The Week Ahead 5/4/25

Hello All,

I hope you all are enjoying the weekend and getting some time away from the screens & have had a good kickstart to ‘25 & I wish you all a successful remainder Q2.

Last week was a relatively noisy one in respect to headlines / economic data, as initially, indices declined mid-week following the negative headline GDP report but actually ended up closing out the day green… following into the remainder of the week, Microsoft reported a great quarter which led to the indices to extend their gains further as Spooz specifically closed the day for its 8th green-day in a row & then to round off the week, we received positive developments out of China along with a great NFP report which allowed Spooz to extend its gains further for the 9th day in a row… something that hasn’t been done in over 20 years.

The Q’s ended up being the best performing index of the week in part driven by the Mag-7 pump whereas Spooz was surprisingly the worst performing index of the week but still closed higher by just over 290bps.

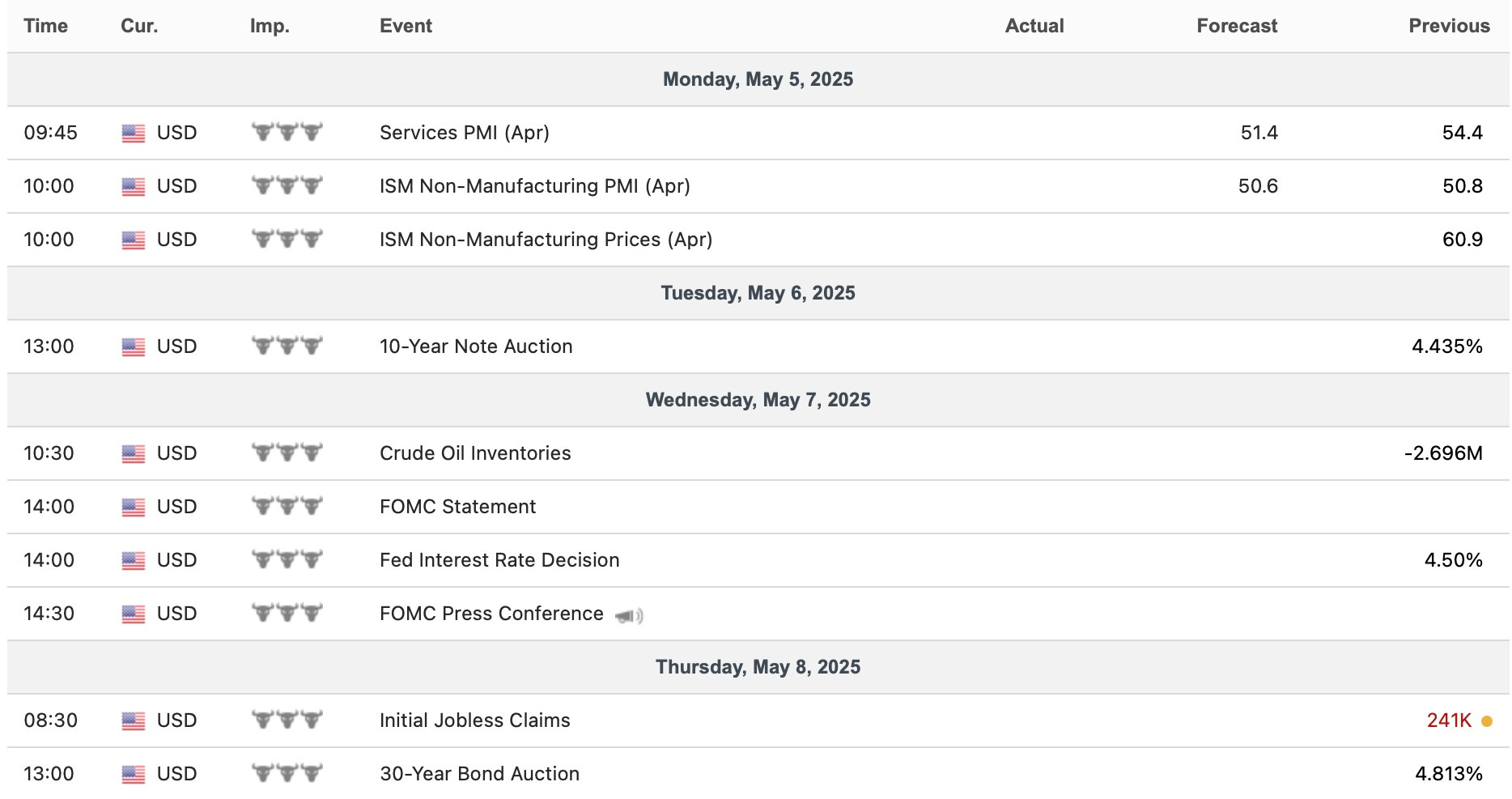

- Economic Data for the Coming Week:

As we get ready to head into the upcoming week, it’s a relatively quieter week ahead in respect to economic data & the biggest event of the week is FOMC day on Wednesday, but we do have a couple of bond auctions throughout the week as well along with some smaller sporadic datapoints too.

- STD Channels on Indices for Perspective: Monthly TF

- SPY

- QQQ

- IWM

- DJIA

Since starting this Substack back in June of ‘23, between individual names / tactical trades / baskets, we have netted a 112.61% return whilst in the same period, the Q's have returned 38.23% / Spooz has returned 34.46% / Dow has returned 26.35% & Small-caps have returned 13.41%, so nice outperformance against all the indices whilst having a 79.8% win rate, averaging a 19.98% return on realized gains / winners & a 14.48% loss on realized losses / losers.

Looking forward to the future as we progress through ‘25.

This past week, we wrote about hard assets & the structural framework behind hard assets given recent events & future outlook along with some historical perspective as well… you can check it out below for those whom may have missed.

Hard Assets in an Era of Soft Money

