The Week Ahead 5/25/25

Hello All,

I hope you all are enjoying the long weekend and getting some time away from the screens & have had a good kickstart to ‘25 & I wish you all a successful remainder of Q2.

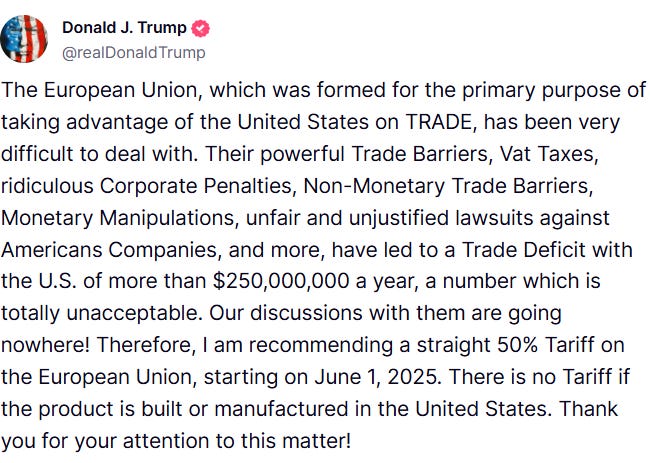

Looking back at this past week, we saw a bit of a pick-up in volatility following the poor bond-auction results mid-week which caused the indices to selloff & work-off the recent overbought conditions thus bringing conditions to a more neutral stance… then to add on to the end of week pressures, Trump threatened Apple with 25% tariffs and then the EU with 50% tariffs starting June 1st… as a result, we saw the indices gap lower on Friday & the worst performing of the indices on the week was small-caps which closed lower by 344bps & the ‘best’ performing of the indices was the Q’s although the Q’s still closed lower by 229bps to round off the week.

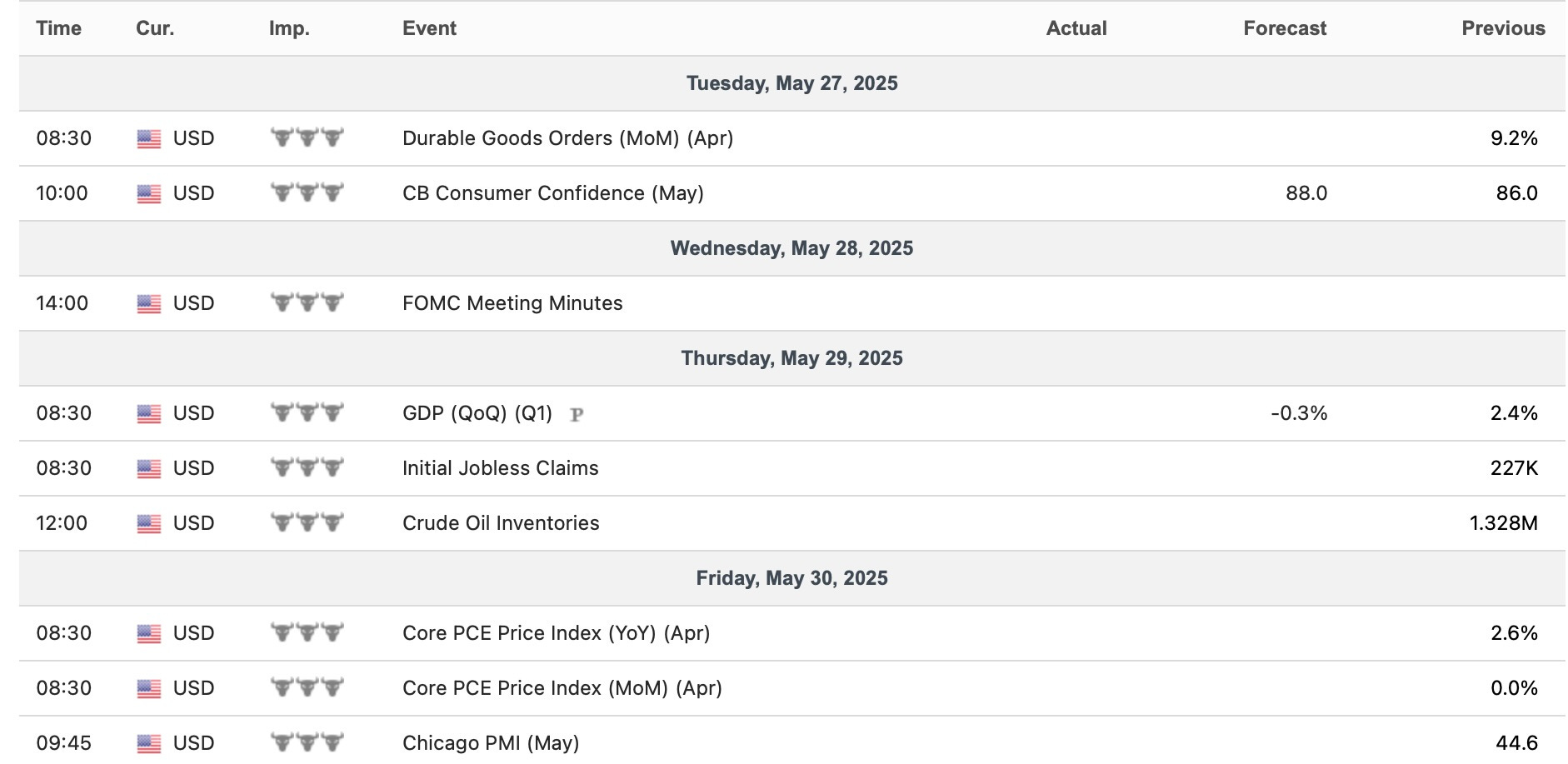

- Economic Data for the Coming Week:

In regard to data into the upcoming week, again, its a relatively quieter one & the biggest event of the week is PCE #’s on Friday & as of now, headline is expected to come in at 2.2% vs. 2.3% prior whereas core is expected to remain unchanged at 2.6%. The trend of data recently is hard-data has continued to hold in better than expected whereas soft-data has been a bit lackluster although did start picking up this past week. With the administration shifting focus from the brief initiatives at austerity back to spending / increasing deficits & growing the economy, data in general likely continues to remain more bifurcated.

