Powell Waits While Trump Pressures

Hello All,

As the week has kicked off, it’s been a relatively muted week for the indices as they more so are digesting the recent upside move that took place these last couple of weeks & in respect to FOMC today, it ended up being a complete nothing-burger as not much new was said by Powell & risks / focus continues to shift towards the upcoming weekend as Bessent prepares to meet with China’s foreign ministry in Switzerland to discuss trade as the market continues to anxiously await either a firm deal announcement (with any country) & or some sort of de-escalation with China.

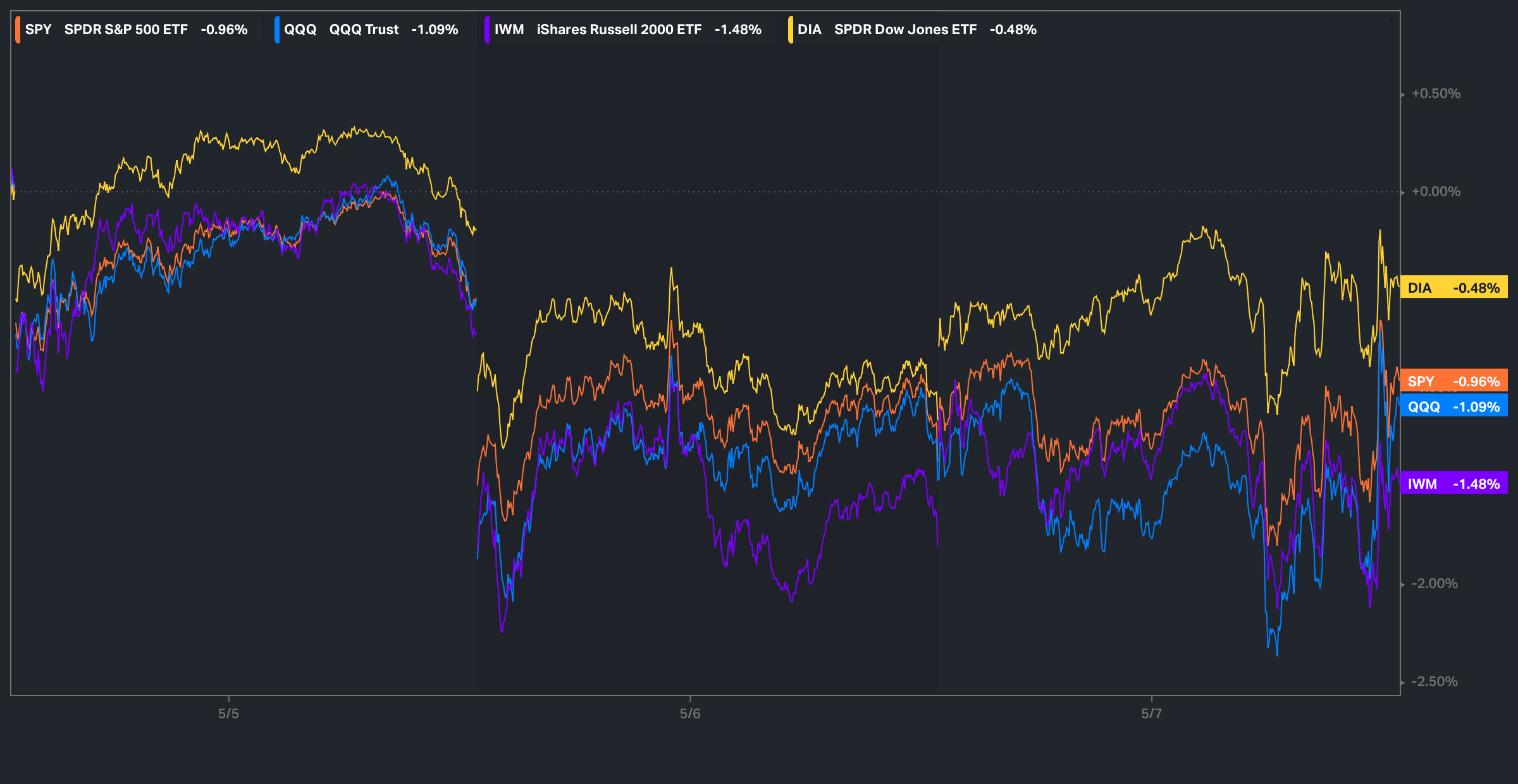

As of now, the Dow has been the best-performing of the indices on the week although still sits lower by just under 50bps & small-caps as of now are the worst-performing of the indices on the week as they sit lower by just under 150bps.