As global central banks quietly rearm their stimulus arsenals and fiscal deficits spiral past the point of discipline, the foundations of the global monetary order are beginning to crack. Amid this shift, one question looms larger than ever: Are we on the verge of a new commodity supercycle?

Recently, we wrote about the recent developments out of Germany given the infrastructure plan that was announced earlier on in the week & covered the setup in detail along with potential beneficiaries & for those who would like to go & read, the article can be viewed here.

Lastly, recently, we published the follow up educational piece which has been highly requested and majority of the topics covered were all suggested by you all, so I hope you find good benefit.

For those who may have missed, a link to Educational Piece Part: Deux can be found here.

For those who may have missed the first educational piece, I included the range of topics covered below along with a link to the piece for those who would like to go back and read:

- General background / knowledge on all option strategies

- In-depth talk on risk / reversals & how to go about expressing / utilizing them

- Options Structuring

- When to used naked calls / puts vs. spreads

- Choosing expiration dates

- Identifying key pivots / supports / resistance zones

- General briefing on stock gaps

- What to look for in regards to fundamentals

- Implementing fundamental / macro / technicals into a trade

- Hedging

- Creating risk/reward setups

- Taking profits / managing losses

- Overall Process

- Book recommendations

A link to the first educational write-up can be found here.

Last week marked another historical week within markets as Spooz in itself has gone on a 9-Day streak of green days… something that hasn’t happened for over 20-years.

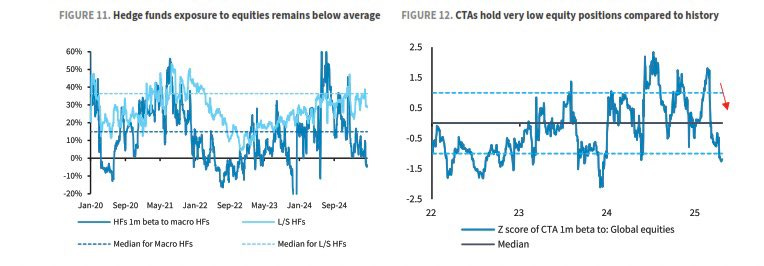

The magnitude of this recent rally has been historic & it hasn’t been of much surprise to us. We’ve highlighted for a few weeks now that positioning / nets were extremely low / HFs & PMs were UW equities hence the 90-Day delay (which we called for) & the softening of rhetoric against China (which we also called for) has ignited this big performance chase after HFs / PMs degrossed near the lows & now have been forced to chase this rally higher.