- STD Channels on Indices for Perspective: Daily TF

- SPY

- QQQ

- IWM

- DJIA

Since starting this Substack back in June of ‘23, between individual names / tactical trades / baskets, we have netted a 122.25% return whilst in the same period, the Q's have returned 44% / Spooz has returned 37.39% / Dow has returned 27.45% & Small-caps have returned 14.59%, so nice outperformance against all the indices whilst having a 80.2% win rate, averaging a 21.34% return on realized gains / winners & a 14.48% loss on realized losses / losers.

Looking forward to the future as we continue to progress through ‘25.

About a month back, we wrote about hard assets & the structural framework behind hard assets given recent events & future outlook along with some historical perspective as well… you can check it out below for those whom may have missed.

Hard Assets in an Era of Soft Money

As global central banks quietly rearm their stimulus arsenals and fiscal deficits spiral past the point of discipline, the foundations of the global monetary order are beginning to crack. Amid this shift, one question looms larger than ever: Are we on the verge of a new commodity supercycle?

We also published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

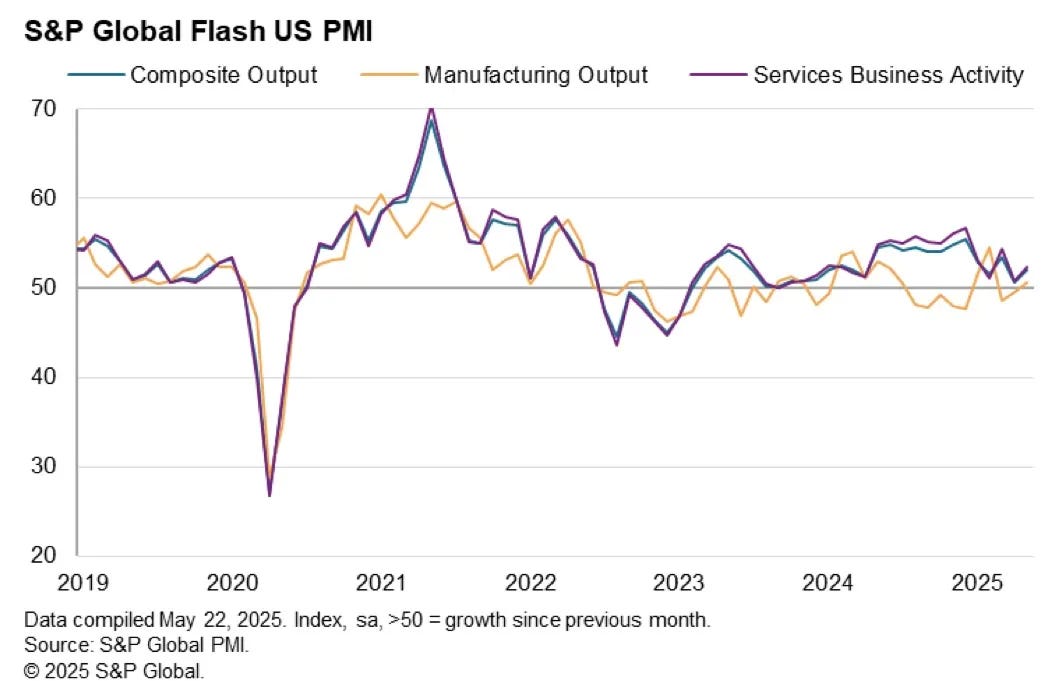

To briefly discuss this past week, it was relatively quiet on the data front, but the biggest surprise came from stronger-than-expected PMI readings, signaling renewed momentum. Manufacturing PMI rose to 52.3 (a 3-month high), Manufacturing Output improved to 50.7, and Services PMI hit 52.3 (a 2-month high), lifting the Composite PMI to 52.0. With all components back above 50, the data points to a solid rebound in private-sector activity and continues to ease recent slowdown concerns. Meanwhile, as we’ll expand on later, the administration continues to shift focus towards “running it hot,” favoring strong economic growth to reduce the deficit-to-GDP ratio by inflating their way out of this mess as we’ve well anticipated.

In regard to other news, to round off the week on this past Friday, Trump threatened Apple with a 25% tariff to motivate to bring back mfg. to the U.S. & on top of that, Trump threatened the EU with 50% tariffs starting June 1st as the EU has been ‘difficult to work with’ thus bringing back tariff uncertainties… question from here being whether or not the EU retaliates & or if the 50% threat makes the EU willing to negotiate / sweeten terms to try and strike an interim deal with the U.S.

And lastly, earlier on in the week this past week, Bessent came out in an interview stating that the administration's focus is to grow the economy faster than the debt in order to stabilize debt-to-GDP. A complete 180-shift as initially coming into the year, the administration touted austerity along with an economic ‘detox’ & instead, they’ve came to the conclusion that ‘running it hot’ will solve their issues as they try & inflate their way out of this mess & kicking-the-can down the road on spending problems is now the best outcome…