A few weeks back, we wrote about hard assets & the structural framework behind hard assets given recent events & future outlook along with some historical perspective as well… you can check it out below for those whom may have missed.

Hard Assets in an Era of Soft Money

As global central banks quietly rearm their stimulus arsenals and fiscal deficits spiral past the point of discipline, the foundations of the global monetary order are beginning to crack. Amid this shift, one question looms larger than ever: Are we on the verge of a new commodity supercycle?

Recently, we wrote about the recent developments out of Germany given the infrastructure plan that was announced earlier on in the week & covered the setup in detail along with potential beneficiaries & for those who would like to go & read, the article can be viewed here.

Lastly, we published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

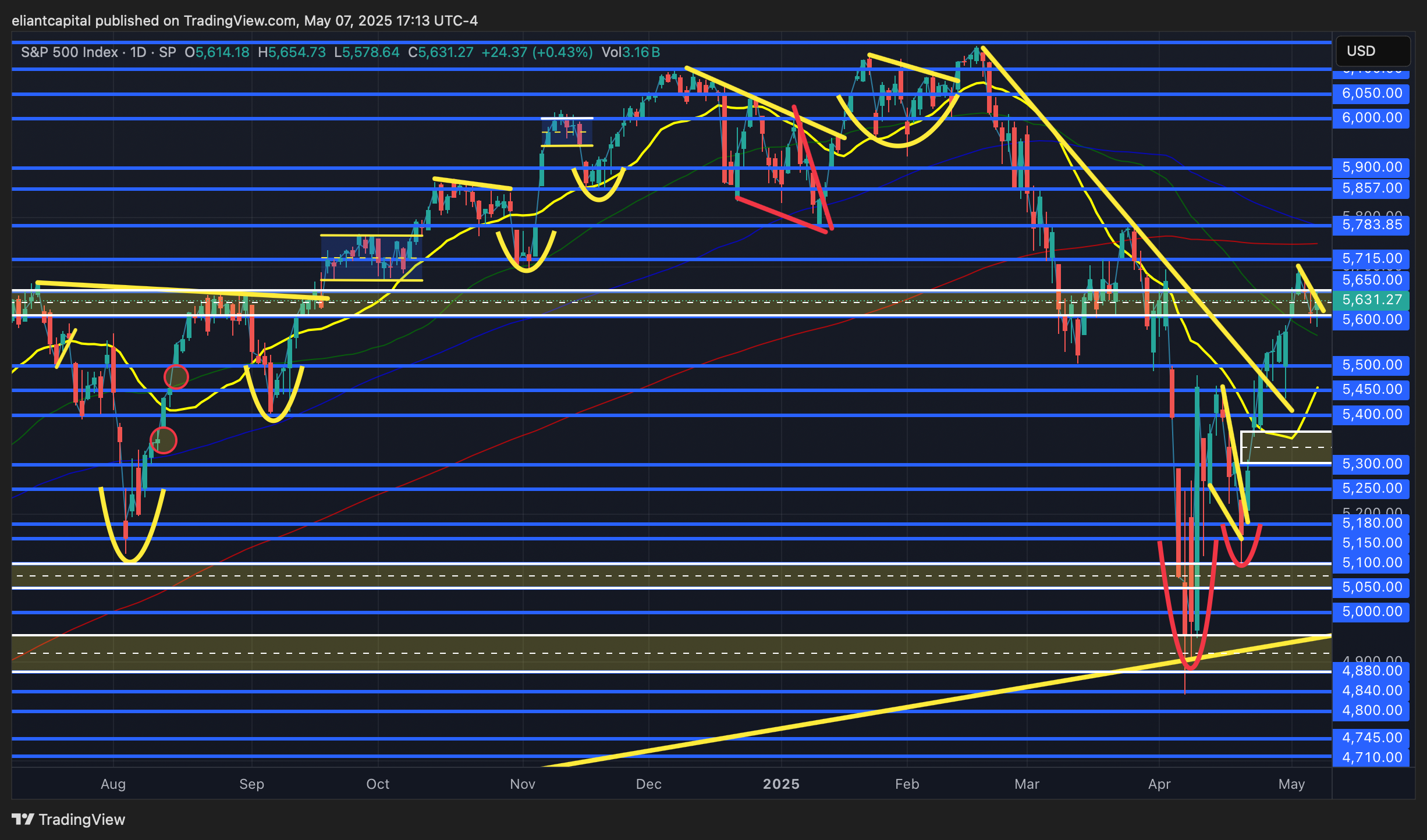

- SPY

Before we jump into Spooz, one important chart I wanted to quickly point out was Spooz & the current divergence between the Advance / Decline line. As of now, as we all know but Spooz is well below the February highs but the interesting phenomenon is the Advance / Decline line continues to make new highs which essentially suggests an improvement to overall market breadth & a positive divergence is currently taking place which essentially is showing that this recent rally has been broad participation which tends to lead to a more bifurcated / supportive market… something to be mindful of as its quite an interesting divergence to say the least.

In respect to Spooz specifically, the overall picture hasn’t changed too much & as we’ll discuss later but not much new was said in regard to FOMC today & in respect to updates with the administration in regard to policy, not much has changed on that front either. We have a relatively quieter remainder of the week ahead & volume in general has been quite low this week & the indices have more so been digesting / consolidating the recent upside move that took place these past couple of weeks as interim overbought conditions get worked off.