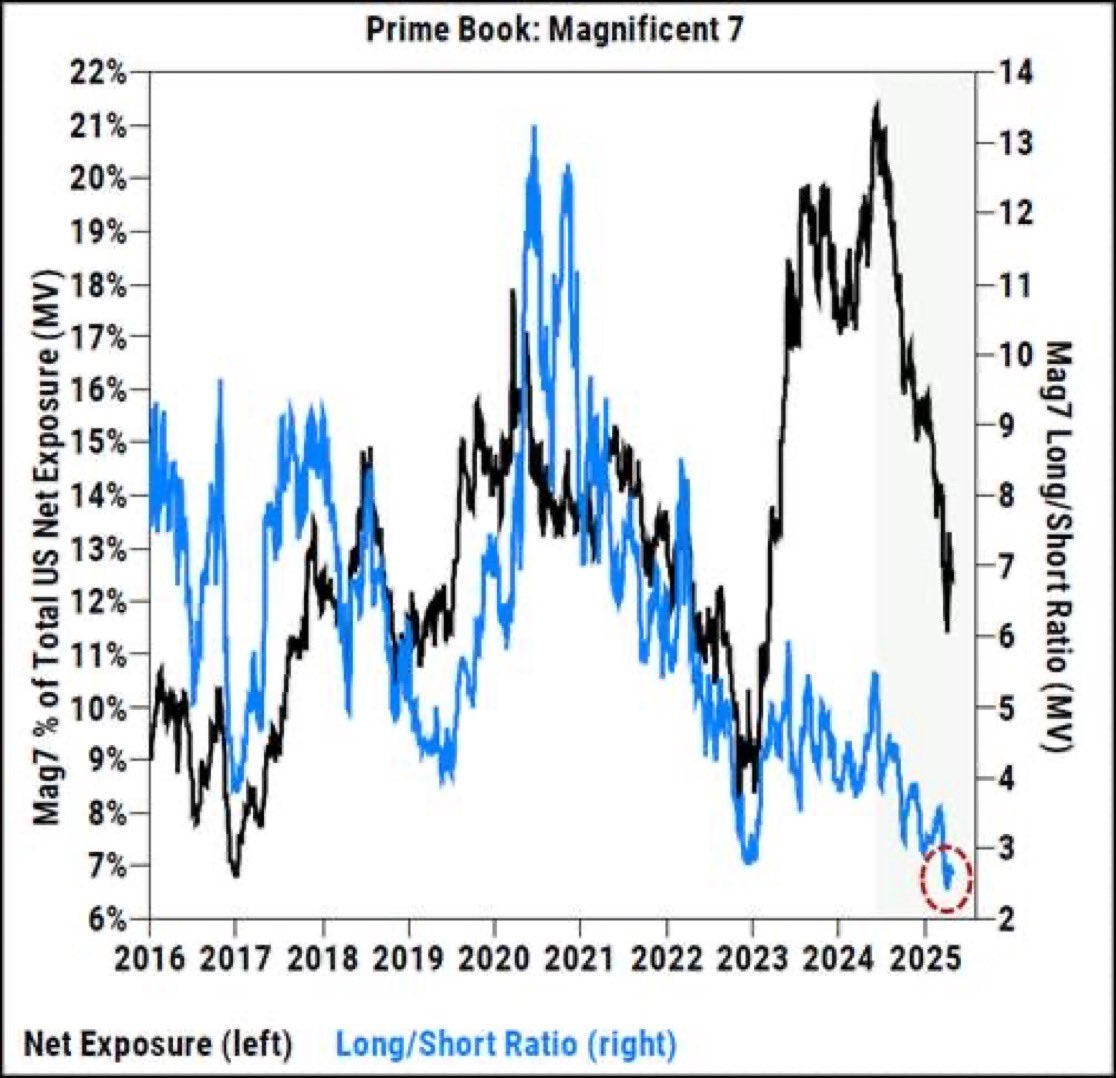

Microsoft’s quarter this past week added to the right-tail chase / fuel to the fire as Mag-7 positioning in itself remains at multi-year lows… this rally has been quite the pain trade to say the least.

