on this past Friday, the bigger question here is more so can the Q’s get followthrough to the upside / a gap-up leading to a potential island bottom & or will the downtrend remain / Q’s ultimately need to flush lower instead of the recent controlled selling to find a bottom… more so reside in the former given how constructive the reversal was on Friday off the lows / several tech names had washouts on Friday but closed with hammers across the board… again, if this market can see a bit of followthrough to the upside into next week, we should see the Q’s snap back towards the 501 / 508ish range above, but ultimately, until 508ish on the upside is firmly reclaimed, the Q’s still may be in for some more volatility / rallies may continue to get sold in the interim

On the contrary, if we were to see this support TL below cave in as support (Friday’s reversal invalidates), we could see the Q’s work lower & potentially fill that gap from mid-September near mid-470s.