In the interim, Spooz remains pinched between the 200d above & 50d just below, similar to the Q’s & Spooz is more so flagging right above the 50d / bull-gap from this past week as well… as long as the bull-gap from this past week does remain supportive (5570/5550ish), I do think indices in general will continue to remain bifurcated & positive developments / hard data continuing to hold in could even push Spooz higher towards the 200d to get that firm test above in the mid-5700s if we were to see Spooz break out of this flag / recent digestion taking place to the upside. On a bit of a bigger picture timeframe as we spoke about this weekend but again to reiterate, Spooz has the 200d / 50wk / 20wk sitting just above so firm resistance does remain above / its essentially a bigger LIS for bears & for Spooz to firmly punch through to the upside, we likely need to see positive developments with China / tariff %’s lower as otherwise, some digestion / consolidation & or even mean-reversion lower given the recent upside move shouldn’t be of too much surprise. I do continue to think that the bigger overall LIS for bulls remains around the bull-gap near 5350ish (U.S. softening rhetoric against China a couple weeks back) & it likely will remain as a bigger LIS likely for the remainder of the quarter although hard data deteriorating will likely push Spooz to fill that bull-gap below if it were to materialize, but for now, I could arguably see Spooz ranging between 5800ish / 5350ish for the time-being to digest this recent upside move (of course markets remain very headline driven so things can flip on a dime).

On the contrary, if last weeks bull-gap near 5550ish were to falter as support, I could see Spooz working lower towards 5500 / 5450ish (coincides with last Wednesday’s low & 20d for added confluence) & that likely will remain a bigger interim pivot, but if it were to falter as support, again, I could see Spooz rolling over to test the prior week from this past week bull-gap below near 5350ish, which as we mentioned just above, it likely remains a bigger pivot for the remainder of the quarter / year & hard-data weakening materially would be a bigger catalyst for that bull-gap to fill entirely (which just hasn’t been the case as hard data continues to hold in thus far).