As we get ready to head into the upcoming week, the biggest event is FOMC on Wednesday where the Federal Reserve is expected to hold rates. As of now, markets are pricing in the first rate cut for ‘25 in July & 3 cuts are expected this year as of now. The big question into FOMC is whether or not the Federal Reserve stands by that persistent inflation worries due to tariff policies are the main concern thus continuing to be adamant on keeping rates where they are & or if the Federal Reserve argues that inflation could be a one-time price shock due to tariffs. The last time Powell spoke, he argued that tariffs could provide persistent inflation & his general tone / speech was more hawkish & since, PCE #’s posted quite the drop-off this week & are now just shy of the Fed’s target, & in respect to hard data, it has generally held in better than majority have expected, but the next few months will be more important in that regard as we start to see the policy / economic uncertainty side-effects as damage has already been done.

- SPY

In zooming out on the weekly, as we’ve covered previously but the early April low coincided with the 50% retrace from the ‘22 Bear Market low to the recent highs made in February along with the perfect retest of the late ‘21 / early ‘22 highs & lastly, the support TL dating back to the ‘20 Covid lows… the low made ended up being a perfect order of confluence & Spooz hasn’t looked back since. Nevertheless, into the remainder of Q2, Spooz is nearing an important juncture above as it closed just below the 50wk & the 20wk sits just above as well… essentially a big line of defense for bears as otherwise, we may see Spooz continue to churn & trek on higher.