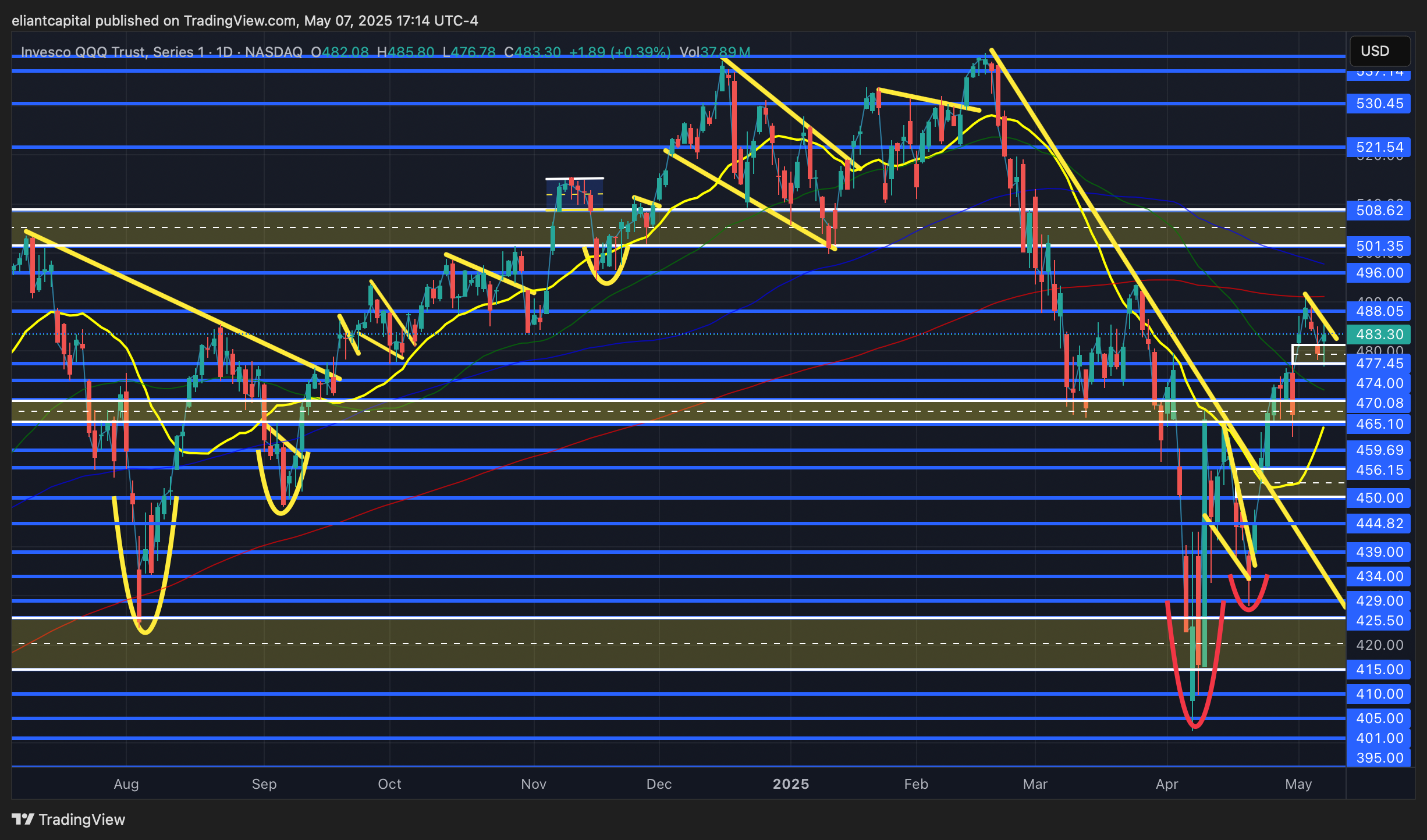

- QQQ

It’s been a relatively quieter & orderly week for the Q’s as the shorter-term overbought conditions get worked off… as we spoke mentioned above but not much new was said in regard to FOMC / Powell’s speech today & into the remainder of the week, we don’t have much data of significance besides tomorrows jobless claims print & then on Friday, we have a plethora of Fed speakers, but otherwise, it’s a relatively quieter remainder of the week ahead. The bigger catalyst remains over the weekend as discussions between the U.S. & China are supposed to take place in Switzerland which was news confirmed last night & then reiterated by Bessent & China’s foreign ministry today.

One interesting chart that we pointed out above with Spooz that fits the same bill for the Nasdaq as well is the Advance / Decline line making new highs. As you can see below but the Nasdaq as we all know is still well below its February highs, but the Advance/Decline line has broken out to new highs thus signaling improving market breadth. The bullish divergence essentially suggests broad participation in the rally and often precedes further upside in the index… something to be mindful of & an interesting divergence to say the least.

In respect to the Q’s, as the week has progressed, we initially saw the Q’s test the 200d above on this past Friday which has presented resistance thus far & more so has created this orderly pullback although we did see the Q’s fill the entirety of the interim bull-gap from this past week which has acted as support thus far. Do continue to think that in the shorter-term, 479 / 474ish on the Q’s will remain as an important pivot / support zone & bulls will remain with edge as long as it remains supportive & if we were to see the Q’s continue to consolidate & remain constructive above the 50d just below, do think we could see an upside impulse in the Q’s if we were to break out of this interim consolation to the upside to start to push higher towards 496 / 501ish (if can firm up above the 200d / likely would coincide with a further upside chase in Mag-8 given how negative positioning remains) which would essentially be a backtest from below of the early January Deepseek lows & would likely be a general pivot that creates some pause for the Q’s on this recent extension of a rally if it were to continue.

On the contrary, if we were to see the Q’s falter below the 50d just below, the 20d sits a tad bit lower near 465ish which coincides with last weeks mid-week low off the headline negative GDP report & I’d argue thats a bigger LIS as faltering below negates the recent trend of higher lows and higher highs which has remained intact since the bottom established in early April. Granted, if those lows were to falter, we likely will see the Q’s continue to roll-over towards the “Softening of rhetoric on China” bull-gap from a couple weeks back near 456ish & in general, that likely remains as one of the more important bull-gaps / pivots for the remainder of the year.