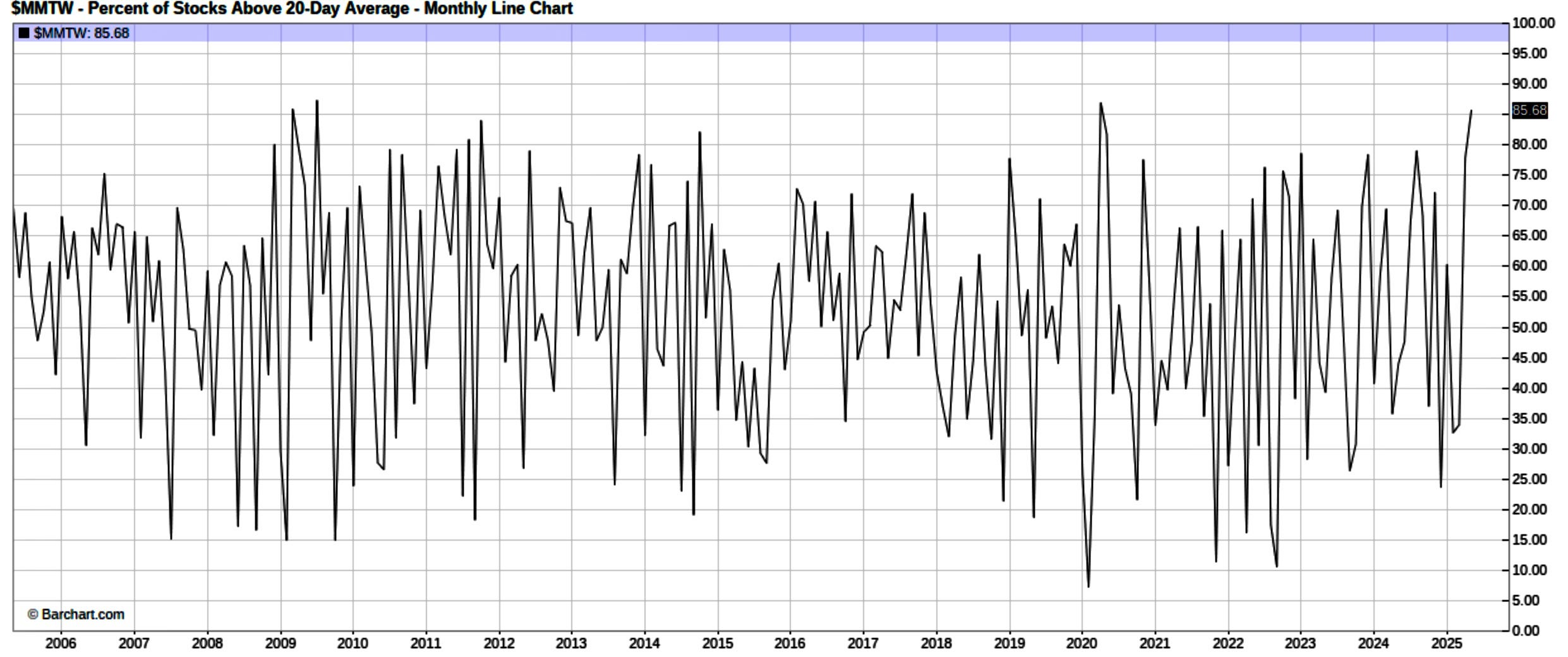

Shorter-term, markets are quite overbought as the percentage of stocks above the 20d has worked back to the high-end of the range… doesn’t necessarily mean the markets are just going to resolve right back lower & crash downwards, but does mean a technical breather / chop & or some sort of consolidation is coming given the recent rally.

Into this upcoming week, again, we do have FOMC on Wednesday & its a lighter week all around in respect to economic data, but the other big factor is how things develop with China.

One big statement that stuck out this past week was out of Miran:

- MIRAN: WOULD BE SURPRISED IF TARIFFS DON'T CHANGE IN FEW WEEKS

Miran is essentially calling for a confirmed de-escalation within the next few weeks & markets are certainly anticipating the positive news given the magnitude of the recent rally in such a short period of time.

On top of the overnight statement out of China on Thursday night:

- China’s Ministry of Commerce stated that it has noted repeated remarks by senior U.S. officials expressing a willingness to engage in tariff negotiations with China. Recently, relevant U.S. parties have also proactively conveyed messages to China, hoping to initiate talks. In response, China is conducting an assessment. The Ministry emphasized that if the U.S. truly wants to negotiate, it must demonstrate sincerity by preparing to correct its wrongful practices and take concrete actions, including removing unilateral tariff hikes.

We also received this headline on Friday out of the WSJ:

Big key factors here is China has acknowledged the U.S. in terms of expressing willingness to negotiate & then in respect to the headline on Friday, it shows Beijing is trying to form an offer to the U.S. to kick off trade talks. I’m sure we will get more developments into the upcoming week, but as we had called for a few weeks back, it seems clear that we reached peak-escalation a few weeks back & now both the U.S. & China are trying to de-escalate the situation.

In respect to Spooz into this upcoming week, as we highlighted earlier but Spooz is sitting just below the 50wk & just above is the 20wk as well which would be a logical spot for bears to look to defend & on the daily, the 200d is sitting about 50-handles higher as well. On Friday, we finally saw a complete unwind in VIX as it has given back all of the Liberation Day Announcement gains & because of that along with the order of confluence with important MAs just above on Spooz, we added 100bps in hedges for August. For those who may have missed, I do think a sensible downside hedge for August is either 540 puts (SPY) & or 5400s (SPX) & you can look to sell 500s (SPY) or 5000s (SPX) against the long-leg to make it a cheaper bet. In terms of a leg lower, I do think bigger pain trade would be Spot down / Vol down... a bit like '22 esque action & or even late ‘23 action unlike the recent panic bid in vol / 17% decline we saw in a matter of 3days earlier on in April that many are likely expecting. Spreads cost around 7.15ish (SPY) & 68.00ish (SPX) & max gain is just under a 6X.