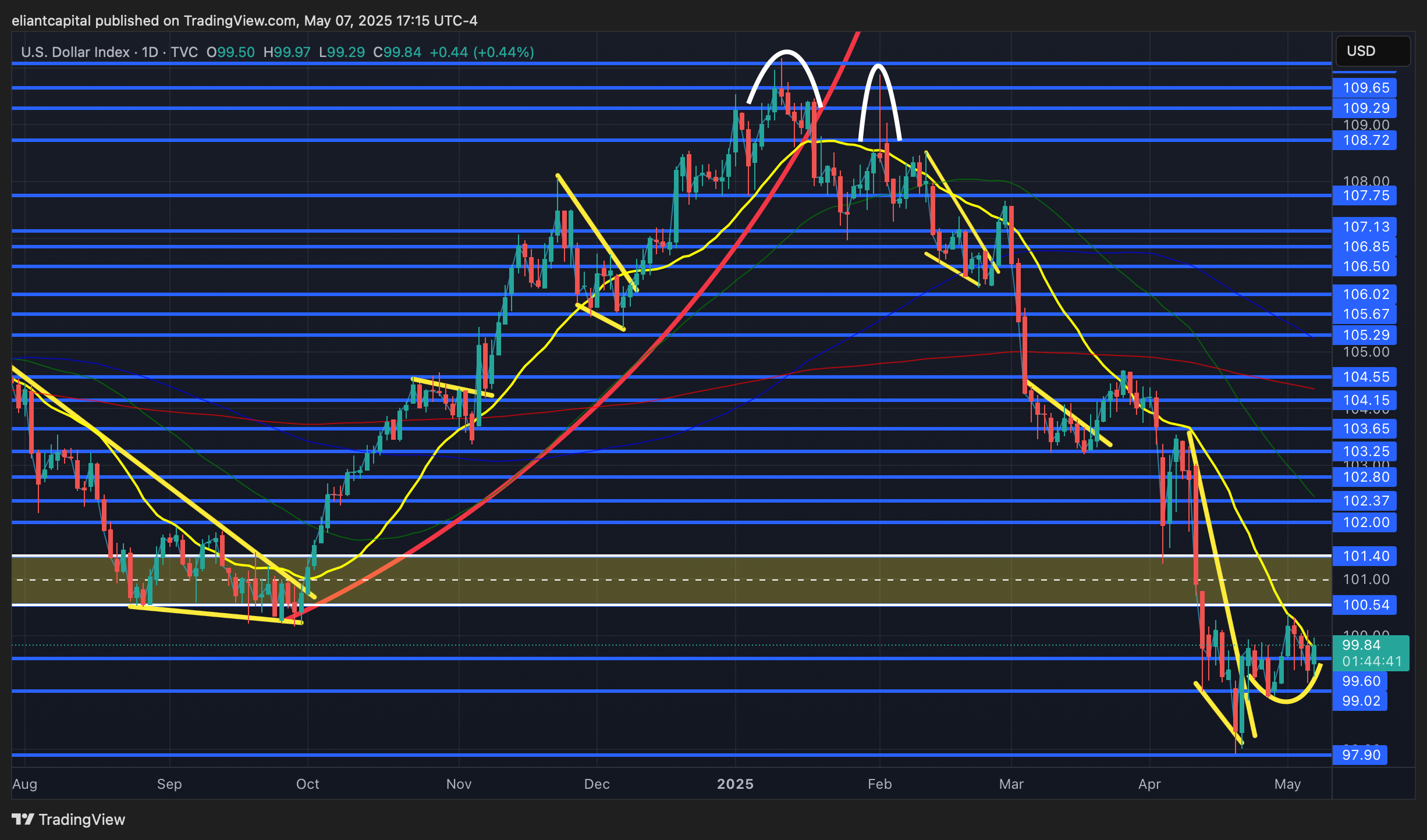

/DXY

To recap today in respect to FOMC… well, it was essentially a nothing-burger. Nothing new particularly was said by Powell & he more or less reiterated the same points in which he did a few weeks back. The Fed is trying to balance the dual mandate whilst acknowledging both labor market & inflation risks together hence wait-and-see is more so the best option at this time & for the Fed to move forward on rate-cuts, they either need to see uncertainties clear up on the inflation picture & the administration to pull back their current extreme policies / reduce tariff rate %’s & or the Fed needs to see hard-data materially weaken & in this case, hard-data has continued to hold in well thus far but as we’ve been stating & as Powell stated today, these next few-months remain detrimental on that aspect as if current policies do remain intact, we’ll likely start to see that reflected in hard-data. As of now, a July cut is still whats priced into markets as of today in terms of when the Fed will look to resume rate-cuts, but again, if the administration remains stubborn on policy & hard-data continues to hold in, the Fed has made it clear that they are in no rush to issue rate-cuts as upside risks with inflation remain apparent & the goal remains to have inflation expectations well-anchored. I don’t think Powell was hawkish today & I don’t think he was dovish either… I think he’s just trying to deal with the cards in which he has been dealt & remain sidelined until more clarity is issued / administration eases up on policy.

In respect to the dollar specifically, we did see the dollar work slightly higher today as it closed higher by just under 50bps, granted, the dollar does still remain below a 100-handle but it does seem like a clear interim bottom has been carved out, but for any sort of material upside / a countertrend rally to ensue, I do think we need to see the dollar at least firm up above 100.5s on the upside to start to push back higher towards 102 / 102.8s above & in general, I do continue to think that it would be a good general fade spot for the dollar whether it be long Euro & or Yen as believe structural damage has taken place this year on the dollar / U.S. credibility has been called into question & if we were to see the counter-trend rally materialize & then start to stall out, I do think the next leg lower in the dollar likely leads the dollar to trade firmly in the mid-90s & potentially even push lower to the lower-90s. We’ve been bearish on the dollar since the beginning of the year & still don’t necessarily see a reason to flip that bias… of course nothing moves in a straight line either.

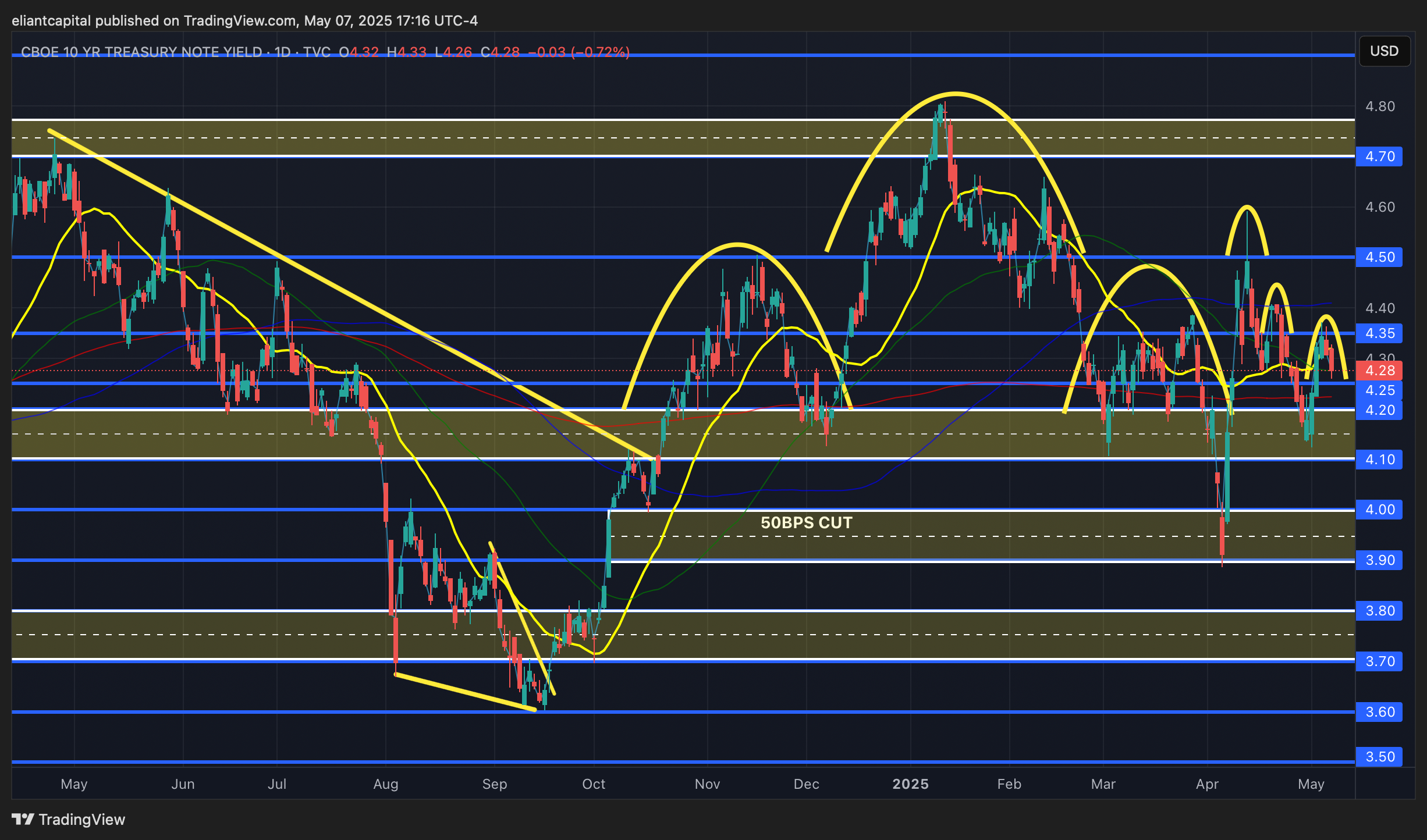

/TNX

As we spoke about above in respect to FOMC today, but not much new was said… the Fed remains in wait-and-see mode & is more so trying to balance both labor market & inflation risks (respecting the dual mandate). The one thing to note is we did see bonds close marginally higher today & bonds did rally post-FOMC & it could potentially be a signal that “the Fed is too late,’’ but again, as long as hard-data continues to hold in & the administration continues to remain stern on policy / provides no relief, the Fed will likely remain on hold until given further confidence to start issuing rate-cuts again.