Hard data this past week as we covered Thursday generally held in better than most expected & Friday’s NFP report was another solid report as well. But again, we mentioned that IF the weakness didn’t set in to hard data into these incoming reports, majority of participants would look forward to the next month & following month after the next as well. Recession / Slowdown fears did kick off strong this past week, but did subside as the week progressed which more so added fuel to the recent wall of worry rally. Nevertheless, we do have FOMC next week as we highlighted earlier along with more developments ahead likely with China but in respect to Spooz specifically, again, markets are quite overbought in the short-term but IF the interim bull-gap from this past week below remains supportive (5570/5550ish), I do think indices in general will continue to remain bifurcated & positive developments / hard data continuing to hold in could even push Spooz higher towards the 200d to get that firm test above in the mid-5700s. On a bit of a bigger picture timeframe, again, Spooz has the 200d / 50wk / 20wk sitting just above so pretty good odds barring a headline that Spooz takes a pause here & potentially sees some interim reversion & or at least some sort of chop / consolidation ahead. From the prior week to this past week, I do think a bigger LIS for bulls remains the bull-gap near 5350ish as a generally bigger LIS likely for the remainder of the quarter although hard data deteriorating will likely push Spooz to fill that bull-gap below if it were to materialize, but for now, I could arguably see Spooz ranging between 5800ish / 5350ish for the time-being to digest this recent upside move (of course markets remain very headline driven so things can flip on a dime). The biggest statement by bulls would be firmly reclaiming the 200d above & making a higher-high above the late March highs near 5780ish… we’ll see how things develop.

However, if we were to see Spooz mean revert in the interim & if last weeks bull-gap near 5550ish were to falter as support, I could see Spooz working lower towards 5500 / 5450ish (coincides with last Wednesday’s low) & that likely will remain a bigger interim pivot, but if it were to falter as support, again, I could see Spooz rolling over to test the prior week from this past week bull-gap below near 5350ish which also happens to coincide with the 20d as well for an added support of confluence.

- QQQ

Similar story as with Q’s as to Spooz, but as of now, the Q’s closed just below the 50wk with the 20wk sitting just above as well & on the daily, the 200d too… an important test for the indices into these next few weeks.

As we noted above earlier but positioning in Mag-7 at multi-year lows along with the great report out of MSFT this past week more so fueled the right-tail trade in tech as the Q’s were the best performing of the indices on the week as the Q’s closed higher by just under 350bps. Because of the low allocation to Mag-7 / right-tail chase, that could lead the Q’s to be a bit more bifurcated as Mag-7 potentially tries to reclaim the prior flight-to-safety trade after flushing earlier on in April… we’ll see how things develop but something to keep in mind given how negative positioning still remains.

Given the gap-up following MSFT’s earnings report this past week, the Q’s established another bull-gap below & the Q’s ended up gapping over the 50d as well along with nearly tapping the 200d on Friday. The big question from here is if the Q’s can manage to go on and firmly reclaim the 200d & or if it flips into resistance thus capping this interim rally for now likely leading to the Q’s / general indices to at least backtest lower before deciding where to go from there. Again, we’re in an interesting spot as Mag-7 net exposure remains extremely underweight which can fuel a right-tail performance chase & then on the other hand, we still have economic uncertainties to deal with even-though uncertainties do continue to clear up by the day which has more so fueled this large rally off the lows.

Nevertheless, in the interim, if bulls can manage to sustain above this bull-gap created this past week (479 / 477ish), I do think bulls will continue to remain with edge & it *could lead the Q’s to potentially consolidate / build out a flag before trying to firm up above the 200d & if the chase were to continue, I could see the Q’s ultimately working higher towards 496 / 501ish above which coincides with a backtest of the early January Deepseek lows & would likely be a general pivot that creates some pause for the Q’s.

On the contrary, if we were to see the bull-gap created this past week falter as support, I do think 465 / 463ish below (This past Wednesday’s Low) is a bigger LIS for bulls as you could argue another higher low was established off the “weak” hard data, but if those lows were to falter, we likely will see the Q’s continue to roll-over towards the prior week to this past weeks bull-gap below near 456ish (China softening rhetoric bull-gap) which also coincides with a backtest of the 20d & would likely be a more firm support if backtested below.