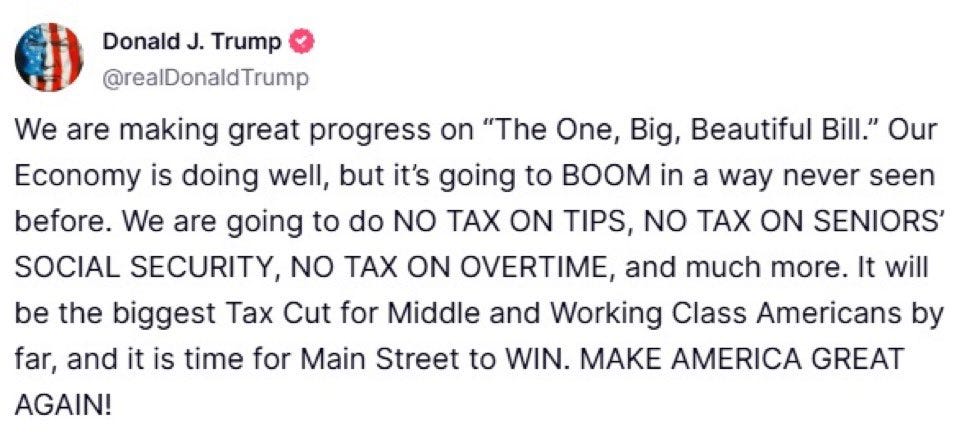

The one interesting headline tonight was out of Trump as shown below:

Big Beautiful Tax-cuts in the works… not Fiscal Austerity by any means & one would imagine if passed that although it would be fiscal stimulative measures towards consumer & economy, bonds likely won’t take it well which is why we have continued to reiterate that upside on the long-end likely remains capped for now & a flush to the upside is likely a short (although it hasn’t presented itself).

As we head into the remainder of the week, again, we don’t have much economic data of significance, but we do have Jobless claims tomorrow & then to round off the week, we have a plethora of fed speakers as well. The biggest catalyst ahead for all markets specifically is this weekend as U.S. & China trade-talks are supposed to take place in Switzerland. It seems as if there is 3 scenarios for this outcome… the first being no progress is made as both the U.S. & China remain stubborn in their own ways & don’t want to be seen as weak… the second is a pause is issued on China to allow for proper negotiations & the third being that both the U.S. & China agree to lower tariff rate %’s on each other to de-escalate the current situation. Bessent is leading the talks which I do think is a bigger positive as he’s been much more rationale than Lutnick & Navarro, but it still seems like the administration wants to be seen as a winner once all is said & done which is more so why the U.S. continues to posture & has been reluctant to lower the 145% tariffs against China as they want China to take the first step towards de-escalation to claim victory & then the U.S. will follow.

If talks do go positively, that should provide upside relief to bonds & if they were to go negative, we may end up getting another bond freakout next week / dollar flush lower as well… something to be mindful of as despite the rally within indices, risks do still remain even if on the surface, rhetoric has drastically softened.

In respect to 10s, as of now, the trend of lower highs continues to remain intact but the 10Y has still remained reluctant to fall below 4.20ish & remain firmly below… if we were to see 10s falter below 4.2ish & remain below, I do think we can see a flush towards the 4.1 / 4.0 range below but it likely would be driven by softening in hard-data & or even the administration walking back policy as otherwise, it’s hard to justify a big rally in bonds, especially the long-end. On the flip side, if we were to see 10s firm up above 4.35ish above, potentially if no progress is made with China over the weekend & or no deals in general are announced, we could get one of those swift moves towards 4.5ish on the 10Y which likely brings out the uneasiness in the administration again. As we’ve mentioned a number of times but the administration has shown they have a clear pain tolerance as the market has kicked them in the mouth twice now & the rapid decline in bonds aren’t welcomed which would likely send the administration a signal that they need to ease up on policy once again if we were to get another freakout (which seems fairly likely if no progress is made within the next week).

As we’ve mentioned but still am not interested in bonds here long or short as they are still stuck in the middle ground of the range (3.65 / 3.8 low-end & 4.75 / 5.0 high-end), but again, would like to fade a bond rally on an upside flush if we do get it (not sure we will).

Again, if looking for a safe-haven / flight-to-safety trade, still think long Yen is a better way to convey instead of bonds but the ideal entry would be a short on USDJPY near 148ish… not sure we get there but its a level I’m watching.